As filed with the Securities and Exchange Commission on November 29, 2024

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact Name of Registrant as Specified in Its Charter)

| 4954 | Not applicable | |||

(State or Other jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

+

(Address, Including Zip Code, And Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

(Name, Address, Including Zip Code, And Telephone Number, Including Area Code, of Agent For Service)

Copies of all correspondence to:

Mitchell S. Nussbaum, Esq.

David J. Levine, Esq.

Loeb & Loeb, LLP

345 Park Avenue

New York, NY 10154

(212) 407-4000

Fax: (212) 407-4990

Approximate date of commencement of proposed sale to the public: From time to time after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☒

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate

by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933. Emerging growth

company.

If

an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided

pursuant to Section 7(a)(2)(B) of the Securities Act.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED NOVEMBER 29, 2024

PRELIMINARY PROSPECTUS

ESGL HOLDINGS LIMITED

17,241,380 Ordinary Shares

We are registering for resale by the selling shareholders named herein (the “Selling Shareholders”) up to 17,241,380 of our ordinary shares, $0.0001 par value per share (the “Ordinary Shares”).

The Selling Shareholders may offer, sell or distribute all or a portion of the securities hereby registered publicly or through private transactions at prevailing market prices or at negotiated prices. We will not receive any of the proceeds from such sales of the Ordinary Shares. We will bear all costs, expenses and fees in connection with the registration of these securities, including with regard to compliance with state securities or “blue sky” laws. The Selling Shareholders will bear all commissions and discounts, if any, attributable to their sale of Ordinary Shares. See “Plan of Distribution.”

Our Ordinary Shares are listed on Nasdaq Capital Market under the symbol “ESGL”. On November 27, 2024, the last reported sales price of our Ordinary Shares was $1.35 per share.

The Ordinary Shares being registered for resale in this prospectus will constitute a considerable percentage of our “public float” (defined as the number of our outstanding Ordinary Shares held by non-affiliates). In addition, the Ordinary Shares being registered for resale hereunder were purchased by the Selling Shareholders at a price below the current market price of our Ordinary Shares. Given the substantial amount of redemptions in connection with the Business Combination and the relative lack of liquidity in our stock, sales of our Ordinary Shares under the registration statement of which this prospectus is a part could result in a significant decline in the market price of our securities.

Investing in our securities involves a high degree of risk. You should review carefully the risks and uncertainties described under the heading “Risk Factors” beginning on page 6 of this prospectus, and under similar headings in any amendment or supplements to this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2024

TABLE OF CONTENTS

No one has been authorized to provide you with information that is different from that contained in this prospectus. This prospectus is dated as of the date set forth on the cover hereof. You should not assume that the information contained in this prospectus is accurate as of any date other than that date.

For investors outside the United States: We have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

| i |

SELECTED DEFINITIONS

| ● | “$” or “US$” or “U.S. dollars” or “USD” refers to the legal currency of the United States. | |

| ● | “Amended and Restated Memorandum of Association” means ESGL’s amended and restated memorandum of association adopted by special resolutions dated July 28, 2023 and effective on August 2, 2023. | |

| ● | “Board” means the board of directors of the Company. | |

| ● | “Business Combination” means the Merger contemplated by the Merger Agreement. | |

| ● | “Code” means the Internal Revenue Code of 1986, as amended. | |

| ● | “Company” means ESGL Holdings Limited. | |

| ● | “Closing” means the closing of the Business Combination. | |

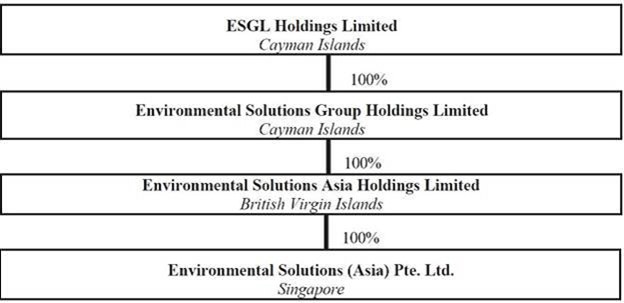

| ● | “ESA” means Environmental Solutions (Asia) Pte. Ltd., which was incorporated under the laws of Singapore on May 8, 1999. | |

| ● | “ESGH” means Environmental Solutions Group Holdings Limited, a holding company incorporated under the laws of the Cayman Islands as an exempted company with limited liability on November 18, 2022. | |

| ● | “ESGL” means ESGL Holdings Limited, a Cayman Islands exempt company. | |

| ● | “Exchange Act” means the Securities Exchange Act of 1934, as amended. | |

| ● | “founder shares” means the 2,156,250 Ordinary Shares issued to the Initial Stockholders at Closing in exchange for the 2,156,250 shares of GUCC Class B common stock issued for an aggregate purchase price of $25,000 in March 2021. | |

| ● | “GAAP” means accounting principles generally accepted in the United States of America. | |

| ● | “Group” means ESGL and its subsidiaries, including ESGH, ES BVI and ESA. | |

| ● | “GUCC” means Genesis Unicorn Capital Corp., a Delaware corporation. | |

| ● | “GUCC Class A common stock” or “Class A common stock” means the Class A common stock, $0.0001 par value per share, of Genesis Unicorn Capital Corp. | |

| ● | “GUCC Class B common stock” or “Class B common stock” means the Class B common stock, $0.0001 par value per share, of Genesis Unicorn Capital Corp. | |

| ● | “GUCC common stock” or “common stock” means shares of GUCC Class A common stock and GUCC Class B common stock, collectively. | |

| ● | “IASB” means International Accounting Standards Board. | |

| ● | “IFRS” means International Financial Reporting Standards as issued by the IASB. | |

| ● | “Initial Stockholders” means the Sponsor and other initial holders of founder shares. | |

| ● | “IPO” refers to the initial public offering of 8,625,000 units (including 1,125,000 units as a result of the underwriters’ exercise of its over-allotment option) of GUCC consummated on February 17, 2022. | |

| ● | “IRS” means the United States Internal Revenue Service. | |

| ● | “Merger” means the transactions contemplated by the Merger Agreement. |

| ● | “Merger Agreement” means that certain Agreement and Plan of Merger, dated as of November 29, 2022, as may be amended from time to time, by and among ESGL, GUCC, ESGH, and the other parties named therein. | |

| ● | “Ordinary Shares” means the ordinary shares, $0.0001 par value per share, of ESGL. | |

| ● | “Private Units” means the units issued to the Sponsor in a private placement simultaneously with the closing of IPO, with each unit included one Ordinary Share and one Private Warrant. | |

| ● | “Private Warrants” means the warrants included in the Private Units issued to the Sponsor in a private placement simultaneously with the closing of IPO, with each Private Warrant entitling the holder to purchase one Ordinary Share. | |

| ● | “Public Warrants” means the public warrants issued in the IPO, with each Public Warrant entitling the holder to purchase one Ordinary Share. | |

| ● | “SEC” means the U.S. Securities and Exchange Commission. | |

| ● | “Securities Act” means the Securities Act of 1933, as amended. | |

| ● | “Sponsor” means Genesis Unicorn Capital, LLC, a Delaware limited liability company. |

| 1 |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this prospectus may constitute “forward-looking statements” for purposes of the federal securities laws. ESGL’s forward-looking statements include, but are not limited to, statements regarding ESGL or its management team’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “appear,” “approximate,” “believe,” “continue,” “could,” “estimate,” “expect,” “foresee,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “seek,” “should,” “would” and similar expressions (or the negative version of such words or expressions) may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this prospectus may include, for example, statements about:

The forward-looking statements are based on the current expectations of the management of ESGL, as applicable, and are inherently subject to uncertainties and changes in circumstances and their potential effects and speak only as of the date of such statement. There can be no assurance that future developments will be those that have been anticipated. These forward-looking statements involve a number of risks, uncertainties or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described in “Risk Factors,” those discussed and identified in public filings made with the SEC by ESGL and the following:

| ● | fluctuations in the Group’s revenues, earnings and cash flows based on changes in commodity prices, as commodity prices for circular products are particularly susceptible to volatility based on regulations and tariffs that affect our ability to export products; | |

| ● | changes in policies imposed by governments may impact on the availability and costs of employing non-Singapore workers; | |

| ● | the Group’s ability to maintain its licenses, permits and accreditations that are required to operate its business; | |

| ● | expectations regarding the Group’s strategies and future financial performance, including its future business plans or objectives, prospective performance and opportunities and competitors, revenues, backlog conversion, products and services, pricing, operating expenses, market trends, liquidity, cash flows and uses of cash, capital expenditures, and ability to invest in growth initiatives and pursue acquisition opportunities; | |

| ● | risks related to the general economic and financial market conditions; political, legal and regulatory environment; and the industry in which the Group operates; | |

| ● | the outcome of any legal proceedings that may be instituted against ESGL; | |

| ● | limited liquidity and trading of ESGL’s securities; | |

| ● | geopolitical risk and changes in applicable laws or regulations; | |

| ● | the possibility that ESGL may be adversely affected by other economic, business, and/or competitive factors; | |

| ● | operational risks; and | |

| ● | litigation and regulatory enforcement risks, including the diversion of management time and attention and the additional costs and demands on the Group’s resources. |

Should one or more of these risks or uncertainties materialize or should any of the assumptions made by the management of ESGL be incorrect, actual results may vary in material respects from those projected in these forward-looking statements.

All subsequent written and oral forward-looking statements concerning the Business Combination or other matters addressed in this registration statement and attributable to ESGL or any person acting on their behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this registration statement. Except to the extent required by applicable law or regulation, ESGL undertakes no obligation to update these forward-looking statements to reflect events or circumstances after the date of this registration statement or to reflect the occurrence of unanticipated events.

| 2 |

SUMMARY OF THE PROSPECTUS

This summary highlights selected information from this prospectus and does not contain all of the information that is important to you in making an investment decision. This summary is qualified in its entirety by the more detailed information included in this prospectus. Before making your investment decision with respect to our securities, you should carefully read this entire prospectus, including the information under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and the financial statements included elsewhere in this prospectus.

Unless otherwise indicated or the context otherwise requires, references in this prospectus to “ESGL,” “Company”, “we,” “our,” “us” “Group” and other similar terms refer to ESGL Holdings Limited and our consolidated subsidiaries.

General

ESGL is a holding company incorporated as an exempted company under the laws of the Cayman Islands. As a holding company with no material operations of its own, ESGL conducts all its operations through its operating entity incorporated in Singapore, Environmental Solutions (Asia) Pte. Ltd. (“ESA”).

ESA is a waste management, treatment and recycling company involved in the collection and recycling of hazardous and non-hazardous industrial waste from customers such as pharmaceutical, semiconductor, petrochemical and electroplating companies. ESA currently has two revenue streams, from: (i) services income which is primarily comprised of the fees it charges its customers for waste collection and disposal services, which fees are similar to those charged by ESA’s competitors, and (ii) the sales and trading of ESA’s circular products that are made and processed from the recycled waste collected from its customers with respect to its waste collection and disposal services, which ESA believes makes ESA a unique and environmentally friendly offering in the marketplace.

A fundamental tenet of ESA is that waste is a resource to be reused, repurposed and recirculated. ESA believes that this mindset of creating commodities from waste sets itself apart from the linear traditional waste industry participants, which largely only generate income from the collection, destruction and disposal of post-collection waste. This philosophy is ingrained and reflected in ESA’s business operations where it utilizes renewable energy and by-products produced from ESA’s waste treatment process to reduce its own operating costs. In line with this mindset, ESA’s primary business focus is the conversion and processing of industrial waste (that would otherwise be unused in the waste recycling process) into circular products such as pyrolysis oil, diesel, metals such as nickel, zinc, copper, silver, gold, minerals such as lime (calcium hydroxide) and fluorspar (calcium fluoride), and chemicals such as hydrochloric acid, sulfuric acid, and calcium chloride. ESA then sells these converted circular products to local and international end users, traders or overseas refiners who require the circular products for their own commercial use or for further processing including manufacturing and galvanizing purposes.

For the six months ended June 30, 2024, the Group’s revenues generated from services income and sales of circular products were approximately US$2.7 million and US$0.8 million respectively. For the two years ended December 31, 2023 and 2022, the Group’s revenue generated from services income was approximately US$3.9 million and US$2.2 million respectively. For the two years ended December 31, 2023 and 2022, the Group’s revenue generated from the sales and trading of its circular products was approximately US$2.3 million and US$2.7 million respectively.

On February 17, 2022, GUCC consummated its initial public offering of 8,625,000 of its units, each consisting of one share of Class A common stock and one redeemable Public Warrant entitling the holder thereof to purchase one share of Class A common stock at price of $11.50, at a purchase price per unit of $10.00. On August 2, 2023, GUCC reincorporated to the Cayman Islands and reincorporated into ESGL, with ESGL continuing as the surviving entity.

ESGL, a Cayman Islands exempted company with limited liability, was formed on November 18, 2022. ESGL’s principal executive office is located at 101 Tuas South Avenue 2 Singapore 637226, telephone number is +65 6653 2299.

| 3 |

Private Placement

On August 21, 2024, we entered into a Share Purchase Agreement (the “Purchase Agreement”) with certain accredited investors named therein (the “Purchasers”), pursuant to which we issued in an initial closing of a private placement an aggregate of 13,800,000 ordinary shares to the Purchasers at a purchase price of US$0.29 per share. The initial closing of the private placement occurred on August 22, 2024 (the “Closing Date”) and we received gross proceeds of $4,002,000. For a period of three months following the Closing Date, Mr. Samuel Wu, one of the Purchasers, was granted the right to purchase up to an additional 3,441,380 Ordinary Shares for gross proceeds of $998,000 on the same and terms and conditions set forth in the Purchase Agreement (the “Second Closing Option”). The Second Closing Option was exercised in full by such Purchaser on September 30, 2024. Accordingly, we issued an aggregate of 17,241,380 Ordinary Shares in the private placement for aggregate gross proceeds to the Company of $5,000,000.

The Ordinary Shares were issued and sold by us in a private placement pursuant to the exemption provided in Section 4(a)(2) under the Securities Act. As soon as practicable following the expiration of the Second Closing Option, we agreed to use commercially reasonable efforts to prepare and file a resale registration statement on Form F-1 with the Securities and Exchange Commission registering the Ordinary Shares issued pursuant to the Purchase Agreement for resale on behalf of the Purchasers. We also agreed to use commercially reasonable efforts to cause such registration statement to be declared effective under the Securities Act as promptly as possible after the filing thereof, and shall use our commercially reasonable efforts to keep such registration statement continuously effective under the Securities Act until the date that all of the shares covered by such registration statement (i) have been sold thereunder or pursuant to Rule 144, or (ii) may be sold without volume or manner-of-sale restrictions pursuant to Rule 144.

Risk Factors Summary

Investing in our securities involves risks. You should carefully consider the risks described in “Risk Factors” before making a decision to invest in our ordinary shares. If any of these risks actually occurs, our business, financial condition and results of operations would likely be materially adversely affected. In such case, the trading price of our securities would likely decline, and you may lose all or part of your investment. Set forth below is a summary of some of the principal risks we face:

Risks Relating to the Group’s Business and Industry

| ● | For the two years ended December 31, 2023 and 2022 and the 6-month period ended June 30, 2024, the Group has incurred operating losses and may incur significant losses for the foreseeable future. The Group may not generate sufficient revenue or become profitable or, if it achieves profitability, it may not be able to sustain it. | |

| ● | The environmental services industry is highly competitive and includes competitors that may have greater financial and operational resources, flexibility to reduce prices or other competitive advantages that could make it difficult for the Group to compete effectively. | |

| ● | The Group requires a significant amount of capital to fund its operations and growth. If the Group cannot obtain sufficient capital on acceptable terms, its business, financial condition, and prospects may be materially and adversely affected. | |

| ● | Fluctuations in prices for recyclable waste materials the Group collects from its customers and the circular products that it sells to local and international end users, traders or overseas refiners may adversely affect the Group’s revenue, operating income, and cash flows. | |

| ● | The Group may not be able to enhance its existing recycling, reuse, disposal and waste treatment solutions and develop new solutions in a timely manner. | |

| ● | The Group may not be able to enhance its existing recycling, reuse, disposal and waste treatment solutions and develop new solutions in a timely manner. | |

| ● | Acute and chronic weather events, including those brought about by climate change, may limit the Group’s operations and increase the costs of collection, transfer, disposal, and other environmental services it provides. | |

| ● | The Group’s revenues, earnings and cash flows will fluctuate based on changes in commodity prices, and commodity prices for circular products are particularly susceptible to volatility based on regulations and tariffs that affect its ability to export products. | |

| ● | The Group may have environmental liabilities that are not covered by its insurance. Changes in insurance markets also may impact its financial results. | |

| ● | The Group could be required to make immediate repayment of certain of its outstanding debt with financial institutions. | |

| ● | The Group’s strategy includes an increasing dependence on technology in its operations. If any of its key technology fails, its business could be adversely affected. | |

| ● | The Group is exposed to environmental liability. |

Risks Relating to our Securities

| ● | Although as a foreign private issuer, ESGL is exempt from certain corporate governance standards applicable to US domestic issuers, if ESGL cannot continue to satisfy the continued listing requirements and other rules of Nasdaq, ESGL’s securities may not be listed or may be delisted, which could negatively affect the price of its securities and your ability to sell them. | |

| ● | Currently, our Ordinary Shares and Warrants are listed on the Nasdaq Capital Market. However, there may not be enough liquidity in such market to enable shareholders to sell their securities. | |

| ● | Certain judgments obtained against us by our shareholders may not be enforceable. | |

| ● | The sale or availability for sale of substantial amounts of Ordinary Shares could adversely affect their market price. | |

| ● | The market price of our equity securities may be volatile, and your investment could suffer or decline in value. |

Risks Relating to Operating as a Public Company

| ● | ESGL’s management team has limited experience managing a public company. | |

| ● | If ESGL fails to implement and maintain an effective system of internal controls to remediate its material weaknesses over financial reporting, ESGL may be unable to accurately report its results of operations, meets its reporting obligations or prevent fraud, and investor confidence and the market price of Ordinary Shares may be materially and adversely affected. | |

| ● | ESGL may be a “passive foreign investment company,” or “PFIC”, which could result in adverse U.S. federal income tax consequences to U.S. Holders. |

The other matters described in the section titled “Risk Factors”.

| 4 |

THE OFFERING

| Issuer | ESGL Holdings Limited | |

| Securities offered by the Selling Shareholders | We are registering for resale by the Selling Shareholders up to 17,241,380 Ordinary Shares. | |

| Terms of the offering | The Selling Shareholders will determine when and how he will dispose of the Ordinary Shares registered under this prospectus for resale. | |

| Shares outstanding prior to the offering | 40,239,419 | |

| Shares outstanding after the offering | 40,239,419 | |

| Use of proceeds | We will not receive any of the proceeds from the sale of the Ordinary Shares by the Selling Shareholders. See “Use of Proceeds.” | |

| Nasdaq ticker symbols | Our Ordinary Shares and our Public Warrants are listed on the Nasdaq Capital Market under the symbols “ESGL” and “ESGLW,” respectively. |

| 5 |

RISK FACTORS

An investment in our securities involves a high degree of risk. You should carefully consider the risks described below before making an investment decision. Our business, prospects, financial condition, or operating results could be harmed by any of these risks, as well as other risks not known to us or that we consider immaterial as of the date of this prospectus. The trading price of our securities could decline due to any of these risks, and, as a result, you may lose all or part of your investment. The following discussion should be read in conjunction with ESGL’s financial statements and notes thereto included herein. You should carefully consider the following risk factors in addition to the other information included in this prospectus, including matters addressed in the section titled “Cautionary Statement Regarding Forward-Looking Statements.”

Risks Relating to the Group’s Business and Industry

For the two years ended December 31, 2023 and 2022 and the six months ended June 30, 2024, the Group has incurred operating losses and may incur significant losses for the foreseeable future. The Group may not generate sufficient revenue or become profitable or, if it achieves profitability, it may not be able to sustain it.

For the two years ended December 31, 2023 and 2022, the Group’s net losses were US$94,979,338 and US$2,391,812, respectively. As of December 31, 2023, the Group had an accumulated losses of US$99,985,928. For the six months ended June 30, 2024, the Group’s net losses were US$471,424 and the Group had an accumulated losses of US$100,457,352.

Substantially all of the Group’s losses have resulted from approximately US$93.1 million of listing expenses which are non-operational and non-recurring. In the financial year ended December 31, 2022, the Group incurred approximately US$981,000 of Listing Expenses. The Group’s Listing Expenses in the year ended December 31, 2023 mainly arose from the accounting treatment of its share based consideration for the Business Combination and the revaluation of the Forward Purchase Agreement “FPA”. In the previous financial year, the Listing Expenses were mainly professional fees incurred for the Business Combination.

The other major contributor to the net loss were expenses incurred in connection with the depreciation of property, plant and equipment, the purchase of raw materials, employee benefits expenses and its other operating expenses. The Group may continue to incur losses for the foreseeable future as it continues its research and development activities, pursues potential mergers and acquisitions, seeks product certification approvals in the territories it has identified, hires additional personnel, obtains and protects its intellectual property and incurs additional costs for commercialization or to expand its pipeline of waste materials it collects and the circular products it generates from the recycled waste collected from its customers with respect to its waste collection and disposal services.

To become and remain profitable, the Group must increase its operating capacity to treat higher volumes of wastes and succeed in developing and eventually commercializing circular products that can generate sufficient revenue. In that regard, the Group has commenced sales of Fluorspar and Kao Lin, materials generated from the wastes the Group collected.

In addition, the Group has not yet demonstrated an ability to successfully overcome many of the risks and uncertainties frequently encountered by companies in new and rapidly evolving fields, particularly in the environmental services industry. Because of these numerous risks and uncertainties, the Group is unable to accurately predict the timing or amount of increased expenses or when, or if, it will be able to achieve profitability. Even if the Group achieves profitability, it may not be able to sustain or increase profitability on a quarterly or annual basis. Its failure to become and remain profitable would depress the value of the Company and could impair the ability of the Company to raise capital, expand its business, maintain its research and development efforts, diversify its products, or even continue its operations. A decline in the value of the Company could also cause you to lose all or part of your investment.

The environmental services industry is highly competitive and includes competitors that may have greater financial and operational resources, flexibility to reduce prices or other competitive advantages that could make it difficult for the Group to compete effectively.

The Group principally competes with waste management companies who collect and dispose the waste the Group needs for its waste management and treatment processes. Competition for waste collection is typically based on factors such as geographic location, quality of services, ease of doing business and/or price. The Group ‘s competitors may have greater financial and operational resources than we do. They could also seek to gain market share by reducing the prices they charge customers, introducing products and solutions that are similar to the Group’s or introducing new technology tools. If the Group were to lose market share or if it were to lower prices to address competitive issues, it could negatively impact the Group’s consolidated financial position , results of operations and cash flows.

| 6 |

The Group requires a significant amount of capital to fund its operations and growth. If the Group cannot obtain sufficient capital on acceptable terms, its business, financial condition, and prospects may be materially and adversely affected.

The Group requires a significant amount of capital and resources for its operations and continued growth. The Group expects to make significant investments to develop new operating capabilities and technology, which are fundamental to the Group’s business operations and future growth. However, the Group cannot assure you that these investments will generate the optimal returns, if at all. To date, the Group has historically funded its cash requirements primarily through the issuance of ordinary shares, cash generated by operations and borrowings from banks. If these resources are insufficient to satisfy the Group’s cash requirements, the Group may seek to raise funds through additional equity offering or debt financing or additional bank facilities. The Group’s ability to obtain additional capital in the future, however, is subject to a number of uncertainties, including those relating to its future business development, financial condition, and results of operations, general market conditions for financing activities by companies in its industry, and macro-economic and other conditions. If the Group cannot obtain sufficient capital on acceptable terms to meet its capital needs, the Group may not be able to execute its growth strategies, and the Group’s business, financial condition, and prospects may be materially and adversely affected.

The Group did not meet its original revenue projection for the fiscal year ended 2023.

The projected revenues of the Group for fiscal year 2023 and the 6-month period ended June 30, 2024 were US$11.0 million and US$3.8 million respectively. The revenues of the Group for the fiscal year ended 2023 and half year ended June 30, 2024 were approximately US$6.2 million and US$3.8 million respectively. The Group did not meet its original 2023 revenue projection mainly due to a combination of several factors. Firstly, the merger with Genesis Unicorn Capital Corp, expected to strengthen the Group’s financial standing, resulted in lower-than-expected proceeds due to unprecedented high redemptions. This unexpected outcome had a notable impact on the Group’s revenue trajectory. Secondly, the Group faced challenges in meeting its funding requirement to enhance technologies and capacity, essential for effectively serving market needs. This limitation hindered the Group’s ability to capitalize on growth and innovation opportunities, consequently affecting revenue generation. Furthermore, geopolitical tensions and market volatility presented additional obstacles to revenue generation efforts. Lower manufacturing activity, potentially influenced by these external factors, led to reduced waste from customers, impacting revenue streams. Lastly, unexpected waste management regulatory changes in Singapore posed operational challenges, particularly in the final quarter of the financial year. Adapting to these regulatory shifts proved to be a complex task, affecting operational efficiency. Therefore, there can be no assurance that the Group’s actual financial results would meet the financial projections and there is a significant likelihood that the Group’s actual financial results over the time periods and under the scenarios covered by the projections would be materially different. At this time, the Group’s management estimates that the impact of the lack of funds for capital investments may continue in the near future and therefore, the Group may not be able to meet its original revenue projections for 2024, 2025 and/or 2026. The Group has not updated its projections due to uncertainties surrounding recent developments, their future outcomes, and their impact on the Group’s projections.

Fluctuations in prices for recyclable waste materials the Group collects from its customers and the circular products that it sells to local and international end users, traders or overseas refiners may adversely affect the Group’s revenue, operating income, and cash flows.

The Group collects a variety of recyclable waste materials from its customers and processes and transforms them into circular products for sale to local and international end users, traders or overseas refiners, and the Group may directly or indirectly receive proceeds from its waste collection services and the sale of circular products. The Group’s results of operations may be affected by changing prices or market requirements for the recyclable waste materials and the circular products. The resale and purchase prices of, and market demand for, the circular products can be volatile because of changes in economic conditions and numerous other factors beyond the Group’s control. These fluctuations may affect the cost of and demand for the Group’s services and the Group’s future revenue, operating income, and cash flows. For example, a decline in oil prices would have an adverse effect on the Company’s revenue.

The Group is also exposed to inflationary pressures and rising interest rates which may adversely affect the selling price of its circular products. If this causes purchasing demand from the Group’s customers for its circular products to reduce, the selling price of certain of the Group’s circular products such as copper and zinc could drop and reduce its revenue. Inflation has also resulted in higher costs for the maintenance of the Group’s equipment, higher electricity and fuel costs and freight and payroll costs, which had an adverse impact on the Group’s operating profit and operating profit margin. Moreover, certain suppliers who are affected by supply chain inflationary pressures may decide to reduce their production and as a result the volume of industrial waste that is generated and supplied to the Group may be reduced. Similarly, following the general decline in the spending power of consumers, the Group’s waste disposal customers which are mainly semi-conductor companies with products that are used in mobile devices to cars may also decide to reduce their production which in turn would lead to lower volumes of waste being disposed to the Group. Although increasing the selling price of the Group’s circular products could mitigate the impact of inflation, competitive pressures may constrain the Group’s ability to fully recover any increased costs in this way. In addition, efforts to mitigate the effect of inflation through continuous investments in waste treatment processes and software developments to automate, streamline and improve the productivity of the Group’s business operations may not be sufficient.

The Group may not be able to enhance its existing recycling, reuse, disposal and waste treatment solutions and develop new solutions in a timely manner.

The Group’s future operating results will depend, to a significant extent, on its ability to continue to provide efficient and innovative recycling, reuse, disposal and waste treatment services that compare favorably with alternative services on the basis of cost, performance, and customer preferences. The Group’s success in maintaining and growing with its existing customers and attracting new customers depends on various factors, including the following:

| ● | innovative development of new services for customers; | |

| ● | maintenance of quality standards; | |

| ● | efficient and cost-effective services; and | |

| ● | utilization of advances in technology. |

| 7 |

The Group’s inability to enhance its existing services and develop new services on a timely basis could harm its operating results and impede its growth.

The Group’s revenues, earnings and cash flows will fluctuate based on changes in commodity prices, and commodity prices for circular products are particularly susceptible to volatility based on regulations and tariffs that affect its ability to export products.

Enforcement or implementation of foreign and domestic regulations can affect the Group’s ability to export its circular products. In 2017, the Chinese government announced bans on certain scrap materials and begun to enforce extremely restrictive quality and other requirements, which significantly reduced China’s import of recyclables. As of January 1, 2021, China ceased importing virtually all recyclables, including those exported by the Group. Many other markets, both domestic and foreign, have also tightened their quality expectations and limited or restricted the import of certain circular products.

Such trade restrictions have disrupted the global trade of recyclables, creating excess supply and decreasing recyclable commodity prices. The Group has been actively working to identify alternative markets for recycling commodities, but there may not be demand for all of the circular products it produces. The heightened quality requirements have been difficult for the industry to achieve and have driven up operating costs. As prices of circular products have fallen and operating costs have increased, the Group and other recyclers are passing cost increases through to waste collection customers.

Fluctuation in energy prices also affects the Group’s business, including recycling of plastics manufactured from petroleum products. Significant variations in the price of methane gas, electricity and other energy- related products can result in a corresponding significant impact to the Group’s revenue from yield from such operations. Any of the commodity prices to which the Group is subject may fluctuate substantially and without notice in the future.

Acute and chronic weather events, including those brought about by climate change, may limit the Group’s operations and increase the costs of collection, transfer, disposal, and other environmental services it provides.

The Group’s operations could be adversely impacted by extreme weather events, changing weather patterns, and rising mean temperature and sea levels, some of which the Group is already experiencing. The Intergovernmental Panel on Climate Change, which includes more than 1,300 scientists from the United States and other countries, forecasts a temperature rise of 2.5° to 10° Fahrenheit over the next century. Changing weather patterns and rising temperatures are expected to result in more severe heat waves, fires, storms, and other extreme weather events. Any of these extreme weather events such as flash flooding in Singapore could significantly decrease the volume of waste material the Group collects from its waste disposal customers and suppliers of industrial waste as they may be required to temporarily cease or suspend their business activities, thereby reducing the volume of waste they generate. Other than the Group’s customers and suppliers, such adverse weather conditions may also result in the temporary suspension of the Group’s business operations, ability to utilize the Group’s normal commercial channels and supply chain, and the incursion of significant costs to repair its fixtures, equipment and property, all of which could significantly affect the Company’s operating results during those periods.

The Group’s businesses are subject to operational and safety risks.

Providing waste management, treatment and recycling services to the Group’s customers involves risks such as equipment defects, malfunctions and failures and natural disasters, which could potentially result in releases of hazardous materials, damage to or total loss of the Group’s property or assets, injury or death of the Group’s employees or a need to shut down or reduce operations of the Group’s facilities while remedial actions are undertaken. The Group’s employees and logistics providers, when necessary, often work under potentially hazardous conditions. These risks expose the Group to potential liability for pollution and other environmental damages, personal injury, loss of life, business interruption and property damage or destruction. The Group must also maintain a solid safety record in order to remain a preferred supplier to its major customers. While the Group seeks to minimize its exposure to such risks primarily through entering and maintaining various insurance policies in relation to the business, operations, employees and assets of ESA, such actions and insurance may not be adequate to cover all of the Group’s potential liabilities which could negatively impact its results of operations and cash flows.

| 8 |

The Group’s insurance coverage and self-insurance reserves may be inadequate to cover all significant risk exposures, and increasing costs to maintain adequate coverage may significantly impact the Group’s financial condition and results of operations.

The Group carries a range of insurance policies intended to protect its assets and operations, including general liability insurance, property damage, business interruption and environmental risk insurance. While the Group endeavors to purchase insurance coverage appropriate to its risk assessment, it is unable to predict with certainty the frequency, nature or magnitude of claims for direct or consequential damages, and as a result the Group’s insurance program may not fully cover itself for losses it may incur.

As a result of a number of catastrophic weather and other events, insurance companies have incurred substantial losses and in many cases they have substantially reduced the nature and amount of insurance coverage available to the market, have broadened exclusions and/or have substantially increased the cost of such coverage. If this trend continues, the Group may not be able to maintain insurance of the types and coverage it desires at reasonable rates. A partially or completely uninsured claim against the Group (including liabilities associated with cleanup or remediation), if successful and of sufficient magnitude, could have a material adverse effect on the Group’s business, financial condition and results of operations. Any future difficulty in obtaining insurance could also impair the Group’s ability to secure future contracts, which may be conditional upon the availability of adequate insurance coverage. In addition, claims associated with risks for which the Group is to some extent self-insured (property, workers’ compensation, employee medical, comprehensive general liability and vehicle liability) may exceed the Group’s recorded reserves, which could negatively impact future earnings.

The Group may have environmental liabilities that are not covered by its insurance. Changes in insurance markets also may impact its financial results.

The Group may incur environmental liabilities arising from its operations or properties. The Group maintains high deductibles for its environmental liability insurance coverage. If the Group was to incur substantial liability for environmental damage, its insurance coverage may be inadequate to cover such liability. This could have a material adverse effect on the Group’s consolidated financial condition, results of operations and cash flows.

Also, due to the variable condition of the insurance market, the Group has experienced, and may experience in the future, increased insurance retention levels and increased premiums or unavailability of insurance. As the Group assumes more risk for insurance through higher retention levels, the Group may experience more variability in its insurance reserves and expense.

The Group depends on key personnel who would be difficult to replace, and its business will likely be harmed if it loses their services or cannot hire additional qualified personnel.

The Group’s success depends, to a significant extent, upon the continued services of its current management team and key personnel. The loss of one or more of its key executives or employees could have a material adverse effect on its business. The Group does not maintain “key person” insurance policies on the lives of any of its executives or any of its other employees. The Group employs all of its executives and key employees on an at-will basis, and their employment can be terminated by the Group or them at any time, for any reason, and without notice, subject, in certain cases, to severance payment rights.

The Group’s success also depends on its ability to attract, retain, and motivate additional skilled management personnel. The Group plans to continue to expand its work force to continue to enhance its business and operating results. The Group believes that there is significant competition for qualified personnel with the skills and knowledge that it requires. Many of the other companies with which the Group competes for qualified personnel have substantially greater financial and other resources than the Group does. They also may provide more diverse opportunities and better chances for career advancement. Some of these characteristics may be more appealing to high-quality candidates than those which the Group has to offer. If the Group is not able to retain its current key personnel or attract the necessary qualified key personnel to accomplish its business objectives, it may experience constraints that will significantly impede the achievement of its business objectives and its ability to pursue its business strategy. New hires require significant training and, in most cases, take significant time before they achieve full productivity. New employees may not become as productive as the Group expects, and the Group may be unable to hire or retain sufficient numbers of qualified individuals. If the Group’s recruiting, training, and retention efforts are not successful or do not generate a corresponding increase in revenue, the Group’s business will be harmed.

| 9 |

General economic conditions can directly and adversely affect revenues for environmental services and the Group’s income from operations margins.

The Group’s business is directly affected by changes in national and general economic factors that are outside of the Group’s control, including consumer confidence, interest rates and access to global markets. A weak economy generally results in decreases in volumes of waste generated, which negatively impacts the ability to grow through new business or service upgrades, and may result in customer turnover and reduction in the waste service needs of the Group’s customers and the demand for circular products from end users, traders or overseas refiners. Consumer uncertainty and the loss of consumer confidence may also reduce the number and variety of services and/or circular products requested by customers. This decrease in demand can negatively impact commodity prices and the Group’s operating income and cash flows.

The Group could become involved in litigation matters that may be expensive and time consuming, and, if resolved adversely, could harm its business, financial condition, or results of operations.

Although the Group is not currently involved in any litigation matters, any such litigation to which it is a party may result in an onerous or unfavorable judgment that may not be reversed upon appeal, or the Group may decide to settle lawsuits on similarly unfavorable terms. Any negative outcome could result in payments of substantial monetary damages or fines, or changes to the Group’s products or business practices, and accordingly the Group’s business, financial condition, or results of operations could be materially and adversely affected.

The Group could be required to make immediate repayment of certain of its outstanding debt with financial institutions.

As of December 31, 2023 and June 30, 2024, the Group has certain borrowings with outstanding balances of approximately US$5.7 million and US$4.7 million respectively classified as current liabilities, as the relevant loan agreements the Group entered into with the lenders provide them discretion to demand immediate repayment of the outstanding balances from us. In addition, as of the date of this prospectus, the Group had obtained waivers from the relevant lenders in relation to certain terms and conditions under the relevant loan agreements in connection with the closing of the Business Combination, except for Term Loan IV with an outstanding balance of approximately S$499,000 (US$378,000) as of December 31, 2023 from the relevant bank (the “Relevant Bank”). On July 20, 2022, the Group had obtained a written consent from the Relevant Bank for, among other things, the undertaking of a proposed restructuring of the Group. Subsequently on January 17, 2023, the Group had requested a waiver from the Relevant Bank for the closing of the Business Combination. As of the date of this prospectus, the Group had not obtained the waiver or any notice from the Relevant Bank objecting, disagreeing to the matter or demanding any immediate repayment of Term Loan IV in connection with the closing of the Business Combination.

Notwithstanding the above, the lenders could demand immediate repayment of the outstanding balances from the Group for the borrowings classified as current liabilities and it may be unable to repay, negotiate, extend or refinance the bank borrowings on favorable terms or at all, which may have a material adverse effect on its business, results of operations and financial position. If the Group fails to repay certain of the bank borrowings, some lenders could enforce their security interests under the relevant loan agreements and take possession of the Group’s leasehold land and buildings where it operates its business, thereby resulting in a material adverse effect on the Group’s business, results of operations and financial condition. See Note 17 to the Group’s financial statements for further information on the Group’s outstanding debt with financial institutions.

| 10 |

The Group’s strategy includes an increasing dependence on technology in its operations. If any of its key technology fails, its business could be adversely affected.

The Group’s operations are increasingly dependent on technology. The Group’s information technology systems are critical to its ability to drive profitable growth, implement standardized processes and deliver a consistent customer experience. Problems with the operation of the information or communication technology systems it uses could adversely affect, or temporarily disable, all or a portion of the Group’s operations. Inabilities and delays in implementing new systems can also affect its ability to realize projected or expected revenue or cost savings. Further, any systems failures could impede its ability to timely collect and report financial results in accordance with applicable laws.

Emerging technologies represent risks, as well as opportunities, to the Group’s current business model. The costs associated with developing or investing in emerging technologies could require substantial capital and adversely affect the Group’s results of operations and cash flows. Delays in the development or implementation of such emerging technologies and difficulties in marketing new products or services based on emerging technologies could have similar negative impacts. The Group’s financial results may suffer if it is not able to develop or license emerging technologies, or if a competitor obtains exclusive rights to an emerging technology that disrupts the current methods used in the environmental services industry.

A cyber security incident could negatively impact the Group’s business and its relationships with customers.

The Group uses information technology, including computer and information networks, in substantially all aspects of its business operations. The Group also use mobile devices, social networking and other online activities to connect with its employees and its customers. Such uses give rise to cyber security risks, including security breach, espionage, system disruption, theft and inadvertent release of information. The Group’s business involves the storage and transmission of numerous classes of sensitive and/or confidential information and intellectual property, including customers’ personal information, private information about employees, and financial and strategic information about the Group and its business partners. In connection with its strategy to grow through acquisitions and to pursue new initiatives that improve its operations and cost structure, the Group is also expanding and improving its information technologies, resulting in a larger technological presence and corresponding exposure to cyber security risk. If the Group fails to assess and identify cyber security risks associated with acquisitions and new initiatives, it may become increasingly vulnerable to such risks. Additionally, while the Group has implemented measures to prevent security breaches and cyber incidents, its preventive measures and incident response efforts may not be entirely effective. Also, the regulatory environment surrounding information security and privacy is increasingly demanding, with the frequent imposition of new and constantly changing requirements. This changing regulatory landscape may cause increasingly complex compliance challenges, which may increase the Group’s compliance costs. Any failure to comply with these changing security and privacy laws and regulations could result in significant penalties, fines, legal challenges and reputational harm. The theft, destruction, loss, misappropriation, or release of sensitive and/or confidential information or intellectual property, or interference with the Group’s information technology systems or the technology systems of third parties on which it relies, could result in business disruption, negative publicity, brand damage, violation of privacy laws, loss of customers, potential liability and competitive disadvantage.

The Group may be subject to intellectual property claims that create uncertainty about ownership of technology essential to its business and divert its managerial and other resources.

The Group can provide no assurance that third parties will not claim infringement by it with respect to its current or future services, trademarks, or other proprietary rights. The Group’s success depends, in part, on its ability to protect its intellectual property and to operate without infringing the intellectual property rights of others in the process. There can be no assurance that any of its intellectual property will be adequately safeguarded or that it will not be challenged by third parties. The Group may be subject to intellectual property infringement claims that would be costly to defend, could limit its ability to use certain critical technologies, and may divert its technical and management personnel from their normal responsibilities. The Group may not prevail in any of these suits. An adverse determination of any litigation or defense proceedings could cause the Group to pay substantial damages, including treble damages, if it willfully infringes and also could increase the risk of its patent applications not being issued.

| 11 |

Furthermore, because of the substantial amount of discovery required in connection with intellectual property litigation, there is a risk that some of the Group’s confidential information could be compromised by disclosure during this type of litigation. In addition, during the course of this kind of litigation, there could be public announcements of the results of hearings, motions, or other interim proceedings or developments in the litigation. If these results are perceived to be negative, it could have an adverse effect on the Group’s business.

Changes in policies imposed by governments may impact on the availability and costs of employing non-Singapore workers.

The Group is dependent on non-Singapore workers for its business operations. The Group’s ability to meet its labor requirements for operational needs is subject to various factors, including changes in the labor policies of such foreign workers’ countries of origin or the policies imposed by Ministry of Manpower (“MOM”) in Singapore. The Group is therefore vulnerable to any shortage in the supply of foreign workers and any increase in the cost of foreign labor, the occurrence of which would adversely affect its business and financial performance.

Government policies affecting labor costs include, inter alia, the new progressive wage model (“PWM”) and foreign worker levies. Changes in these policies may lead to an increase in the Group’s labor costs which may result in its business, financial condition and results of operations being materially and adversely affected. The Group is subject to foreign worker levies for the foreign workers it hires. The Group paid foreign worker levies in the amount of US$168,137 and US$97,703 for the two fiscal years ended December 31, 2023 and 2022, respectively.

The foreign worker levies applicable to the Group will differ according to the percentage of the Group’s total workforce comprising of foreign workers. As of April 16, 2024, approximately 64.7% of the Group’s total workforce is comprised of foreign workers for whom it might have to pay such foreign worker levies. Further, the criteria for applying for certain foreign work permits will be tightened moving forward and there will be increase in foreign worker levies. There is no assurance that the Singapore Government will not further increase the levy rates in future, and if they do so, the Group may face a significant increase in labor costs.

In January 2022, the National Environment Agency (“NEA”) and MOM announced a new waste management PWM with a six (6) year schedule of sustained PWM wage increases from 2023 to 2028 and a mandatory annual PWM bonus for eligible workers from January 2024. Under the new PWM wage schedule, the monthly baseline wage of an entry-level waste collection crew worker is expected to increase from S$2,210 in 2023 to S$3,260 in 2028 or possibly sooner. The implementation of and revisions to the PWM has increased the Group’s labor costs and there is no assurance that the Singapore government will not revise the PWM to further increase the base salaries beyond 2028.

The Group is exposed to environmental liability.

The Group’s business operations are subject to environmental laws and regulations in Singapore, in particular on the disposal and treatment of industrial and toxic waste and obligations to protect public health and the environment. While the Group has not had any material non-compliance with applicable environmental laws and regulations to date, there is no assurance that it will continue to be in compliance with all the applicable laws and regulations, and the Group may incur additional costs in complying with such laws and regulations. Any violation of the relevant environmental laws and regulations may lead to substantial fines, costs for implementation of preventive or corrective measures, clean-up costs or even suspension of operations that could materially and adversely affect the Group’s business, operations, financial performance, financial condition, results of operations and/or prospects.

The Group is exposed to the risk of non-renewal, non-granting or suspension of its licenses, permits and accreditations that are required to operate its business.

The waste management industry in Singapore in which the Group operates in is highly regulated. The Group’s licenses and registrations are subject to periodic renewal by the relevant government authorities and are generally subject to a variety of conditions which are stipulated either within the licenses and registrations themselves, or under the particular laws and/or regulations issued by the competent authorities. Failure to comply with such conditions, laws or regulations could result in the revocation, non-renewal or downgrade of the relevant licenses, permits or accreditations and/or imposition of penalties. In such an event, the Group’s business and financial performance will be adversely affected.

| 12 |

Developments in the social, political, regulatory and economic environment in the country where the Group operates, may have a material and adverse impact on the Group.

The Group’s business, prospects, financial condition and results of operations may be adversely affected by social, political, regulatory and economic developments in the country in which the Group operates. Such political and economic uncertainties include, but are not limited to, the risks of war, terrorism, nationalism, nullification of contract, changes in interest rates, imposition of capital controls and methods of taxation. For example, all of the Group’s current operations are located in Singapore, and negative developments in Singapore’s socio-political environment may adversely affect the Group’s business, financial condition, results of operations and prospects.

Disruptions in the international trading environment may seriously decrease the Group’s international sales outside Singapore.

The success and profitability of the Group’s international activities depends on factors such as general economic conditions, labor conditions, political stability, macro-economic regulating measures, tax laws, import and export duties, transportation difficulties, fluctuation of local currency and foreign exchange controls of the countries in which the Group sells its services, as well as the political and economic relationships in Singapore where the Group sources waste materials and jurisdictions where the Group’s end users, traders or overseas refiners are located. As a result, the Group’s sales are vulnerable to disruptions in the international trading environment, including adverse changes in foreign government regulations, political unrest and international economic downturns. Any disruptions in the international trading environment may affect the demand for the Group’s products, which could impact its business, financial condition and results of operations.

Many of the economies in Asia are experiencing substantial inflationary pressures which may prompt the governments to take action to control the growth of the economy and inflation that could lead to a significant decrease in the Group’s profitability.

While many of the economies in Asia have experienced rapid growth over the last two decades, they currently are experiencing inflationary pressures, and the rate of growth is slowing down. The economy in Singapore and globally has experienced general increases in certain operating costs and expenses, such as employee compensation and office operating expenses, as a result of higher inflation. Average wages in Singapore are expected to continue to increase and the Group expects that its employee costs, including wages and employee benefits, will continue to increase. Unless the Group is able to control its employee costs or pass them on to its clients, the Group’s financial condition, and results of operations may be adversely affected.

As governments in Asia (and worldwide) take steps to address current inflationary pressures, there may be significant changes in the availability of bank credit, commercial reasonability of interest rates, limitations on loans, restrictions on currency conversions and foreign investment rules, thereby restricting the availability of credit and reducing economic growth. Inflation, actions that may be implemented to combat inflation and public speculation about any possible additional actions also may contribute materially to economic uncertainty in Asia (and worldwide) and accordingly weaken investor confidence, thus adversely impacting economic growth and causing decreased economic activity, which in turn could lead to a reduction in demand for the Group’s products and services, and consequently have a material adverse effect on the Group’s businesses, financial condition and results of operations. Conversely, more lenient government policies and interest rate decreases may trigger increases in inflation and, consequently, growth volatility and the need for sudden and significant interest rate increases, which could negatively affect the Group’s business. There also may be imposition of price controls. If prices for the Group’s waste disposal services and/or circular products rise at a rate that is insufficient to compensate for the rise in the costs of supplies and operations, it may have an adverse effect on the Group’s profitability. If these or other similar restrictions are imposed by a government to influence the economy, it may lead to a slowing of economic growth.

| 13 |

Cayman Islands economic substance requirements may have an effect on the Group’s business and operations.

Pursuant to the International Tax Cooperation (Economic Substance) Act (As Revised) of the Cayman Islands (“ES Act”) that came into force on 1 January 2019, a “relevant entity” is required to satisfy the economic substance test set out in the ES Act. A “relevant entity” includes an exempted company incorporated in the Cayman Islands as is the Company; however, it does not include an entity that is tax resident outside the Cayman Islands. Accordingly, for so long as the Company is a tax resident outside the Cayman Islands, it is not required to satisfy the economic substance test set out in the ES Act.

Risks Relating to our Securities

Although as a foreign private issuer, ESGL is exempt from certain corporate governance standards applicable to US domestic issuers, if ESGL cannot continue to satisfy the continued listing requirements and other rules of Nasdaq, ESGL’s securities may not be listed or may be delisted, which could negatively affect the price of its securities and your ability to sell them.

ESGL’s securities currently list on Nasdaq. ESGL cannot assure you that its securities will continue to be listed on Nasdaq. In order to maintain its listing on Nasdaq, ESGL is required to comply with certain rules of Nasdaq, including those regarding minimum shareholders’ equity, minimum share price, minimum market value of publicly held shares, and various additional requirements.

If Nasdaq subsequently delists its securities from trading, ESGL could face significant consequences, including:

| ● | a limited availability for market quotations for its securities; | |

| ● | reduced liquidity with respect to its securities; | |

| ● | a determination that the Ordinary Shares are a “penny stock,” which will require brokers trading in the Ordinary Shares to adhere to more stringent rules and possibly result in a reduced level of trading activity in the secondary trading market for the Ordinary Shares; | |

| ● | limited amount of news and analyst coverage; and | |

| ● | a decreased ability to issue additional securities or obtain additional financing in the future. |

Currently, our Ordinary Shares and Warrants are listed on the Nasdaq Capital Market. However, there may not be enough liquidity in such market to enable shareholders to sell their securities.

Currently, our Ordinary Shares and Warrants are listed on the Nasdaq Capital Market. If a public market for our securities does not develop, investors may not be able to re-sell their Ordinary Shares or Warrants, rendering their shares illiquid and possibly resulting in a complete loss of their investment. We cannot predict the extent to which investor interest in us will lead to the development of an active, liquid trading market. The trading price of and demand for the Ordinary Shares and the development and continued existence of a market and favorable price for the Ordinary Shares will depend on a number of conditions, including the development of a market following, including by analysts and other investment professionals, the businesses, operations, results, and prospects of the Group, general market and economic conditions, governmental actions, regulatory considerations, legal proceedings, and developments or other factors. These and other factors may impair the development of a liquid market and the ability of investors to sell shares at an attractive price. These factors also could cause the market price and demand for the Ordinary Shares of the Group to fluctuate substantially, which may limit or prevent investors from readily selling their shares and may otherwise affect negatively the price and liquidity of the Ordinary Shares. Many of these factors and conditions are beyond the control of the Group or the shareholders.

We do not anticipate that we will pay dividends on our Ordinary Shares and, consequently, your ability to achieve a return on your investment will depend on appreciation in the price of Ordinary Shares.

We intend to retain any earnings to finance the operation and expansion of its business, and we do not anticipate paying any cash dividends in the foreseeable future. In addition, in the future we may enter into agreements that prohibit or restrict its ability to declare or pay dividends on our Ordinary Shares. As a result, you may only receive a return on your investment in our Ordinary Shares if the market price of such shares increases.

| 14 |

Certain judgments obtained against us by our shareholders may not be enforceable.

We are an exempted company incorporated under the laws of the Cayman Islands. The Group conducts most of its operations in Singapore and substantially all of its operations outside of the United States. Substantially all of the Group’s assets are located outside of the United States. In addition, all of our senior executive officers reside outside the United States. Substantially all of the assets of these persons are located outside the United States. As of the date of this prospectus, there are no officers, directors, or director nominees residing in China or Hong Kong, except for Lim Boon Yew Gary, who is one of our independent directors and resides in Hong Kong. A judgment of a court in the United States predicated upon U.S. federal or state securities laws may be enforced in Hong Kong at common law by bringing an action in a Hong Kong court on that judgment for the amount due thereunder, and then seeking summary judgment on the strength of the foreign judgment, provided that the foreign judgment, among other things, is (1) for a debt or a definite sum of money; (2) made by a court of competent jurisdiction over the parties and the subject matter; (3) between the same parties on an identical issue; (4) final and conclusive on the merits; and (5) not impeachable according to the rules on conflicts of laws of Hong Kong. Such a judgment may not, in any event, be so enforced in Hong Kong if (a) it was obtained by fraud; (b) the proceedings in which the judgment was obtained were opposed to natural justice; or (c) its enforcement or recognition would be contrary to the public policy of Hong Kong. It will be costlier and more time-consuming for the investors to effect service of process outside the United States, or to enforce judgments obtained from the U.S. courts in the courts of the jurisdictions where our directors and officers reside. For example, to enforce a foreign judgment in Hong Kong, the applicant will be required to apply to the Hong Kong High Court to enforce a foreign judgment (the “Application”) for which the applicant will be required to (i) engage a local counsel to facilitate or prepare the Application; and (ii) go through the standard litigation process to sue on the judgment as a debt. In addition, a judgment of a United States court for civil liabilities predicated upon the federal securities laws of the United States may also not be enforceable in or recognized by the courts of the jurisdictions where our directors and officers reside.

Furthermore, as of the date of this prospectus, most of officers, directors, or director nominees reside in Singapore. It is possible that the Singapore courts may not (i) recognize and enforce judgments of courts in the United States, based upon the civil liability provisions of the securities laws of the United States or any state or territory of the United States (ii) enter judgments in original actions brought in the Singapore courts based solely on the civil liability provisions of these securities laws. An in personam final and conclusive judgment in the federal or state courts of the United States under which a fixed or ascertainable sum of money is payable may be enforced as a debt in the Singapore courts under the common law as long as it is (i) from a court of competent jurisdiction in the United States and (ii) final and conclusive on the merits under the laws of the United States. Additionally, the court where the judgment was obtained must have had international jurisdiction over the party sought to be bound in the local proceedings. However, the Singapore courts are unlikely to enforce a foreign judgment if (a) the foreign judgment is inconsistent with a prior local judgment that is binding on the same parties; (b) the enforcement of the foreign judgment would contravene the public policy of Singapore; (c) the proceedings in which the foreign judgment was obtained were contrary to principles of natural justice; (d) the foreign judgment was obtained by fraud; or (e) the enforcement of the foreign judgment amounts to the direct or indirect enforcement of a foreign penal, revenue or other public law. As a result, it may be difficult or impossible for you to bring an action against us or against these individuals in the United States in the event that you believe that your rights have been infringed under the U.S. federal securities laws or otherwise. Even if you are successful in bringing an action of this kind, the laws of the Cayman Islands, Singapore, and Hong Kong may render you unable to enforce a judgment against our assets or the assets of our directors and officers. For more information regarding the relevant laws of the Cayman Islands and Singapore, see “Comparison of Stockholders’ Rights — Enforceability of Civil Liabilities under the U.S. Securities Laws.”

Our share price may be volatile and could decline substantially.