00016944262023FYFALSE33.33http://fasb.org/us-gaap/2023#CostOfRevenuehttp://fasb.org/us-gaap/2023#CostOfRevenuehttp://fasb.org/us-gaap/2023#CostOfRevenuehttp://fasb.org/us-gaap/2023#CostOfRevenuehttp://fasb.org/us-gaap/2023#CostOfRevenuehttp://fasb.org/us-gaap/2023#CostOfRevenuehttp://fasb.org/us-gaap/2023#OtherLiabilitiesCurrenthttp://fasb.org/us-gaap/2023#AccruedEnvironmentalLossContingenciesNoncurrentP3YP3Yhttp://fasb.org/us-gaap/2023#OtherOperatingIncomeExpenseNethttp://fasb.org/us-gaap/2023#OtherOperatingIncomeExpenseNethttp://fasb.org/us-gaap/2023#OtherOperatingIncomeExpenseNethttp://fasb.org/us-gaap/2023#OtherOperatingIncomeExpenseNethttp://fasb.org/us-gaap/2023#OtherOperatingIncomeExpenseNethttp://fasb.org/us-gaap/2023#OtherOperatingIncomeExpenseNetP1Y00016944262023-01-012023-12-3100016944262023-06-30iso4217:USD00016944262024-02-21xbrli:shares00016944262023-10-012023-12-3100016944262023-12-3100016944262022-12-31iso4217:USDxbrli:shares00016944262022-01-012022-12-3100016944262021-01-012021-12-310001694426us-gaap:CommonStockMember2020-12-310001694426us-gaap:AdditionalPaidInCapitalMember2020-12-310001694426us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001694426us-gaap:RetainedEarningsMember2020-12-310001694426us-gaap:TreasuryStockCommonMember2020-12-310001694426us-gaap:NoncontrollingInterestMember2020-12-3100016944262020-12-310001694426us-gaap:RetainedEarningsMember2021-01-012021-12-310001694426us-gaap:NoncontrollingInterestMember2021-01-012021-12-310001694426us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001694426us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001694426us-gaap:CommonStockMember2021-01-012021-12-310001694426us-gaap:CommonStockMember2021-12-310001694426us-gaap:AdditionalPaidInCapitalMember2021-12-310001694426us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001694426us-gaap:RetainedEarningsMember2021-12-310001694426us-gaap:TreasuryStockCommonMember2021-12-310001694426us-gaap:NoncontrollingInterestMember2021-12-3100016944262021-12-310001694426us-gaap:RetainedEarningsMember2022-01-012022-12-310001694426us-gaap:NoncontrollingInterestMember2022-01-012022-12-310001694426us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310001694426us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001694426us-gaap:CommonStockMember2022-01-012022-12-310001694426dk:IEPEnergyHoldingLLCMemberus-gaap:CommonStockMember2022-01-012022-12-310001694426dk:IEPEnergyHoldingLLCMemberus-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001694426dk:IEPEnergyHoldingLLCMemberus-gaap:RetainedEarningsMember2022-01-012022-12-310001694426dk:IEPEnergyHoldingLLCMember2022-01-012022-12-310001694426us-gaap:CommonStockMember2022-12-310001694426us-gaap:AdditionalPaidInCapitalMember2022-12-310001694426us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001694426us-gaap:RetainedEarningsMember2022-12-310001694426us-gaap:TreasuryStockCommonMember2022-12-310001694426us-gaap:NoncontrollingInterestMember2022-12-310001694426us-gaap:RetainedEarningsMember2023-01-012023-12-310001694426us-gaap:NoncontrollingInterestMember2023-01-012023-12-310001694426us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310001694426us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310001694426us-gaap:CommonStockMember2023-01-012023-12-310001694426us-gaap:CommonStockMember2023-12-310001694426us-gaap:AdditionalPaidInCapitalMember2023-12-310001694426us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-310001694426us-gaap:RetainedEarningsMember2023-12-310001694426us-gaap:TreasuryStockCommonMember2023-12-310001694426us-gaap:NoncontrollingInterestMember2023-12-31dk:business_linedk:segment0001694426dk:OneCustomerMemberus-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMember2023-01-012023-12-31xbrli:pure0001694426us-gaap:AccountsReceivableMemberdk:TwoCustomersMemberus-gaap:CustomerConcentrationRiskMember2022-01-012022-12-310001694426dk:OneCustomerMemberus-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMember2023-01-012023-12-310001694426dk:OneCustomerMemberus-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMember2022-01-012022-12-310001694426us-gaap:BuildingAndBuildingImprovementsMembersrt:MinimumMember2023-12-310001694426us-gaap:BuildingAndBuildingImprovementsMembersrt:MaximumMember2023-12-310001694426srt:MinimumMemberdk:RefineryMachineryAndEquipmentMember2023-12-310001694426srt:MaximumMemberdk:RefineryMachineryAndEquipmentMember2023-12-310001694426srt:MinimumMemberdk:PipelinestanksandterminalsMember2023-12-310001694426srt:MaximumMemberdk:PipelinestanksandterminalsMember2023-12-310001694426srt:MinimumMemberdk:RetailStoreEquipmentandSiteImprovementsMember2023-12-310001694426srt:MaximumMemberdk:RetailStoreEquipmentandSiteImprovementsMember2023-12-310001694426srt:MinimumMemberdk:RefineryTurnaroundCostsMember2023-12-310001694426srt:MaximumMemberdk:RefineryTurnaroundCostsMember2023-12-310001694426us-gaap:AutomobilesMembersrt:MinimumMember2023-12-310001694426us-gaap:AutomobilesMembersrt:MaximumMember2023-12-310001694426srt:MinimumMemberus-gaap:ComputerEquipmentMember2023-12-310001694426srt:MaximumMemberus-gaap:ComputerEquipmentMember2023-12-310001694426srt:MinimumMemberus-gaap:FurnitureAndFixturesMember2023-12-310001694426srt:MaximumMemberus-gaap:FurnitureAndFixturesMember2023-12-310001694426us-gaap:AssetRetirementObligationCostsMembersrt:MinimumMember2023-12-310001694426us-gaap:AssetRetirementObligationCostsMembersrt:MaximumMember2023-12-310001694426srt:MinimumMember2023-12-310001694426srt:MaximumMember2023-12-310001694426srt:MinimumMember2023-01-012023-12-310001694426srt:MaximumMember2023-01-012023-12-310001694426dk:DelawareGatheringMember2022-06-010001694426dk:DelawareGatheringAcquisitionMember2022-06-012022-06-010001694426dk:DelawareGatheringAcquisitionMember2022-06-010001694426dk:RefiningMember2023-01-012023-12-31dk:facility00016944262020-05-07dk:store0001694426us-gaap:OperatingSegmentsMemberdk:RefiningMember2023-01-012023-12-310001694426dk:LogisticsMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310001694426dk:RetailSegmentMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310001694426us-gaap:CorporateNonSegmentMember2023-01-012023-12-310001694426us-gaap:IntersegmentEliminationMemberdk:RefiningMember2023-01-012023-12-310001694426us-gaap:IntersegmentEliminationMemberdk:LogisticsMember2023-01-012023-12-310001694426dk:RetailSegmentMemberus-gaap:IntersegmentEliminationMember2023-01-012023-12-310001694426us-gaap:IntersegmentEliminationMember2023-01-012023-12-310001694426us-gaap:OperatingSegmentsMemberdk:RefiningMember2022-01-012022-12-310001694426dk:LogisticsMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310001694426dk:RetailSegmentMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310001694426us-gaap:CorporateNonSegmentMember2022-01-012022-12-310001694426us-gaap:IntersegmentEliminationMemberdk:RefiningMember2022-01-012022-12-310001694426us-gaap:IntersegmentEliminationMemberdk:LogisticsMember2022-01-012022-12-310001694426dk:RetailSegmentMemberus-gaap:IntersegmentEliminationMember2022-01-012022-12-310001694426us-gaap:IntersegmentEliminationMember2022-01-012022-12-310001694426us-gaap:OperatingSegmentsMemberdk:RefiningMember2021-01-012021-12-310001694426dk:LogisticsMemberus-gaap:OperatingSegmentsMember2021-01-012021-12-310001694426dk:RetailSegmentMemberus-gaap:OperatingSegmentsMember2021-01-012021-12-310001694426us-gaap:CorporateNonSegmentMember2021-01-012021-12-310001694426us-gaap:IntersegmentEliminationMemberdk:RefiningMember2021-01-012021-12-310001694426us-gaap:IntersegmentEliminationMemberdk:LogisticsMember2021-01-012021-12-310001694426dk:RetailSegmentMemberus-gaap:IntersegmentEliminationMember2021-01-012021-12-310001694426us-gaap:IntersegmentEliminationMember2021-01-012021-12-3100016944262020-05-072020-05-070001694426dk:StockCompensationPlanExcludingLossMember2023-01-012023-12-310001694426dk:StockCompensationPlanExcludingLossMember2022-01-012022-12-310001694426dk:StockCompensationPlanExcludingLossMember2021-01-012021-12-310001694426dk:StockCompensationPlanLossMember2023-01-012023-12-310001694426dk:StockCompensationPlanLossMember2022-01-012022-12-310001694426dk:StockCompensationPlanLossMember2021-01-012021-12-310001694426us-gaap:StockCompensationPlanMember2023-01-012023-12-310001694426us-gaap:StockCompensationPlanMember2022-01-012022-12-310001694426us-gaap:StockCompensationPlanMember2021-01-012021-12-310001694426dk:DelekLogisticsMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-01-012023-12-310001694426dk:DelekLogisticsMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001694426dk:DelekLogisticsMember2023-01-012023-12-3100016944262022-11-140001694426dk:ATMProgramMember2022-01-012022-12-310001694426dk:ATMProgramMember2023-01-012023-12-3100016944262022-04-1400016944262021-12-200001694426dk:DelekLogisticsPartnersLPMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001694426dk:DelekLogisticsPartnersLPMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-310001694426dk:DelekLogisticsPartnersLPMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMemberus-gaap:NonrelatedPartyMember2023-12-310001694426dk:DelekLogisticsPartnersLPMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMemberus-gaap:NonrelatedPartyMember2022-12-310001694426us-gaap:RelatedPartyMemberdk:DelekLogisticsPartnersLPMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001694426us-gaap:RelatedPartyMemberdk:DelekLogisticsPartnersLPMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-310001694426dk:W2WHoldingsLLCMember2023-12-310001694426dk:WinktoWebsterPipelineLLCMember2021-09-300001694426dk:WinktoWebsterPipelineLLCMember2021-09-302021-09-300001694426dk:WinktoWebsterPipelineLLCMember2021-01-012021-12-310001694426dk:WinktoWebsterPipelineLLCMember2023-12-310001694426dk:WinktoWebsterPipelineLLCMember2022-12-310001694426dk:DelekLogisticsPartnersLPMemberdk:RedRiverPipelineCompanyLLCMember2023-12-310001694426dk:DelekLogisticsPartnersLPMemberdk:RedRiverPipelineCompanyLLCMember2022-12-310001694426dk:DelekLogisticsPartnersLPMemberdk:PlainsAllAmericanPipelineAndAndeavorLogisticsMember2023-01-012023-12-31dk:jointVenture0001694426dk:DelekLogisticsPartnersLPMemberdk:PlainsAllAmericanPipelineMember2023-12-310001694426dk:DelekLogisticsPartnersLPMemberdk:AndeavorLogisticsMember2023-12-310001694426dk:DelekLogisticsPartnersLPMemberdk:PlainsAllAmericanPipelineAndAndeavorLogisticsMember2023-12-310001694426dk:DelekLogisticsPartnersLPMemberdk:PlainsAllAmericanPipelineAndAndeavorLogisticsMember2022-12-310001694426dk:AsphaltTerminalJointVentureMember2023-12-310001694426dk:EthanolUnitTrainFacilityAndTankJointVentureMember2023-12-310001694426dk:OtherJointVentureInvestmentsMember2023-12-310001694426dk:OtherJointVentureInvestmentsMember2022-12-310001694426dk:TitledInventoryMember2023-12-310001694426dk:InventoryIntermediationAgreementMember2023-12-310001694426dk:TitledInventoryMember2022-12-310001694426dk:InventoryIntermediationAgreementMember2022-12-310001694426us-gaap:CostOfSalesMember2023-01-012023-12-310001694426us-gaap:CostOfSalesMember2022-01-012022-12-310001694426us-gaap:CostOfSalesMember2021-01-012021-12-3100016944262022-12-2200016944262023-12-202023-12-2000016944262023-12-212023-12-2100016944262023-12-2000016944262023-12-21dk:barrel0001694426dk:JAronCompanyMemberdk:ElDoradoRefineryMember2022-01-012022-12-310001694426dk:JAronCompanyMemberdk:ElDoradoRefineryMember2021-01-012021-12-310001694426dk:JAronCompanyMemberdk:ElDoradoRefineryMember2022-12-310001694426us-gaap:RevolvingCreditFacilityMemberdk:DelekRevolverMemberus-gaap:LineOfCreditMember2023-12-310001694426us-gaap:RevolvingCreditFacilityMemberdk:DelekRevolverMemberus-gaap:LineOfCreditMember2022-12-310001694426us-gaap:SecuredDebtMemberdk:DelekTermLoanCreditFacilityMember2023-12-310001694426us-gaap:SecuredDebtMemberdk:DelekTermLoanCreditFacilityMember2022-12-310001694426us-gaap:RevolvingCreditFacilityMemberdk:DklRevolverMemberus-gaap:LineOfCreditMember2023-12-310001694426us-gaap:RevolvingCreditFacilityMemberdk:DklRevolverMemberus-gaap:LineOfCreditMember2022-12-310001694426us-gaap:RevolvingCreditFacilityMemberdk:DKLTermFacilityMemberus-gaap:LineOfCreditMember2023-12-310001694426us-gaap:RevolvingCreditFacilityMemberdk:DKLTermFacilityMemberus-gaap:LineOfCreditMember2022-12-310001694426dk:A2025NotesMemberus-gaap:SeniorNotesMember2023-12-310001694426dk:A2025NotesMemberus-gaap:SeniorNotesMember2022-12-310001694426dk:A2028NotesMemberus-gaap:SeniorNotesMember2023-12-310001694426dk:A2028NotesMemberus-gaap:SeniorNotesMember2022-12-310001694426dk:UnitedCommunityBankRevolverMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2023-12-310001694426dk:UnitedCommunityBankRevolverMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2022-12-310001694426us-gaap:RevolvingCreditFacilityMemberus-gaap:SecuredDebtMember2022-11-180001694426us-gaap:SecuredDebtMember2022-11-180001694426dk:IncrementalTermLoansMemberus-gaap:SecuredDebtMember2022-11-182022-11-180001694426dk:IncrementalTermLoansMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:BaseRateMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426dk:IncrementalTermLoansMemberus-gaap:RevolvingCreditFacilityMemberdk:SecuredOvernightFinancingRateSOFRMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426us-gaap:SecuredDebtMember2023-12-310001694426us-gaap:SecuredDebtMember2022-12-310001694426us-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2023-12-310001694426us-gaap:RevolvingCreditFacilityMemberdk:FifthThirdBankMemberdk:DKLRevolverDelekLogisticsTermFacilityMemberus-gaap:SecuredDebtMember2022-10-130001694426us-gaap:RevolvingCreditFacilityMemberdk:FifthThirdBankMemberdk:DKLRevolverDelekLogisticsTermFacilityMemberus-gaap:SecuredDebtMember2023-11-060001694426us-gaap:RevolvingCreditFacilityMemberus-gaap:DebtInstrumentRedemptionPeriodOneMemberdk:DklRevolverMemberus-gaap:LineOfCreditMember2023-01-012023-12-31dk:payment0001694426us-gaap:RevolvingCreditFacilityMemberdk:DklRevolverMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426srt:ScenarioForecastMemberus-gaap:RevolvingCreditFacilityMemberdk:DklRevolverMemberus-gaap:LineOfCreditMemberus-gaap:DebtInstrumentRedemptionPeriodTwoMember2024-01-012024-12-310001694426srt:ScenarioForecastMemberus-gaap:RevolvingCreditFacilityMemberdk:DklRevolverMemberus-gaap:LineOfCreditMember2024-01-012024-12-310001694426srt:ScenarioForecastMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:DebtInstrumentRedemptionPeriodThreeMemberdk:DklRevolverMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001694426srt:ScenarioForecastMemberus-gaap:RevolvingCreditFacilityMemberdk:DklRevolverMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001694426dk:DebtInstrumentInterestRatePeriodOneMemberdk:FifthThirdBankMemberdk:DKLRevolverDelekLogisticsTermFacilityMemberus-gaap:SecuredDebtMemberus-gaap:PrimeRateMember2022-10-132022-10-130001694426dk:DebtInstrumentInterestRatePeriodTwoMemberdk:FifthThirdBankMemberdk:DKLRevolverDelekLogisticsTermFacilityMemberus-gaap:SecuredDebtMemberus-gaap:PrimeRateMember2022-10-132022-10-130001694426dk:DebtInstrumentInterestRatePeriodOneMemberdk:FifthThirdBankMemberdk:DKLRevolverDelekLogisticsTermFacilityMemberus-gaap:SecuredDebtMembersrt:MinimumMemberdk:SecuredOvernightFinancingRateSOFRMember2023-01-012023-12-310001694426dk:FifthThirdBankMemberus-gaap:SecuredDebtMembersrt:MaximumMemberdk:SecuredOvernightFinancingRateSOFRMemberdk:DKLRevolverSeniorSecuredRevolvingCommitmentMember2023-01-012023-12-310001694426dk:DebtInstrumentInterestRatePeriodOneMemberdk:FifthThirdBankMemberdk:DKLRevolverDelekLogisticsTermFacilityMemberus-gaap:SecuredDebtMember2022-10-132022-10-130001694426dk:DebtInstrumentInterestRatePeriodTwoMemberdk:FifthThirdBankMemberdk:DKLRevolverDelekLogisticsTermFacilityMemberus-gaap:SecuredDebtMember2022-10-132022-10-130001694426us-gaap:RevolvingCreditFacilityMemberdk:FifthThirdBankMemberdk:DKLTermFacilityMemberus-gaap:LineOfCreditMember2023-12-310001694426us-gaap:RevolvingCreditFacilityMemberdk:FifthThirdBankMemberdk:DKLTermFacilityMemberus-gaap:LineOfCreditMember2022-12-310001694426us-gaap:RevolvingCreditFacilityMemberdk:FifthThirdBankMemberdk:DklRevolverMemberus-gaap:LineOfCreditMember2023-12-310001694426us-gaap:RevolvingCreditFacilityMemberus-gaap:LetterOfCreditMember2023-12-310001694426us-gaap:RevolvingCreditFacilityMembersrt:MaximumMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426us-gaap:RevolvingCreditFacilityMemberus-gaap:BaseRateMembersrt:MinimumMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426us-gaap:RevolvingCreditFacilityMemberus-gaap:BaseRateMembersrt:MaximumMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426us-gaap:RevolvingCreditFacilityMembersrt:MinimumMemberdk:SecuredOvernightFinancingRateSOFRAndCanadianOvernightFinancingRateCDORMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426us-gaap:RevolvingCreditFacilityMembersrt:MaximumMemberdk:SecuredOvernightFinancingRateSOFRAndCanadianOvernightFinancingRateCDORMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426us-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2022-12-310001694426us-gaap:LetterOfCreditMemberdk:FifthThirdBankMemberdk:DklRevolverMemberus-gaap:LineOfCreditMember2023-12-310001694426dk:USSwingLineSublimitMemberdk:FifthThirdBankMemberdk:DklRevolverMemberus-gaap:LineOfCreditMember2023-12-310001694426dk:FifthThirdBankMembersrt:MaximumMemberdk:DklRevolverMember2023-01-012023-12-310001694426dk:FifthThirdBankMemberus-gaap:PrimeRateMembersrt:MinimumMemberdk:DKLRevolverSeniorSecuredRevolvingCommitmentMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426dk:FifthThirdBankMemberus-gaap:PrimeRateMembersrt:MaximumMemberdk:DKLRevolverSeniorSecuredRevolvingCommitmentMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426dk:FifthThirdBankMemberus-gaap:SecuredDebtMembersrt:MinimumMemberdk:SecuredOvernightFinancingRateSOFRMemberdk:DKLRevolverSeniorSecuredRevolvingCommitmentMember2023-01-012023-12-310001694426dk:TotalLeverageRatioInterestRateMemberdk:FifthThirdBankMembersrt:MinimumMemberdk:DKLRevolverSeniorSecuredRevolvingCommitmentMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426dk:TotalLeverageRatioInterestRateMemberdk:FifthThirdBankMembersrt:MaximumMemberdk:DKLRevolverSeniorSecuredRevolvingCommitmentMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426us-gaap:RevolvingCreditFacilityMemberdk:FifthThirdBankMemberdk:DKLRevolverSeniorSecuredRevolvingCommitmentMemberus-gaap:LineOfCreditMember2023-12-310001694426us-gaap:RevolvingCreditFacilityMemberdk:FifthThirdBankMemberdk:DKLRevolverSeniorSecuredRevolvingCommitmentMemberus-gaap:LineOfCreditMember2022-12-310001694426dk:UnitedCommunityBankRevolverMemberus-gaap:RevolvingCreditFacilityMemberdk:WallStreetJournalPrimeRateMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426dk:UnitedCommunityBankRevolverMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001694426us-gaap:RevolvingCreditFacilityMemberdk:FirstSecondAndThirdAmendmentMemberdk:FifthThirdBankMemberus-gaap:LineOfCreditMember2023-11-062023-11-060001694426us-gaap:RevolvingCreditFacilityMemberdk:FifthThirdBankMemberdk:FirstAmendmentMemberus-gaap:LineOfCreditMember2023-11-060001694426dk:FifthThirdBankMemberdk:FirstAmendmentMemberus-gaap:UnsecuredDebtMemberus-gaap:LineOfCreditMember2023-11-060001694426dk:UnitedCommunityBankRevolverMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2023-06-080001694426dk:UnitedCommunityBankRevolverMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2023-06-090001694426dk:A2025NotesMemberus-gaap:SeniorNotesMember2018-05-310001694426dk:A2025NotesMemberus-gaap:SeniorNotesMember2023-05-152023-05-150001694426dk:A2025NotesMemberus-gaap:SeniorNotesMember2023-01-012023-12-310001694426dk:A2028NotesMemberus-gaap:SeniorNotesMember2021-05-240001694426dk:A2028NotesMemberus-gaap:SeniorNotesMember2021-05-242021-05-240001694426us-gaap:DebtInstrumentRedemptionPeriodOneMemberdk:A2028NotesMemberus-gaap:SeniorNotesMember2021-05-242021-05-240001694426dk:A2028NotesMemberus-gaap:SeniorNotesMemberus-gaap:DebtInstrumentRedemptionPeriodTwoMember2021-05-242021-05-240001694426dk:A2028NotesMemberus-gaap:DebtInstrumentRedemptionPeriodThreeMemberus-gaap:SeniorNotesMember2021-05-242021-05-240001694426us-gaap:DebtInstrumentRedemptionPeriodFourMemberdk:A2028NotesMemberus-gaap:SeniorNotesMember2021-05-242021-05-240001694426us-gaap:CommodityContractMember2023-01-012023-12-310001694426us-gaap:OtherCurrentAssetsMemberus-gaap:CommodityContractMemberus-gaap:NondesignatedMember2023-12-310001694426us-gaap:OtherCurrentAssetsMemberus-gaap:CommodityContractMemberus-gaap:NondesignatedMember2022-12-310001694426us-gaap:CommodityContractMemberus-gaap:NondesignatedMemberus-gaap:OtherCurrentLiabilitiesMember2023-12-310001694426us-gaap:CommodityContractMemberus-gaap:NondesignatedMemberus-gaap:OtherCurrentLiabilitiesMember2022-12-310001694426us-gaap:CommodityContractMemberus-gaap:NondesignatedMemberus-gaap:OtherNoncurrentAssetsMember2023-12-310001694426us-gaap:CommodityContractMemberus-gaap:NondesignatedMemberus-gaap:OtherNoncurrentAssetsMember2022-12-310001694426us-gaap:OtherCurrentAssetsMemberdk:RINCommitmentContractsMemberus-gaap:NondesignatedMember2023-12-310001694426us-gaap:OtherCurrentAssetsMemberdk:RINCommitmentContractsMemberus-gaap:NondesignatedMember2022-12-310001694426dk:RINCommitmentContractsMemberus-gaap:NondesignatedMemberus-gaap:OtherCurrentLiabilitiesMember2023-12-310001694426dk:RINCommitmentContractsMemberus-gaap:NondesignatedMemberus-gaap:OtherCurrentLiabilitiesMember2022-12-310001694426us-gaap:CommodityContractMember2023-12-31utr:bbl0001694426us-gaap:CommodityContractMember2022-12-31utr:MMBTUdk:rIN0001694426us-gaap:CommodityContractMemberus-gaap:NondesignatedMemberus-gaap:CostOfSalesMember2023-01-012023-12-310001694426us-gaap:CommodityContractMemberus-gaap:NondesignatedMemberus-gaap:CostOfSalesMember2022-01-012022-12-310001694426us-gaap:CommodityContractMemberus-gaap:NondesignatedMemberus-gaap:CostOfSalesMember2021-01-012021-12-310001694426us-gaap:CommodityContractMember2022-01-012022-12-310001694426us-gaap:CommodityContractMember2021-01-012021-12-310001694426us-gaap:CommodityContractMemberus-gaap:NondesignatedMemberus-gaap:OperatingExpenseMember2023-01-012023-12-310001694426us-gaap:CommodityContractMemberus-gaap:NondesignatedMemberus-gaap:OperatingExpenseMember2022-01-012022-12-310001694426us-gaap:CommodityContractMemberus-gaap:NondesignatedMemberus-gaap:OperatingExpenseMember2021-01-012021-12-310001694426us-gaap:CommodityContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2023-01-012023-12-310001694426us-gaap:CommodityContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2022-01-012022-12-310001694426us-gaap:CommodityContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2021-01-012021-12-310001694426us-gaap:CommodityContractMemberus-gaap:CostOfSalesMember2023-01-012023-12-310001694426us-gaap:CommodityContractMemberus-gaap:CostOfSalesMember2022-01-012022-12-310001694426us-gaap:CommodityContractMemberus-gaap:CostOfSalesMember2021-01-012021-12-310001694426us-gaap:NondesignatedMemberus-gaap:CostOfSalesMember2023-01-012023-12-310001694426us-gaap:NondesignatedMemberus-gaap:CostOfSalesMember2022-01-012022-12-310001694426us-gaap:NondesignatedMemberus-gaap:CostOfSalesMember2021-01-012021-12-310001694426us-gaap:ForwardContractsMember2023-01-012023-12-310001694426us-gaap:ForwardContractsMember2022-01-012022-12-310001694426us-gaap:ForwardContractsMember2021-01-012021-12-310001694426dk:RINCommitmentContractsMember2023-01-012023-12-310001694426dk:RINCommitmentContractsMember2022-01-012022-12-310001694426dk:RINCommitmentContractsMember2021-01-012021-12-310001694426dk:A2028NotesMemberus-gaap:FairValueInputsLevel1Memberus-gaap:SeniorNotesMember2023-12-310001694426dk:A2028NotesMemberus-gaap:FairValueInputsLevel1Memberus-gaap:SeniorNotesMember2022-12-310001694426us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2023-12-310001694426us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2023-12-310001694426us-gaap:CommodityContractMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001694426us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001694426dk:RINCommitmentContractsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2023-12-310001694426dk:RINCommitmentContractsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2023-12-310001694426dk:RINCommitmentContractsMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001694426dk:RINCommitmentContractsMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2023-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2023-12-310001694426us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001694426us-gaap:FairValueMeasurementsRecurringMember2023-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberdk:EnvironmentalCreditsObligationMember2023-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberdk:EnvironmentalCreditsObligationMemberus-gaap:FairValueInputsLevel2Member2023-12-310001694426us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberdk:EnvironmentalCreditsObligationMember2023-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberdk:EnvironmentalCreditsObligationMember2023-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberdk:InventoryIntermediationAgreementMember2023-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberdk:InventoryIntermediationAgreementMemberus-gaap:FairValueInputsLevel2Member2023-12-310001694426us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberdk:InventoryIntermediationAgreementMember2023-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberdk:InventoryIntermediationAgreementMember2023-12-310001694426us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2022-12-310001694426us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2022-12-310001694426us-gaap:CommodityContractMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001694426us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001694426dk:RINCommitmentContractsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2022-12-310001694426dk:RINCommitmentContractsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2022-12-310001694426dk:RINCommitmentContractsMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001694426dk:RINCommitmentContractsMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2022-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2022-12-310001694426us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001694426us-gaap:FairValueMeasurementsRecurringMember2022-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberdk:EnvironmentalCreditsObligationMember2022-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberdk:EnvironmentalCreditsObligationMemberus-gaap:FairValueInputsLevel2Member2022-12-310001694426us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberdk:EnvironmentalCreditsObligationMember2022-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberdk:EnvironmentalCreditsObligationMember2022-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberdk:InventoryIntermediationAgreementMember2022-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberdk:InventoryIntermediationAgreementMemberus-gaap:FairValueInputsLevel2Member2022-12-310001694426us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberdk:InventoryIntermediationAgreementMember2022-12-310001694426us-gaap:FairValueMeasurementsRecurringMemberdk:InventoryIntermediationAgreementMember2022-12-310001694426dk:AsphaltAndMarineFuelTerminalMember2022-12-310001694426dk:AsphaltAndMarineFuelTerminalMember2023-12-3100016944262020-06-3000016944262021-04-012021-06-300001694426dk:ElDoradoRefineryFireMember2021-01-012021-12-310001694426dk:ElDoradoRefineryFireMember2022-01-012022-12-310001694426dk:ElDoradoRefineryFireMember2023-01-012023-12-3100016944262023-10-012023-10-31dk:employee0001694426dk:ElDoradoRefineryFireMember2023-10-012023-10-310001694426dk:BigSpringRefineryMember2023-01-012023-12-310001694426dk:WinterStormUriMember2021-01-012021-12-310001694426dk:WinterStormUriMember2023-01-012023-12-310001694426dk:WinterStormUriMember2022-01-012022-12-31dk:crudeOilRelease0001694426us-gaap:DomesticCountryMember2023-12-310001694426us-gaap:StateAndLocalJurisdictionMember2023-12-310001694426us-gaap:RelatedPartyMember2023-01-012023-12-310001694426us-gaap:RelatedPartyMember2022-01-012022-12-310001694426us-gaap:RelatedPartyMember2021-01-012021-12-310001694426us-gaap:OperatingSegmentsMemberdk:RefiningMember2021-12-310001694426dk:LogisticsMemberus-gaap:OperatingSegmentsMember2021-12-310001694426dk:RetailSegmentMemberus-gaap:OperatingSegmentsMember2021-12-310001694426srt:ConsolidationEliminationsMember2021-12-310001694426srt:ConsolidationEliminationsMember2022-01-012022-12-310001694426us-gaap:OperatingSegmentsMemberdk:RefiningMember2022-12-310001694426dk:LogisticsMemberus-gaap:OperatingSegmentsMember2022-12-310001694426dk:RetailSegmentMemberus-gaap:OperatingSegmentsMember2022-12-310001694426srt:ConsolidationEliminationsMember2022-12-310001694426srt:ConsolidationEliminationsMember2023-01-012023-12-310001694426us-gaap:OperatingSegmentsMemberdk:RefiningMember2023-12-310001694426dk:LogisticsMemberus-gaap:OperatingSegmentsMember2023-12-310001694426dk:RetailSegmentMemberus-gaap:OperatingSegmentsMember2023-12-310001694426srt:ConsolidationEliminationsMember2023-12-310001694426dk:FuelSupplyAgreementMember2022-12-310001694426dk:FuelSupplyAgreementMember2023-12-310001694426dk:FuelTradeNameMember2023-12-310001694426dk:FuelTradeNameMember2022-12-310001694426dk:RightsofWayMembersrt:MinimumMember2022-12-310001694426dk:RightsofWayMembersrt:MinimumMember2023-12-310001694426dk:RightsofWayMembersrt:MaximumMember2022-12-310001694426dk:RightsofWayMembersrt:MaximumMember2023-12-310001694426dk:RightsofWayMember2023-12-310001694426dk:RightsofWayMember2022-12-310001694426us-gaap:CustomerRelationshipsMember2023-12-310001694426us-gaap:CustomerRelationshipsMember2022-12-310001694426dk:RightsofWayMember2023-12-310001694426dk:RightsofWayMember2022-12-310001694426dk:LinespacehistoryMember2023-12-310001694426dk:LinespacehistoryMember2022-12-310001694426dk:LiquorLicensesMember2023-12-310001694426dk:LiquorLicensesMember2022-12-310001694426dk:RefineryPermitsMember2023-12-310001694426dk:RefineryPermitsMember2022-12-310001694426dk:DepreciationandAmortizationExpenseAdjustmentMember2023-01-012023-12-310001694426dk:DepreciationandAmortizationExpenseAdjustmentMember2022-01-012022-12-310001694426dk:DepreciationandAmortizationExpenseAdjustmentMember2021-01-012021-12-310001694426us-gaap:LandMember2023-12-310001694426us-gaap:LandMember2022-12-310001694426us-gaap:BuildingAndBuildingImprovementsMember2023-12-310001694426us-gaap:BuildingAndBuildingImprovementsMember2022-12-310001694426dk:RefineryMachineryAndEquipmentMember2023-12-310001694426dk:RefineryMachineryAndEquipmentMember2022-12-310001694426dk:PipelinestanksandterminalsMember2023-12-310001694426dk:PipelinestanksandterminalsMember2022-12-310001694426dk:SiteimprovementsMember2023-12-310001694426dk:SiteimprovementsMember2022-12-310001694426dk:RefineryTurnaroundCostsMember2023-12-310001694426dk:RefineryTurnaroundCostsMember2022-12-310001694426us-gaap:OtherMachineryAndEquipmentMember2023-12-310001694426us-gaap:OtherMachineryAndEquipmentMember2022-12-310001694426us-gaap:ConstructionInProgressMember2023-12-310001694426us-gaap:ConstructionInProgressMember2022-12-310001694426dk:DelekUs2006LongTermIncentivePlanMember2023-12-310001694426us-gaap:CommonStockMember2022-05-020001694426us-gaap:CommonStockMember2023-05-020001694426us-gaap:CommonStockMember2023-05-030001694426us-gaap:RestrictedStockUnitsRSUMembersrt:MinimumMember2023-01-012023-12-310001694426us-gaap:RestrictedStockUnitsRSUMembersrt:MaximumMember2023-01-012023-12-31dk:tranche0001694426us-gaap:PerformanceSharesMember2023-01-012023-12-310001694426dk:A2023GrantsMemberus-gaap:PerformanceSharesMember2023-01-012023-12-310001694426dk:A2022GrantsMemberus-gaap:PerformanceSharesMember2023-01-012023-12-310001694426us-gaap:PerformanceSharesMemberdk:A2021GrantsMember2023-01-012023-12-310001694426dk:A2023GrantsMemberus-gaap:PerformanceSharesMembersrt:MinimumMember2023-01-012023-12-310001694426dk:A2023GrantsMemberus-gaap:PerformanceSharesMembersrt:MaximumMember2023-01-012023-12-310001694426dk:A2022GrantsMemberus-gaap:PerformanceSharesMembersrt:MinimumMember2023-01-012023-12-310001694426dk:A2022GrantsMemberus-gaap:PerformanceSharesMembersrt:MaximumMember2023-01-012023-12-310001694426dk:DelekUS2006And2016AndAlonUSAEnergy2005LongTermIncentivePlanMemberus-gaap:GeneralAndAdministrativeExpenseMember2023-01-012023-12-310001694426dk:DelekUS2006And2016AndAlonUSAEnergy2005LongTermIncentivePlanMemberus-gaap:GeneralAndAdministrativeExpenseMember2022-01-012022-12-310001694426dk:DelekUS2006And2016AndAlonUSAEnergy2005LongTermIncentivePlanMemberus-gaap:GeneralAndAdministrativeExpenseMember2021-01-012021-12-310001694426dk:DelekUS2006And2016AndAlonUSAEnergy2005LongTermIncentivePlanMember2023-12-310001694426dk:DelekUS2006And2016AndAlonUSAEnergy2005LongTermIncentivePlanMember2023-01-012023-12-310001694426us-gaap:CommonStockMemberdk:DelekLogisticsGP2012LongTermIncentivePlanMember2021-06-092021-06-090001694426us-gaap:CommonStockMemberdk:DelekLogisticsGP2012LongTermIncentivePlanMember2021-06-0900016944262023-02-272023-02-2700016944262023-05-022023-05-0200016944262023-08-042023-08-0400016944262023-11-012023-11-010001694426us-gaap:SubsequentEventMember2024-02-202024-02-200001694426us-gaap:CommonStockMember2018-11-060001694426us-gaap:CommonStockMember2022-08-012022-08-010001694426us-gaap:CommonStockMember2022-08-010001694426us-gaap:CommonStockMember2022-03-072022-03-0700016944262022-03-072022-03-070001694426dk:TylerRefineryMember2023-01-012023-12-310001694426dk:ElDoradoRefineryMember2023-01-012023-12-310001694426dk:BigSpringRefineryMember2023-01-012023-12-31dk:defined_benefit_plan0001694426us-gaap:DefinedBenefitPlanEquitySecuritiesMember2023-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesMember2022-12-310001694426us-gaap:FixedIncomeSecuritiesMember2023-12-310001694426us-gaap:FixedIncomeSecuritiesMember2022-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesUsMemberus-gaap:FairValueInputsLevel1Member2023-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesUsMemberus-gaap:FairValueInputsLevel2Member2023-12-310001694426us-gaap:FairValueInputsLevel3Memberus-gaap:DefinedBenefitPlanEquitySecuritiesUsMember2023-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesUsMember2023-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMemberus-gaap:FairValueInputsLevel1Member2023-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMemberus-gaap:FairValueInputsLevel2Member2023-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMemberus-gaap:FairValueInputsLevel3Member2023-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMember2023-12-310001694426us-gaap:FixedIncomeSecuritiesMemberus-gaap:FairValueInputsLevel1Member2023-12-310001694426us-gaap:FixedIncomeSecuritiesMemberus-gaap:FairValueInputsLevel2Member2023-12-310001694426us-gaap:FairValueInputsLevel3Memberus-gaap:FixedIncomeSecuritiesMember2023-12-310001694426us-gaap:FairValueInputsLevel1Member2023-12-310001694426us-gaap:FairValueInputsLevel2Member2023-12-310001694426us-gaap:FairValueInputsLevel3Member2023-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesUsMemberus-gaap:FairValueInputsLevel1Member2022-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesUsMemberus-gaap:FairValueInputsLevel2Member2022-12-310001694426us-gaap:FairValueInputsLevel3Memberus-gaap:DefinedBenefitPlanEquitySecuritiesUsMember2022-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesUsMember2022-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMemberus-gaap:FairValueInputsLevel1Member2022-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMemberus-gaap:FairValueInputsLevel2Member2022-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMemberus-gaap:FairValueInputsLevel3Member2022-12-310001694426us-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMember2022-12-310001694426us-gaap:FixedIncomeSecuritiesMemberus-gaap:FairValueInputsLevel1Member2022-12-310001694426us-gaap:FixedIncomeSecuritiesMemberus-gaap:FairValueInputsLevel2Member2022-12-310001694426us-gaap:FairValueInputsLevel3Memberus-gaap:FixedIncomeSecuritiesMember2022-12-310001694426us-gaap:FairValueInputsLevel1Member2022-12-310001694426us-gaap:FairValueInputsLevel2Member2022-12-310001694426us-gaap:FairValueInputsLevel3Member2022-12-310001694426dk:OilTanksMember2023-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| | | | | | | | | | | | | | |

| ☑ | | ANNUAL REPORT PURSUANT TO SECTION 18 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | | | |

| | For the Fiscal Year Ended | December 31, 2023 | |

OR

| | | | | | | | | | | | | | |

| ☐ | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | | | |

| | For the transition period from to |

Commission file number 001-38142

DELEK US HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | |

| Delaware | | 35-2581557 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| |

|

310 Seven Springs Way, Suite 500 | Brentwood | Tennessee | 37027 |

| (Address of principal executive offices) | | | (Zip Code) |

(615) 771-6701

(Registrant’s telephone number, including area code)

Not applicable

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Common Stock, par value $0.01 | | DK | | New York Stock Exchange |

| | | | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☑ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 4262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

The aggregate market value of the common stock held by non-affiliates as of June 30, 2023 was approximately $1,542,152,000, based upon the closing sale price of the registrant's common stock on the New York Stock Exchange on that date. For purposes of this calculation only, all directors and officers subject to Section 16(b) of the Securities Exchange Act of 1934 are deemed to be affiliates.

At February 21, 2024, there were 64,019,267 shares of the registrant's common stock, $.01 par value, outstanding (excluding securities held by, or for the account of, the Company or its subsidiaries).

Documents incorporated by reference

Portions of the registrant's definitive Proxy Statement to be delivered to stockholders in connection with the 2024 Annual Meeting of Stockholders, which will be filed with the Securities and Exchange Commission within 120 days after December 31, 2023, are incorporated by reference into Part III of this Annual Report on Form 10-K.

Delek US Holdings, Inc.

Annual Report on Form 10-K

For the Annual Period Ending December 31, 2023

PART I

Delek US Holdings, Inc. is a registrant pursuant to the Securities Act of 1933 and is listed on the New York Stock Exchange ("NYSE") under the ticker symbol "DK." Effective July 1, 2017, we acquired the outstanding common stock of Alon USA Energy, Inc. ("Alon") (the "Delek/Alon Merger"), resulting in a new post-combination consolidated registrant renamed as Delek US Holdings, Inc.

Unless otherwise noted or the context requires otherwise, the terms "we," "our," "us," "Delek" and the "Company" are used in this report to refer to Delek US Holdings, Inc. and its consolidated subsidiaries for all periods presented. Our business consists of three operating segments: refining, logistics and retail.

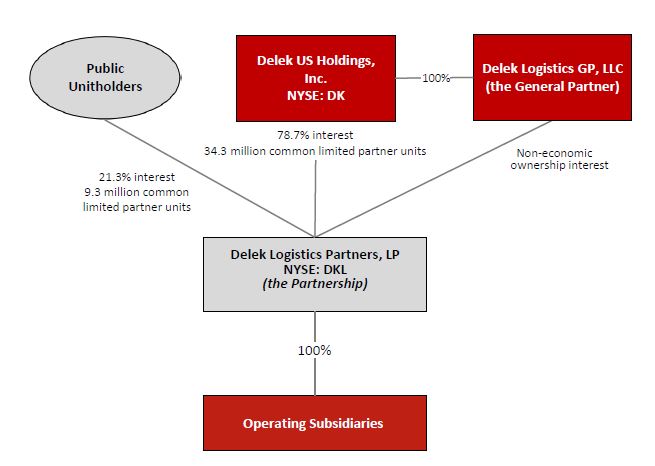

As of December 31, 2023, we owned a 78.7% limited partner interest as well as a non-economic general partner interest in Delek Logistics Partners, LP ("Delek Logistics", NYSE:DKL), a publicly-traded master limited partnership that we formed in April 2012.

Statements in this Annual Report on Form 10-K, other than purely historical information, including statements regarding our plans, strategies, objectives, beliefs, expectations and intentions are forward-looking statements. Forward-looking statements include, among other things, statements that refer to the acquisition of 3 Bear Delaware Holding – NM, LLC (“3 Bear”) (subsequently renamed to Delek Delaware Gathering ("Delaware Gathering")) (the "Delaware Gathering Acquisition"), including any statements regarding the expected benefits, synergies, growth opportunities, impact on liquidity and prospects, and other financial and operating benefits thereof, the information concerning possible future results of operations, business and growth strategies, including as the same may be impacted by any ongoing military conflict, such as the war between Russia and Ukraine ("the Russia-Ukraine War"), financing plans, expectations that regulatory developments or other matters will or will not have a material adverse effect on our business or financial condition, our competitive position and the effects of competition, the projected growth of the industry in which we operate, and the benefits and synergies to be obtained from our completed and any future acquisitions, statements of management’s goals and objectives, and other similar expressions concerning matters that are not historical facts. Words such as "may," "will," "should," "could," "would," "predicts," "potential," "continue," "expects," "anticipates," "future," "intends," "plans," "believes," "estimates," "appears," "projects" and similar expressions, as well as statements in future tense, identify forward-looking statements. Forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties, including those discussed below and in Item 1A. Risk Factors, which may cause actual results to differ materially from the forward-looking statements. See also "Forward-Looking Statements" included in Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations, of this Annual Report on Form 10-K.

See the “Glossary of Terms” beginning on page 4 of this Annual Report on Form 10-K for definitions of certain business and industry terms used herein. Available Information

Our Internet website address is www.DelekUS.com and X (previously known as Twitter) account is @DelekUSHoldings. Information contained on our website is not part of this Annual Report on Form 10-K. Our reports, proxy and information statements, and any amendments to such documents are filed electronically with the Securities and Exchange Commission (“SEC”) and are available on our Internet website in the “Investor Relations” section (ir.delekus.com), free of charge, as soon as reasonably practicable after we file or furnish such material to the SEC. We also post our Governance Guidelines, Code of Business Conduct & Ethics and the charters of our Board of Directors’ committees in the “Corporate Governance” section of our website, accessible by navigating to the “About Us” section on our Internet website. We will provide any of these documents to any stockholder that makes a written request to the Corporate Secretary, Delek US Holdings, Inc., 310 Seven Springs Way, Suite 500, Brentwood, Tennessee 37027.

Glossary of Terms

The following are definitions of certain industry terms used in this Annual Report on Form 10-K:

Alkylation Unit - A refinery unit utilizing an acid catalyst to combine smaller hydrocarbon molecules to form larger molecules in the gasoline boiling range to produce a high octane gasoline blendstock, which is referred to as alkylate.

Barrel - A unit of volumetric measurement equivalent to 42 U.S. gallons.

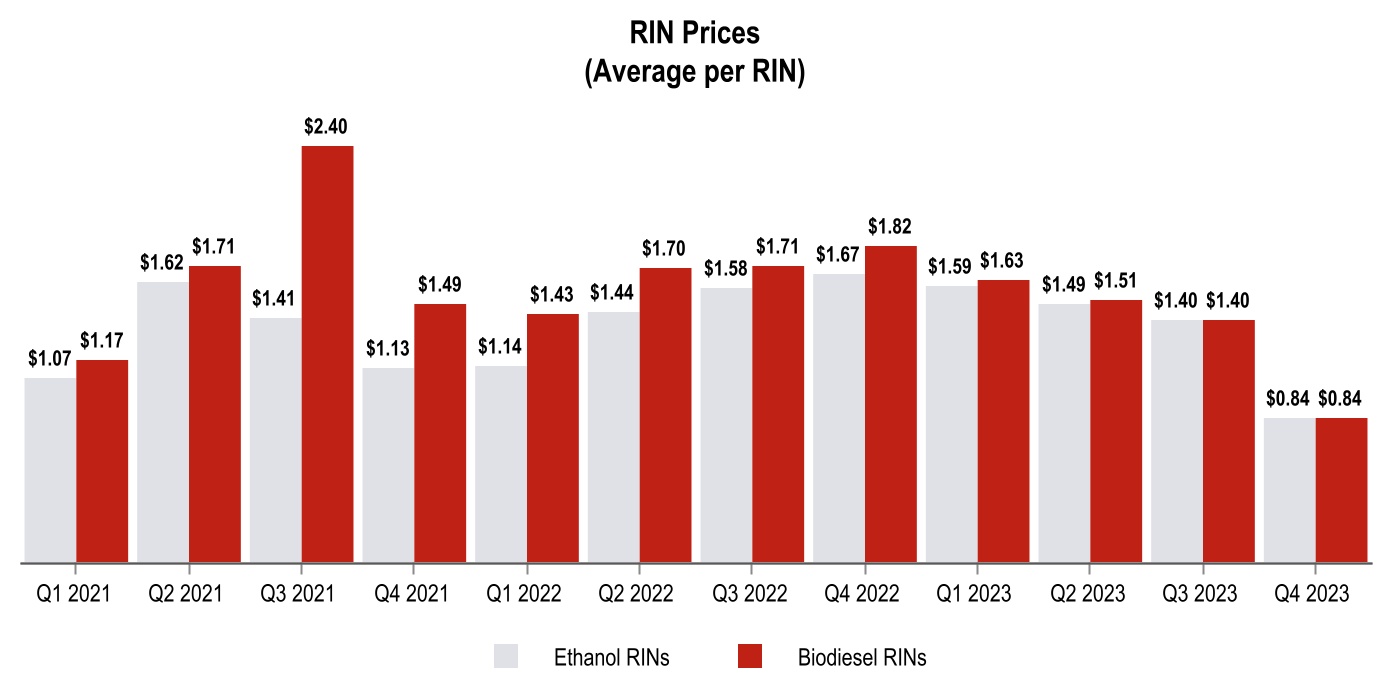

Biodiesel - A renewable fuel produced from vegetable oils or animal fats that can be blended with petroleum-derived diesel to produce biodiesel blends for use in diesel engines. Pure biodiesel is referred to as B100, whereas blends of biodiesel are referenced by how much biodiesel is in the blend (e.g., a B5 blend contains five volume percent biodiesel and 95 volume percent ULSD).

Blendstocks - Various products or intermediate streams that are combined with other components of similar type and distillation range to produce finished gasoline, diesel fuel or other refined products. Blendstocks may include natural gasoline, hydrotreated Fluid Catalytic Cracking Unit gasoline, alkylate, ethanol, reformate, butane, diesel, biodiesel, kerosene, light cycle oil or slurry, among others.

Bpd/bpd - Barrels per calendar day.

Brent Crude (Brent) - A light, sweet crude oil, though not as light as WTI. Brent is the leading global price benchmark for Atlantic basin crude oil.

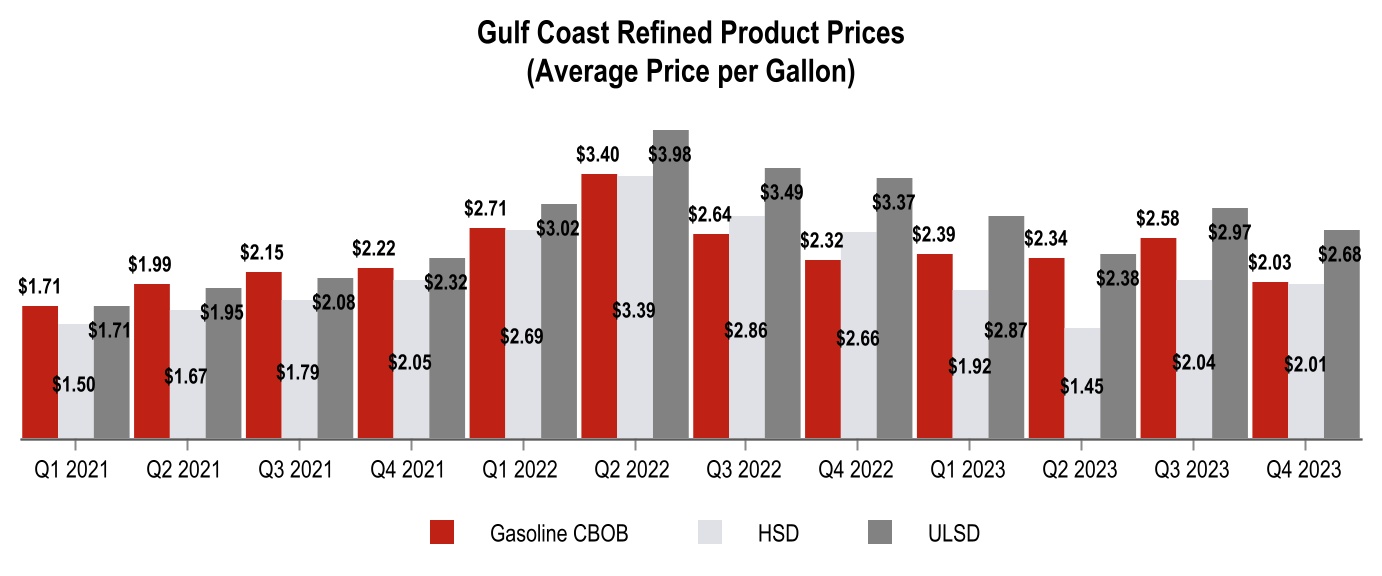

CBOB - Motor gasoline blending components intended for blending with oxygenates, such as ethanol, to produce finished conventional motor gasoline.

CERCLA - Comprehensive Environmental Response, Compensation and Liability Act.

Colonial Pipeline - A pipeline owned and operated by the Colonial Pipeline Company that originates near Houston, Texas and terminates near New York, New York, connecting the U.S. refinery region of the Gulf Coast with customers throughout the southern and eastern United States.

Complexity Index - A measure of secondary conversion capacity of a refinery relative to its primary distillation capacity used to quantify and rank the complexity of various refineries. Generally, more complex refineries have a higher index number.

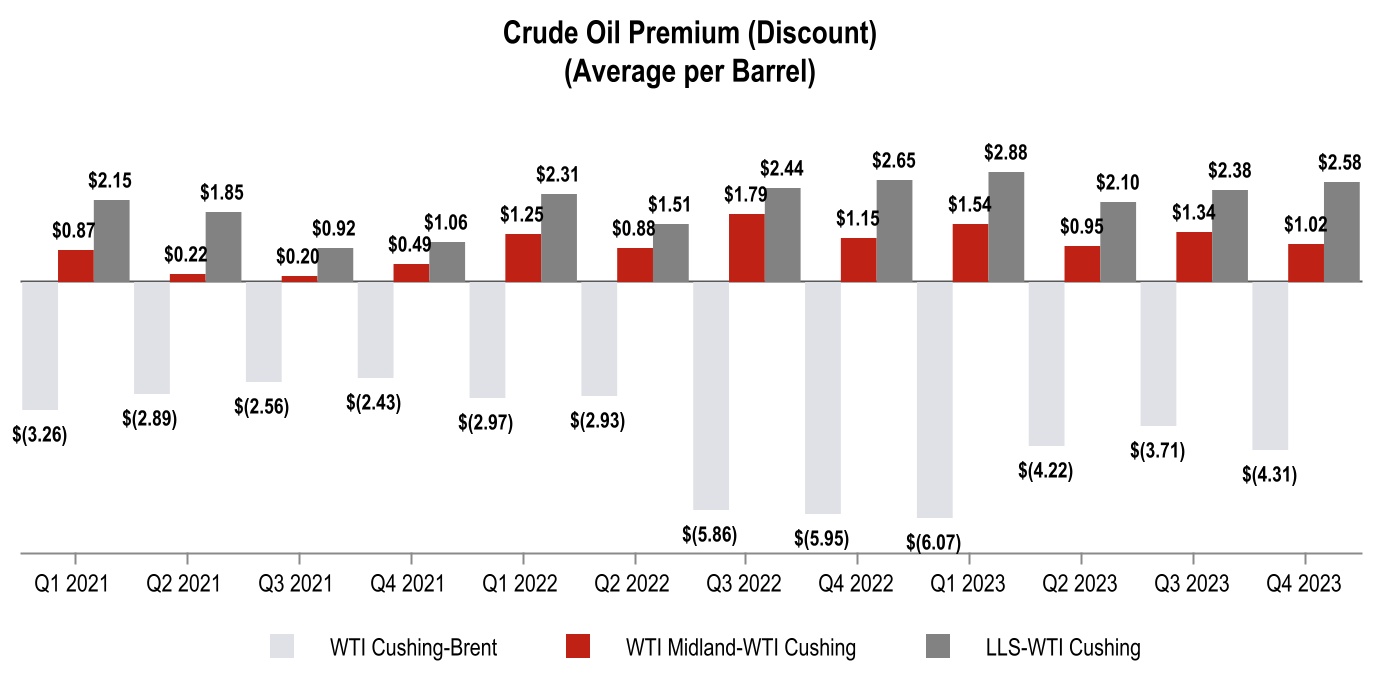

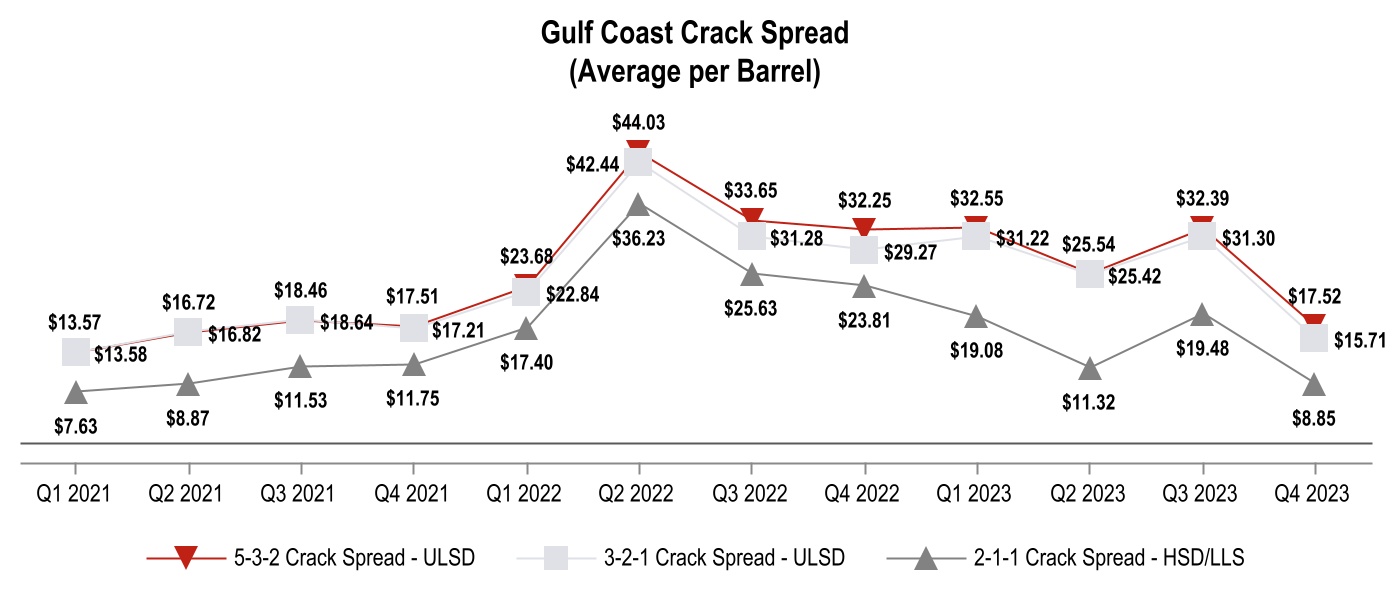

Crack spread - The crack spread is a measure of the difference between market prices for crude oil and refined products and is commonly used proxy within the industry to estimate or identify trends in refining margins.

Cushing - Cushing, Oklahoma.

Delayed Coking Unit (Coker) - A refinery unit that processes ("cracks") heavy oils, such as the bottom cuts of crude oil from the crude or vacuum units, to produce blendstocks for light transportation fuels or feedstocks for other units and petroleum coke.

Direct operating expenses - Operating expenses attributed to the respective segment.

EISA - Energy Independence and Security Act of 2007.

Enterprise Pipeline System - A major product pipeline transport system that reaches from the Gulf Coast into the northeastern United States.

EPA - The Environmental Protection Agency.

ESG - Environmental, Social, and Corporate Governance is an evaluation of an entity's collective conscientiousness for social and environmental factors.

Ethanol - An oxygenated blendstock that is blended with sub-grade (CBOB) or conventional gasoline to produce a finished gasoline.

E-10 - A 90% gasoline-10% ethanol blend.

E-15 - An 85% gasoline-15% ethanol blend.

E-85 - A blend of gasoline and 70%-85% ethanol.

Feedstocks - Crude oil and petroleum products used as inputs in refining processes.

FERC - The Federal Energy Regulatory Commission.

FIFO - First-in, first-out inventory accounting method.

Fluid Catalytic Cracking Unit or FCC Unit - A refinery unit that uses fluidized catalyst at high temperatures to crack large hydrocarbon molecules into smaller, higher-valued molecules (LPG, gasoline, LCO, etc.).

Gulf Coast 2-1-1 crack spread - A crack spread, expressed in dollars per barrel, reflecting the approximate gross margin resulting from processing, or "cracking", one barrel of crude oil into one-half barrel of gasoline and one-half barrel of high sulfur diesel, utilizing the market prices of LLS crude oil, Gulf Coast Pipeline conventional gasoline and Gulf Coast Pipeline No. 2 Heating Oil.

Gulf Coast 3-2-1 crack spread - A crack spread, expressed in dollars per barrel, reflecting the approximate gross margin resulting from processing, or "cracking", one barrel of crude oil into two-thirds barrel of gasoline and one-third barrel of ultra-low sulfur diesel, utilizing the market prices of WTI crude oil, Gulf Coast Pipeline conventional gasoline and Gulf Coast Pipeline ultra-low sulfur diesel.

Gulf Coast 5-3-2 crack spread - A crack spread, expressed in dollars per barrel, reflecting the approximate gross margin resulting from processing, or "cracking", one barrel of crude oil into three-fifths barrel of gasoline and two-fifths barrel of high sulfur diesel, utilizing the market prices of WTI crude oil, Gulf Coast Pipeline CBOB and Gulf Coast Pipeline No. 2 Heating Oil.

Gulf Coast Pipeline CBOB - A grade of gasoline blendstock that must be blended with 10% biofuels in order to be marketed as Regular Unleaded at retail locations.

Gulf Coast Pipeline No. 2 Heating Oil - A petroleum distillate that can be used as either a diesel fuel or a fuel oil. This is the standard by which other Gulf Coast distillate products (such as ultra-low sulfur diesel) are priced.

Gulf Coast Region - Commonly referred to as PADD III, includes the states of Texas, Arkansas, Louisiana, Mississippi, Alabama and New Mexico.

HLS - Heavy Louisiana Sweet crude oil; typical API gravity of 33° and sulfur content of 0.35%.

HSD - High sulfur diesel, No. 2 diesel fuel that has a sulfur level above 500 ppm.

Jobbers - Retail stations owned by third parties that sell products purchased from or through us.

Light/Medium/Heavy Crude Oil - Terms used to describe the relative densities of crude oil, normally represented by their API gravities. Light crude oils (those having relatively high API gravities) may be refined into a greater number of valuable products and are typically more expensive than a heavier crude oil.

LLS - Louisiana Light Sweet crude oil; typical API gravity of 38° and sulfur content of 0.34%.

LPG - Liquefied petroleum gas.

Mid-Continent Region - Commonly referred to as PADD II, includes the states of North Dakota, South Dakota, Nebraska, Kansas, Oklahoma, Minnesota, Iowa, Missouri, Wisconsin, Illinois, Michigan, Indiana, Ohio, Kentucky and Tennessee.

Midland - Midland, Texas.

MBbl/d -Thousand barrels per day

MMBTU - One Million British Thermal Units.

MSCF/d - Abbreviation for a thousand standard cubic feet per day, a common measure for volume of natural gas.

MMcf/d - Abbreviation for a million cubic feet per day common measure for volume of natural gas.

Naphtha - A hydrocarbon fraction that is used as a gasoline blending component, a feedstock for reforming and as a petrochemical feedstock.

NGL - Natural gas liquids.

OSHA - The Occupational Safety and Health Administration.

Petroleum Administration for Defense District (PADD) - Any of five regions in the United States as set forth by the Department of Energy and used throughout the oil industry for geographic reference. Our refineries operate in PADD III, commonly referred to as the Gulf Coast Region.

Petroleum Coke - A coal-like substance produced as a byproduct during the Delayed Coking refining process.

Per barrel of sales - Calculated by dividing the applicable income statement line item (operating margin or operating expenses) by the total barrels sold during the period.

PPB - Parts per billion.

PPM - Parts per million.

RCRA - Resource Conservation and Recovery Act.

Refining margin, refined product margin - Refining margin or refined product margin is measured as the difference between net refining revenues and total refining cost of materials and other and is used as a metric to assess a refinery's product margins against market crack spread trends.

Renewable Fuels Standard 2 (RFS-2) - An EPA regulation promulgated pursuant to the EISA, which requires most refineries to blend increasing amounts of renewable fuels (including biodiesel and ethanol) with refined products.

Renewable Identification Number (RIN) - A renewable fuel credit used to satisfy requirements for blending renewable fuels under RFS-2.

Roofing flux - An asphalt-like product used to make roofing shingles for the housing industry.

Straight run - Product produced off of the crude or vacuum unit and not further processed.

Sweet/Sour crude oil - Terms used to describe the relative sulfur content of crude oil. Sweet crude oil is relatively low in sulfur content; sour crude oil is relatively high in sulfur content. Sweet crude oil requires less processing to remove sulfur and is typically more expensive than sour crude oil.

Throughput - The quantity of crude oil and feedstocks processed through a refinery or a refinery unit.

Turnaround - A periodic shutdown of refinery process units to perform routine maintenance to restore the operation of the equipment to its former level of performance. Turnaround activities normally include cleaning, inspection, refurbishment, and repair and replacement of equipment and piping. It is also common to use turnaround periods to change catalysts or to implement capital project improvements.

Ultra-Low Sulfur Diesel (ULSD) - Diesel fuel produced with a lower sulfur content (15 ppm) to reduce sulfur dioxide emissions. ULSD is the only diesel fuel that may be used for on-road and most other applications in the U.S.

Vacuum Distillation Unit - A refinery unit that distills heavy crude oils under deep vacuum to allow their separation without coking.

West Texas Intermediate Crude Oil (WTI) - A light, sweet crude oil characterized by an API gravity between 38° and 44° and a sulfur content of less than 0.4 wt% that is used as a benchmark for other crude oil.

West Texas Sour Crude Oil (WTS) - A sour crude oil, characterized by an API gravity between 30° and 33° and a sulfur content of approximately 1.28 wt% that is used as a benchmark for other sour crude.

Summary of Risk Factors

An investment in us involves a high degree of risk. Numerous factors, including those discussed below in Item 1A. Risk Factors, may limit our ability to successfully execute our business and growth strategies. You should carefully consider all of the information set forth and incorporated by reference in this Annual Report in deciding whether to invest in the Company. Among these important risks are the following:

•Developments which impact the global oil markets have had, may continue to have, or may have an adverse impact on our business, our future results of operations and our overall financial performance.

•A regional or global disease outbreak could have a material adverse effect on our business, financial condition, results of operation and liquidity.

•A substantial or extended decline in refining margins would reduce our operating results and cash flows and could materially and adversely impact our future rate of growth and the carrying value of our assets.

•We operate in a highly regulated industry and increased costs of compliance with, or liability for violation of, existing or future laws, regulations and other requirements could significantly increase our costs of doing business, thereby adversely affecting our profitability.

•The availability and cost of RINs and other required credits could have a material adverse effect on our financial condition and results of operations.

•Increased supply of and demand for alternative transportation fuels, increased fuel economy standards and increased use of alternative means of transportation could lead to a decrease in transportation fuel prices and/or a reduction in demand for petroleum-based transportation fuels.

•Competition in the refining and logistics industry is intense, and an increase in competition in the markets in which we sell our products could adversely affect our earnings and profitability.

•Our retail segment is subject to loss of market share or pressure to reduce prices in order to compete effectively with a changing group of competitors in a fragmented retail industry.

•We may seek to diversify and expand our retail fuel and convenience store operations, which may present operational and competitive challenges.

•Decreases in commodity prices may lessen our borrowing capacities, increase collateral requirements for derivative instruments or cause a write-down of inventory.

•Acts of terror or sabotage, threats of war, armed conflict, or war may have an adverse impact on our business, our future results of operations and our overall financial performance.

•Legislative and regulatory measures to address climate change and greenhouse gas ("GHG") emissions could increase our operating costs or decrease demand for our refined products.

•Increasing attention to environmental, social and governance matters may impact our business, financial results, cost of capital, or stock price.

•We are particularly vulnerable to disruptions to our refining operations because our refining operations are concentrated in four facilities.

•The physical effects of climate change and severe weather present risks to our operations.

•Our operations are subject to business interruptions and casualty losses. Failure to manage risks associated with business interruptions and casualty losses could adversely impact our operations, financial condition, results of operations and cash flows.

•There are certain environmental hazards and risks inherent in our operations that could adversely affect those operations and our financial results.

•The costs, scope, timelines and benefits of our refining projects may deviate significantly from our original plans and estimates.

•We depend upon our logistics segment for a substantial portion of the crude oil supply and refined product distribution networks that serve our Tyler, Texas, Big Spring, Texas, and El Dorado, Arkansas refineries.

•Interruptions or limitations in the supply and delivery of crude oil, or the supply and distribution of refined products, may negatively affect our refining operations and inhibit the growth of our refining operations.

•We are subject to risks associated with significant investments in the Permian Basin.

•We have made investments in joint ventures which subject us to additional risks, over which we do not have full control and which have unique risks.

•Our retail segment is dependent on fuel sales, which makes us susceptible to increases in the cost of gasoline and interruptions in fuel supply.

•General economic conditions may adversely affect our business, operating results and financial condition.

•We may be adversely affected by the effects of inflation.

•Disruption of our supply chain could adversely impact our ability to refine, manufacture, transport and sell our products.

•Our business could be adversely impacted as a result of our failure to retain or attract key talent.

•We have capital needs to finance our crude oil and refined products inventory for which our internally generated cash flows or other sources of liquidity may not be adequate.

•If there is negative publicity concerning our brand names or the brand names of our suppliers, fuel and merchandise sales in our retail segment may suffer.

•Wholesale cost increases, vendor pricing programs and tax increases applicable to tobacco products, as well as campaigns to discourage their use, could adversely impact our results of operations in our retail segment.

•Our insurance policies historically do not cover all losses, costs or liabilities that we may experience, and insurance companies that currently insure companies in the energy industry may cease to do so or substantially increase premiums.

•Our ongoing study of strategic options to unlock and enhance stockholder value pose additional risks to our business.

•We may not be able to successfully execute our strategy of growth through acquisitions.

•Acquisitions involve risks that could cause our actual growth or operating results to differ adversely compared with our expectations.

•Our future results will suffer if we do not effectively manage our expanded operations.

•We may incur significant costs and liabilities with respect to investigation and remediation of environmental conditions at our facilities.

•We could incur substantial costs or disruptions in our business if we cannot obtain or maintain necessary permits and authorizations or otherwise comply with health, safety, environmental and other laws and regulations.

•Our Tyler refinery currently primarily distributes refined petroleum products via truck or rail. We do not have the ability to distribute these products into markets outside our local market via pipeline.

•An increase in competition, and/or reduction in demand in the markets in which we purchase feedstocks and sell our refined products, could increase our costs and/or lower prices and adversely affect our sales and profitability.

•Compliance with and changes in tax laws could adversely affect our performance.

•Adverse weather conditions or other unforeseen developments could damage our facilities, reduce customer traffic and impair our ability to produce and deliver refined petroleum products or receive supplies for our retail fuel and convenience stores.

•Our operating results are seasonal and generally lower in the first and fourth quarters of the year for our refining and logistics segments and in the first quarter of the year for our retail segment. We depend on favorable weather conditions in the spring and summer months.

•A substantial portion of the workforce at our refineries is unionized, and we may face labor disruptions that would interfere with our operations.

•We rely on information technology in our operations, and any material failure, inadequacy, interruption, cyber-attack or security failure of that technology could harm our business.

•If we lose any of our key personnel, our ability to manage our business and continue our growth could be negatively impacted.

•If we are, or become, a United States ("U.S.") real property holding corporation, special tax rules may apply to a sale, exchange or other disposition of common stock, and non-U.S. holders may be less inclined to invest in our stock, as they may be subject to U.S. federal income tax in certain situations.

•Loss of or reductions to tax incentives for biodiesel production may have a material adverse effect on earnings, profitability and cash flows relating to our renewable fuels facilities.

•Our business requires us to make significant capital expenditures and to maintain and improve our refineries, logistics assets, and retail locations.

•Our business is subject to complex and evolving laws, regulations and security standards regarding privacy, cybersecurity and data protection. Many of these data protection laws are subject to change and uncertain interpretation, and could result in claims, changes to our business practices, monetary penalties, increased cost of operations or other harm to our business.

•If our cost efficiency measures are not successful, we may become less competitive

•The price of our common stock may fluctuate significantly, and you could lose all or part of your investment.

•Stockholder activism may negatively impact the price of our common stock.

•Future sales of shares of our common stock could depress the price of our common stock, and could result in substantial dilution to our stockholders.

•We depend upon our subsidiaries for cash to meet our obligations and pay any dividends.

•We may be unable to pay future regular dividends in the anticipated amounts and frequency set forth herein.

•Provisions of Delaware law and our organizational documents may discourage takeovers and business combinations that our stockholders may consider in their best interests, which could negatively affect our stock price.

•Changes in our credit profile could affect our relationships with our suppliers, which could have a material adverse effect on our liquidity and our ability to operate our refineries at full capacity.

•Our commodity and interest rate derivative activity may limit potential gains, increase potential losses, result in earnings volatility and involve other risks.

•We are exposed to certain counterparty risks which may adversely impact our results of operations.

•From time to time, our cash and credit needs may exceed our internally generated cash flow and available credit, and our business could be materially and adversely affected if we are not able to obtain the necessary cash or credit from financing sources.

•Our debt levels may limit our flexibility in obtaining additional financing and in pursuing other business opportunities.

•Our debt agreements contain operating and financial restrictions that might constrain our business and financing activities.

•Fluctuations in interest rates could materially affect our financial results.

•We may refinance a significant amount of indebtedness and otherwise require additional financing; we cannot guarantee that we will be able to obtain the necessary funds on favorable terms or at all.

•We recorded goodwill and other intangible assets that could become impaired and result in material non-cash charges to our results of operations in the future.

•An impairment of our long-lived assets or goodwill could negatively impact our results of operations and financial condition.

PART I

ITEMS 1 and 2. BUSINESS and PROPERTIES

Company Overview

We are an integrated downstream energy business focused on petroleum refining ("Refining" or our "refining segment"), the transportation, storage and wholesale distribution of crude oil, intermediate and refined products ("Logistics" or our "logistics segment") and convenience store retailing ("Retail" or our "retail segment"). Delek US Holdings, Inc., a Delaware corporation formed in 2016 (a successor to the original Delek US Holdings, Inc. which was a Delaware corporation originally formed in 2001), operates through its consolidated subsidiaries, which include Delek US Energy, Inc. (and its subsidiaries) ("Delek Energy") and Alon (and its subsidiaries).

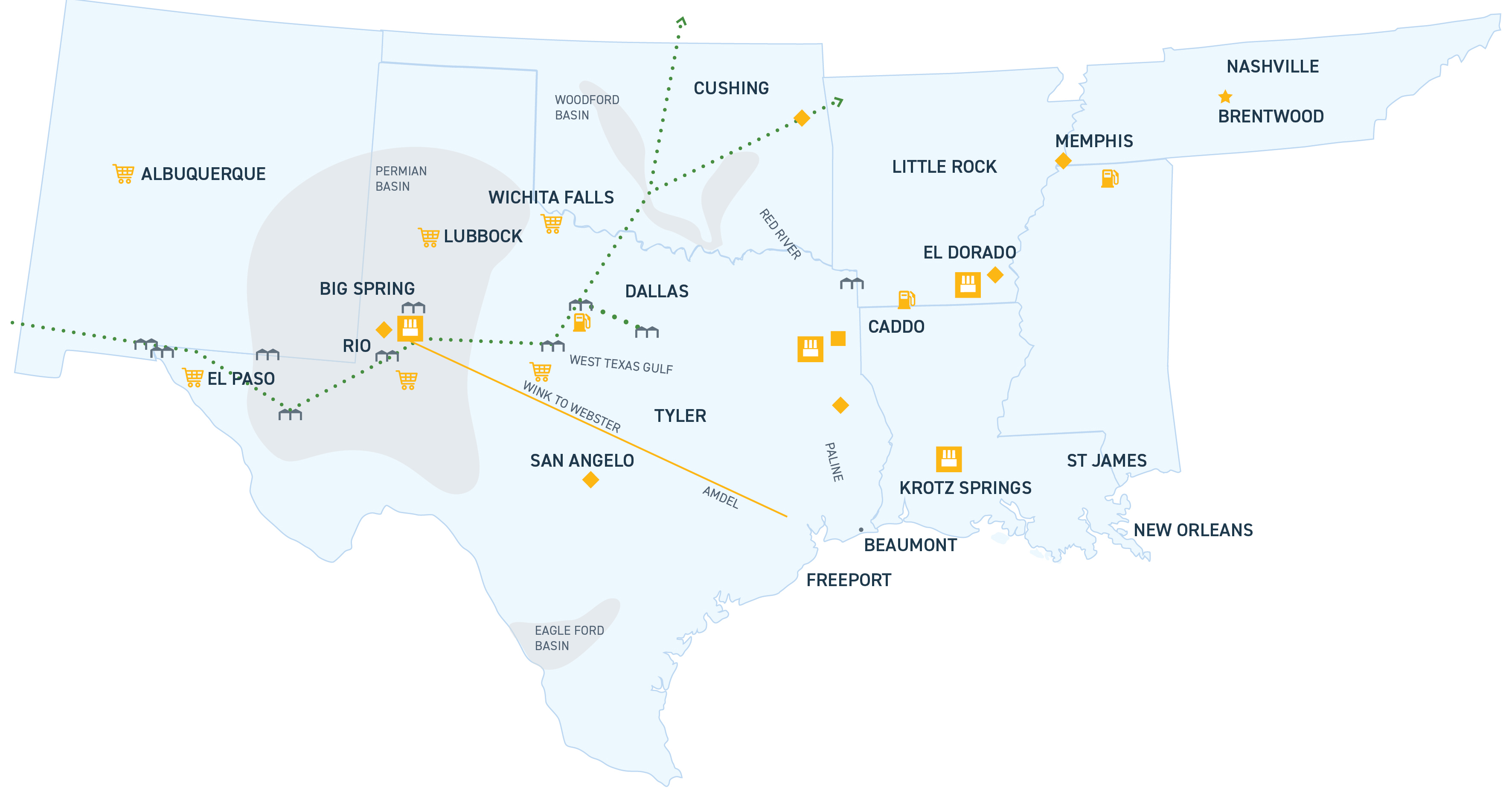

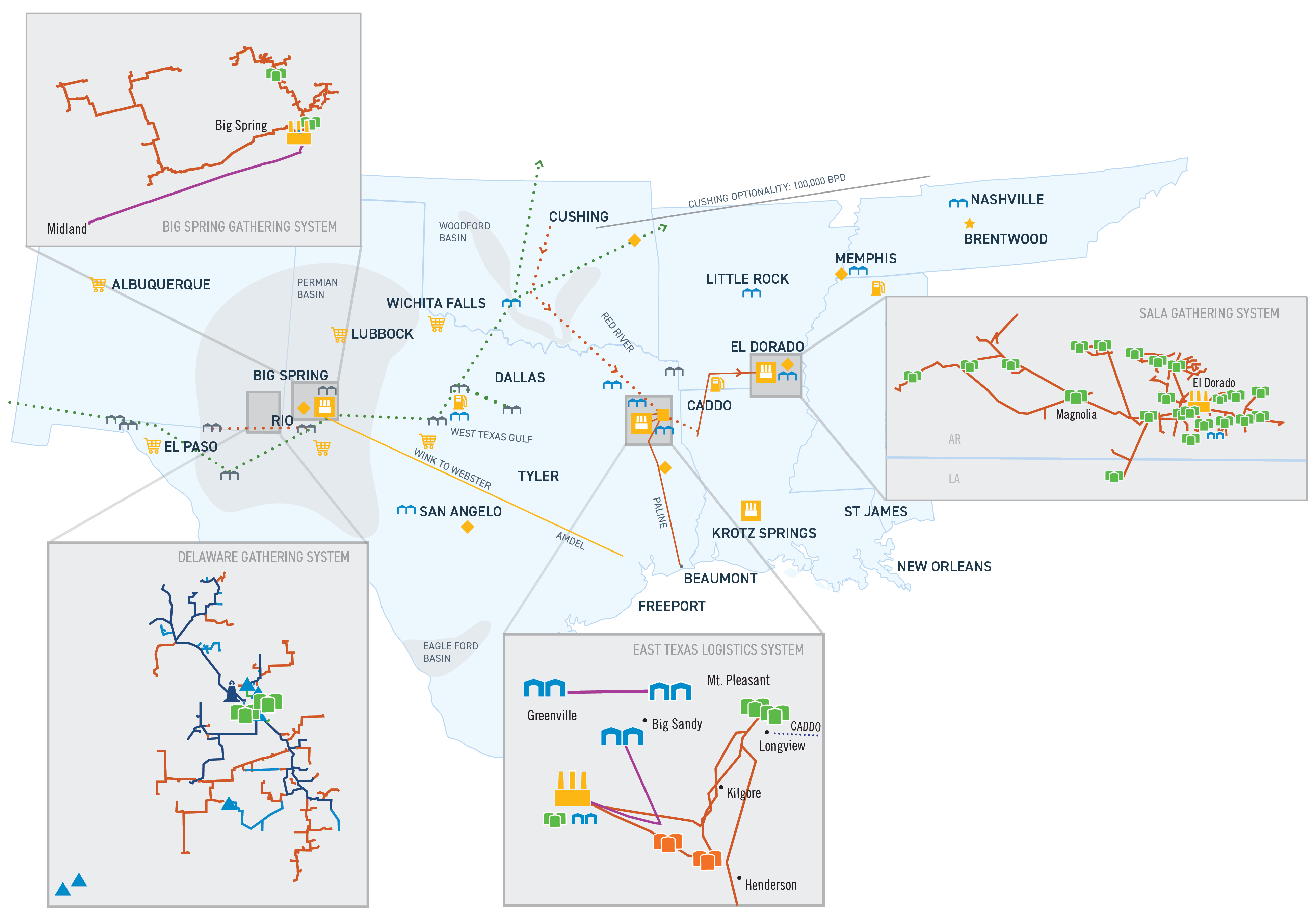

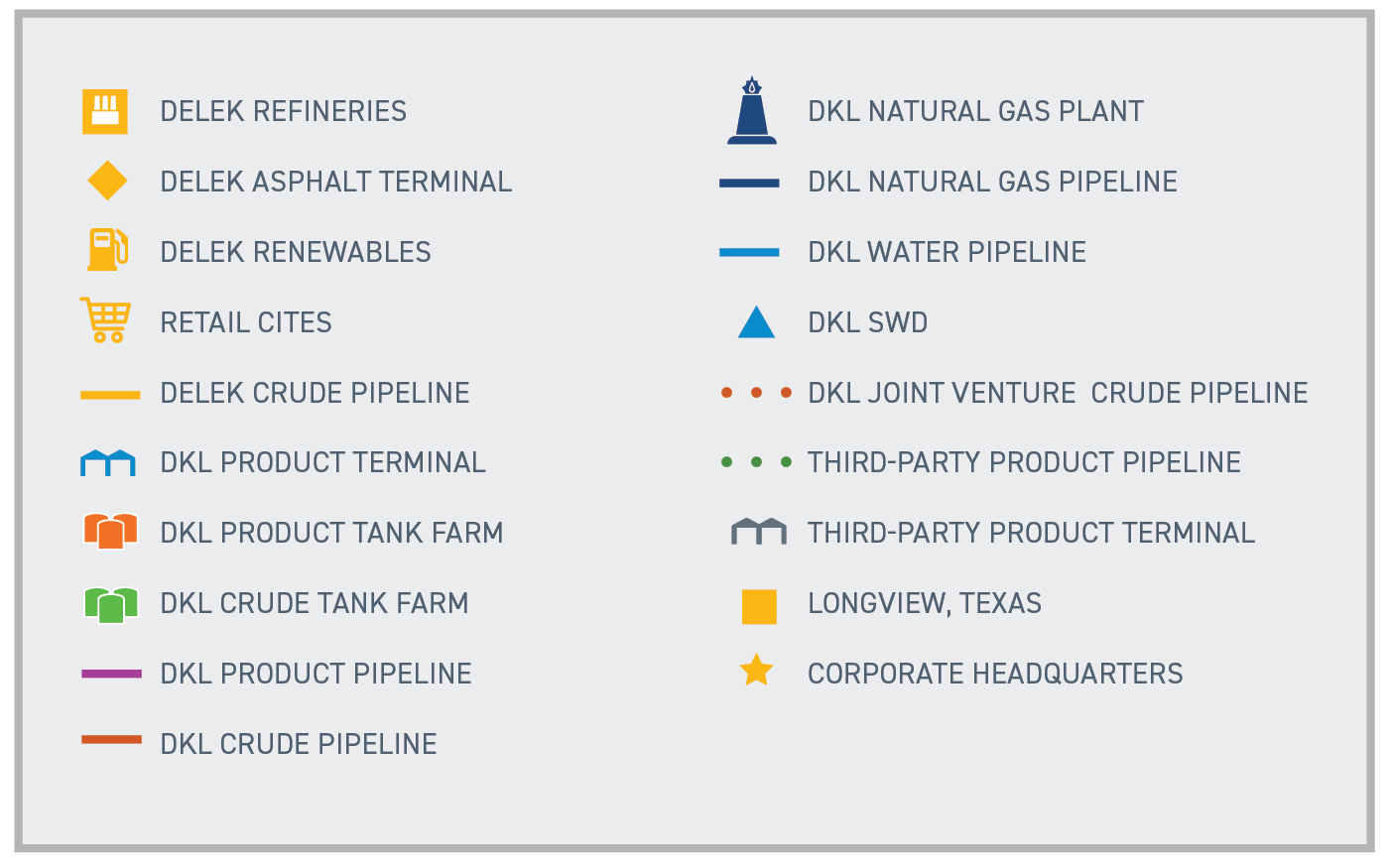

The following map outlines the geography of our integrated downstream energy structure as of December 31, 2023:

| | | | | | | | | | | | | | |

| Refining | | Logistics | | Retail |

302,000 bpd total capacity: | | 9 light product distribution terminals | | 250 stores as of December 31, 2023 |

| Tyler, TX | | Approximately 2,204 miles of pipeline (1) | | Southwest U.S. locations |

| El Dorado, AR | | Approximately 10.0 million barrels of active shell capacity | | Primary source of fuel is Big Spring, TX refinery |

| Big Spring, TX | | Approximately 200 MBbl/d of water disposal capacity | | |

| Krotz Springs, LA | | Approximately 88 MMcf/d of gas processing capacity | | |

WTI primary crude oil supply - 228,000 bpd | | Crude oil pipeline joint ventures: | | |

| Biodiesel facilities with 40 million gallons total | | Red River Pipeline Company LLC | | |

| annual capacity: | | Caddo Pipeline LLC | | |

| Crossett, AR | | Andeavor Logistics RIO Pipeline LLC | | |

| Cleburne, TX | | West Texas wholesale: | | |

| New Albany, MS | | Sale of refined products through terminals | | |

(1) Includes approximately 240 miles of leased capacity and 489 miles of gathering system pipeline which is decommissioned.

Our Vision

It is vitally important that our strategic objectives, especially in view of the evolutionary direction of our macroeconomic and geopolitical environment, involves a process of continuous evaluation of our business model in terms of cost structure, as well as long-term economic and operational sustainability. We are operating in a mature industry (the production, logistics and marketing of hydrocarbons and hydrocarbon-based refined products), with increasingly difficult operational and regulatory challenges and, likewise, pressure on operating costs/gross margins as well as the availability and cost of capital. More consolidation in our industry is expected from increased cost pressures due in part to the regulatory environment continuing to move towards reducing carbon emissions and transitioning to renewable energy in the long-term, however, we believe we are uniquely positioned as a leader of operating and excelling in niche markets and could continue capitalizing on and growing our integrated business model. In order to compete under historic environmental and regulatory changes, companies in our industry will need to be adaptive, forward-thinking and strategic in their approach to long-term sustainability.

The emphasis on environmental responsibility and long-term economic and environmental sustainability has increased. Demand for additional transparency continues to evolve. As we evaluate our current sustainability and ESG positioning in the market, we also must integrate a broader sustainability view to all of our activities, both operational and strategic. We have developed overarching key objectives that guide us when we formulate our strategic plans.

Key Objectives

Certain fundamental principles are foundational to our long-term strategy and direct us as we develop our strategic objectives. With that in mind, we have identified the following overarching key objectives:

I. Operational Excellence

II. Financial Strength and Flexibility

III. Strategic Initiatives

See further discussion in the 'Executive Summary: Strategic Objectives' Section of Item 7. Management's Discussion and Analysis, of this Annual Report on Form 10-K.

Evolving Strategic View

Historically, we have grown through acquisitions in all of our segments. Our business strategy has been focused on capitalizing on and growing our integrated business model in ways that allow us to participate in all phases of the downstream production process, from transporting crude oil to our refineries for processing into refined products to selling fuel to retail customers at the pump. This growth has come from acquisitions or new investments, as well as investments in our existing businesses, as we continue to broaden our existing geographic presence and integrated business model. Our strategy has also included (and continues to include) evaluating certain under-performing and non-core business lines and assets and divesting of those when doing so helps us achieve our strategic objectives.

In connection with the development of our Key Objectives, we have expanded the scope of our growth and business development strategy to one that is also focused on operational, economic and environmental sustainability, including increased emphasis on sustainable carbon efficiency. As an initial foundational change, this expanded scope includes the implementation of an enhanced screening process for proposed future growth projects to incorporate key considerations regarding their environmental and social impact, including quantitative and qualitative data corresponding to several sustainability criteria, such as GHG emissions, carbon intensity, water usage, electricity usage, waste generation, biodiversity impact, and impact on indigenous peoples, among other environmental conscious considerations. This type of data provides management with a more thorough understanding of a project’s potential environmental and social impacts to better make investment decisions that are aligned with our long-term sustainability view. As we move into the future and begin to execute on new growth transactions under the sustainability framework, this data will enable us not only to more closely track the impact we have on both the communities in which we operate and the environment at large, but also to realize the exponential impact of sustainable growth on the long-term value to our stakeholders.

Here are some of our most significant transactions in recent years, all of which continue to have a lasting and important impact on our strategic positioning and long-term value proposition:

| | | | | | | | | | | | | | | | | | | | |

| Date | | Acquired Company/Assets | | Acquired From | | Approximate Purchase Price(1) |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| July 2017 | | Purchased the remaining approximately 53% ownership in Alon that Delek did not already own, in an all-stock transaction, resulting in the addition of the Krotz Springs refinery and the majority ownership in the Big Spring refinery, as well as the addition of our retail segment. | | Shareholders of Alon USA Energy, Inc. | | $530.7 million |

| | | | | | |

| February 2018 | | Purchased the remaining 18.4% ownership in the Alon USA Partners, LP, in an all-equity transaction, representing the remaining interest in the Big Spring refinery operations, which has become one of our best-performing refineries. | | LP unitholders of Alon USA Partners, LP | | $184.7 million |

| May 2019 | | Acquired a 33% membership interest in Red River Pipeline Joint Venture, which continues to be highly accretive to our Logistics segment and one of the principle drivers of our joint venture investment growth. | | Plains Pipeline, L.P. | | $124.7 million |

| July 2019 | | Acquired a 15% membership interest in Wink to Webster Pipeline ("WWP") Joint Venture (which was subsequently converted to an indirect interest via the formation of and contribution to the WWP Project Financing Joint Venture); the WWP JV ramped up operations in 2022 with the completion of long-haul pipeline segments and brings committed volumes that are expected to position the JV for appreciable returns. | | Wink to Webster Pipeline LLC | | $76.3 million |

| June 2022 | | Acquired 100% of the limited liability company interests in 3 Bear from 3 Bear Energy – New Mexico LLC, related to their crude oil and natural gas gathering, processing and transportation businesses, as well as water disposal and recycling operations, located in the Delaware Basin of New Mexico, which enhanced our third party revenues, further diversified of our customer and product mix and, expanded our footprint into the Delaware basin. | | 3 Bear Energy – New Mexico LLC | | $628.3 million |

(1)Includes amounts paid through the date of this Annual Report on Form 10-K. The WWP Project Financing Joint Venture "purchase price" includes our total capital invested to date, which reflects the required capital calls to date under our indirect 15% WWP Joint Venture interest totaling $336.4 million, the majority of which have been financed within the WWP Project Financing Joint Venture. See further discussion in the Notes to our consolidated financial statements included in Item 8. of this Annual Report on Form 10-K.