FY2023PRICE T ROWE GROUP INC0001113169falsehttp://fasb.org/us-gaap/2023#BusinessCombinationContingentConsiderationArrangementsChangeInAmountOfContingentConsiderationLiability1http://fasb.org/us-gaap/2023#AmortizationOfAcquisitionCostshttp://fasb.org/us-gaap/2023#AmortizationOfAcquisitionCostshttp://fasb.org/us-gaap/2023#OtherComprehensiveIncomeLossForeignCurrencyTransactionAndTranslationReclassificationAdjustmentFromAOCIRealizedUponSaleOrLiquidationBeforeTaxhttp://fasb.org/us-gaap/2023#CertificatesOfDepositMemberhttp://fasb.org/us-gaap/2023#CertificatesOfDepositMemberP2YP5Y00011131692023-01-012023-12-3100011131692023-06-30iso4217:USD00011131692024-02-12xbrli:shares00011131692023-12-3100011131692022-12-310001113169us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001113169us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-31iso4217:USDxbrli:shares0001113169us-gaap:AssetManagement1Member2023-01-012023-12-310001113169us-gaap:AssetManagement1Member2022-01-012022-12-310001113169us-gaap:AssetManagement1Member2021-01-012021-12-310001113169trow:CapitalAllocationBasedIncomeMember2023-01-012023-12-310001113169trow:CapitalAllocationBasedIncomeMember2022-01-012022-12-310001113169trow:CapitalAllocationBasedIncomeMember2021-01-012021-12-310001113169trow:AdministrativeDistributionAndServicingMember2023-01-012023-12-310001113169trow:AdministrativeDistributionAndServicingMember2022-01-012022-12-310001113169trow:AdministrativeDistributionAndServicingMember2021-01-012021-12-3100011131692022-01-012022-12-3100011131692021-01-012021-12-310001113169us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-01-012023-12-310001113169us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-01-012022-12-310001113169us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-01-012021-12-310001113169us-gaap:EquityMethodInvesteeMember2023-01-012023-12-310001113169us-gaap:EquityMethodInvesteeMember2022-01-012022-12-310001113169us-gaap:EquityMethodInvesteeMember2021-01-012021-12-310001113169trow:ConsolidatedInvestmentPortfoliosMember2022-12-310001113169trow:ConsolidatedInvestmentPortfoliosMember2021-12-310001113169trow:ConsolidatedInvestmentPortfoliosMember2020-12-3100011131692021-12-3100011131692020-12-310001113169trow:ConsolidatedInvestmentPortfoliosMember2023-12-310001113169us-gaap:CommonStockMember2020-12-310001113169us-gaap:AdditionalPaidInCapitalMember2020-12-310001113169us-gaap:RetainedEarningsUnappropriatedMember2020-12-310001113169us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001113169us-gaap:ParentMember2020-12-310001113169us-gaap:NoncontrollingInterestMember2020-12-310001113169us-gaap:RetainedEarningsUnappropriatedMember2021-01-012021-12-310001113169us-gaap:ParentMember2021-01-012021-12-310001113169us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001113169us-gaap:CommonStockMember2021-01-012021-12-310001113169us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001113169us-gaap:RestrictedStockMemberus-gaap:CommonStockMember2021-01-012021-12-310001113169us-gaap:RestrictedStockUnitsRSUMemberus-gaap:CommonStockMember2021-01-012021-12-310001113169us-gaap:AdditionalPaidInCapitalMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001113169us-gaap:ParentMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001113169us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001113169us-gaap:NoncontrollingInterestMember2021-01-012021-12-310001113169us-gaap:CommonStockMember2021-12-310001113169us-gaap:AdditionalPaidInCapitalMember2021-12-310001113169us-gaap:RetainedEarningsUnappropriatedMember2021-12-310001113169us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001113169us-gaap:ParentMember2021-12-310001113169us-gaap:NoncontrollingInterestMember2021-12-310001113169us-gaap:RetainedEarningsUnappropriatedMember2022-01-012022-12-310001113169us-gaap:ParentMember2022-01-012022-12-310001113169us-gaap:NoncontrollingInterestMember2022-01-012022-12-310001113169us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310001113169us-gaap:CommonStockMember2022-01-012022-12-310001113169us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001113169us-gaap:RestrictedStockMemberus-gaap:CommonStockMember2022-01-012022-12-310001113169us-gaap:RestrictedStockUnitsRSUMemberus-gaap:CommonStockMember2022-01-012022-12-310001113169us-gaap:AdditionalPaidInCapitalMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001113169us-gaap:ParentMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001113169us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001113169us-gaap:CommonStockMember2022-12-310001113169us-gaap:AdditionalPaidInCapitalMember2022-12-310001113169us-gaap:RetainedEarningsUnappropriatedMember2022-12-310001113169us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001113169us-gaap:ParentMember2022-12-310001113169us-gaap:NoncontrollingInterestMember2022-12-310001113169us-gaap:RetainedEarningsUnappropriatedMember2023-01-012023-12-310001113169us-gaap:ParentMember2023-01-012023-12-310001113169us-gaap:NoncontrollingInterestMember2023-01-012023-12-310001113169us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310001113169us-gaap:CommonStockMember2023-01-012023-12-310001113169us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310001113169us-gaap:RestrictedStockMemberus-gaap:CommonStockMember2023-01-012023-12-310001113169us-gaap:RestrictedStockUnitsRSUMemberus-gaap:CommonStockMember2023-01-012023-12-310001113169us-gaap:AdditionalPaidInCapitalMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001113169us-gaap:ParentMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001113169us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001113169us-gaap:CommonStockMember2023-12-310001113169us-gaap:AdditionalPaidInCapitalMember2023-12-310001113169us-gaap:RetainedEarningsUnappropriatedMember2023-12-310001113169us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-310001113169us-gaap:ParentMember2023-12-310001113169us-gaap:NoncontrollingInterestMember2023-12-310001113169trow:ComputerAndCommunicationsSoftwareAndEquipmentMember2023-12-310001113169us-gaap:BuildingAndBuildingImprovementsMember2023-12-310001113169us-gaap:LeaseholdImprovementsMember2023-12-310001113169us-gaap:FurnitureAndFixturesMember2023-12-310001113169trow:InvestmentAdvisoryAgreementsMember2023-12-31trow:businesstrow:obligation0001113169us-gaap:InvestmentAdviceMember2023-12-310001113169us-gaap:DistributionServiceMember2023-12-310001113169us-gaap:AdministrativeServiceMember2023-12-310001113169trow:OherAdministrativeServiceMember2023-12-310001113169trow:EmployeeStockBasedCompensationProgramsMember2023-12-31trow:share_based_compensation_plan0001113169trow:DirectorPlansMember2023-12-310001113169trow:A2020LongTermIncentivePlanAndThe2017NonEmployeeDirectorEquityPlanMember2023-12-310001113169trow:EmployeeStockBasedCompensationProgramsMembertrow:RestrictedStockAndRestrictedStockUnitsMember2023-01-012023-12-310001113169us-gaap:EmployeeStockOptionMembertrow:EmployeeStockBasedCompensationProgramsMember2023-01-012023-12-310001113169us-gaap:EmployeeStockOptionMembertrow:DirectorPlansMember2023-01-012023-12-310001113169trow:A2017NonEmployeeDirectorEquityPlanMember2023-01-012023-12-310001113169us-gaap:MoneyMarketFundsMember2023-01-012023-12-310001113169us-gaap:MoneyMarketFundsMember2022-01-012022-12-310001113169us-gaap:MoneyMarketFundsMember2021-01-012021-12-310001113169us-gaap:AssetManagement1Membertrow:InvestmentAdvisoryClientsMemberus-gaap:EquitySecuritiesMember2023-01-012023-12-310001113169us-gaap:AssetManagement1Membertrow:InvestmentAdvisoryClientsMemberus-gaap:EquitySecuritiesMember2022-01-012022-12-310001113169us-gaap:AssetManagement1Membertrow:InvestmentAdvisoryClientsMemberus-gaap:EquitySecuritiesMember2021-01-012021-12-310001113169us-gaap:AssetManagement1Membertrow:FixedIncomeIncludingMoneyMarketMembertrow:InvestmentAdvisoryClientsMember2023-01-012023-12-310001113169us-gaap:AssetManagement1Membertrow:FixedIncomeIncludingMoneyMarketMembertrow:InvestmentAdvisoryClientsMember2022-01-012022-12-310001113169us-gaap:AssetManagement1Membertrow:FixedIncomeIncludingMoneyMarketMembertrow:InvestmentAdvisoryClientsMember2021-01-012021-12-310001113169us-gaap:AssetManagement1Membertrow:InvestmentAdvisoryClientsMembertrow:MultiAssetMember2023-01-012023-12-310001113169us-gaap:AssetManagement1Membertrow:InvestmentAdvisoryClientsMembertrow:MultiAssetMember2022-01-012022-12-310001113169us-gaap:AssetManagement1Membertrow:InvestmentAdvisoryClientsMembertrow:MultiAssetMember2021-01-012021-12-310001113169us-gaap:AssetManagement1Membertrow:AlternativesInvestmentMembertrow:InvestmentAdvisoryClientsMember2023-01-012023-12-310001113169us-gaap:AssetManagement1Membertrow:AlternativesInvestmentMembertrow:InvestmentAdvisoryClientsMember2022-01-012022-12-310001113169us-gaap:AssetManagement1Membertrow:AlternativesInvestmentMembertrow:InvestmentAdvisoryClientsMember2021-01-012021-12-310001113169us-gaap:AssetManagement1Membertrow:InvestmentAdvisoryClientsMember2023-01-012023-12-310001113169us-gaap:AssetManagement1Membertrow:InvestmentAdvisoryClientsMember2022-01-012022-12-310001113169us-gaap:AssetManagement1Membertrow:InvestmentAdvisoryClientsMember2021-01-012021-12-310001113169us-gaap:AssetManagement1Memberus-gaap:EquitySecuritiesMembertrow:AssetsUnderManagementMember2023-01-012023-12-310001113169us-gaap:AssetManagement1Memberus-gaap:EquitySecuritiesMembertrow:AssetsUnderManagementMember2022-01-012022-12-310001113169us-gaap:AssetManagement1Memberus-gaap:EquitySecuritiesMembertrow:AssetsUnderManagementMember2021-01-012021-12-310001113169us-gaap:AssetManagement1Membertrow:FixedIncomeIncludingMoneyMarketMembertrow:AssetsUnderManagementMember2023-01-012023-12-310001113169us-gaap:AssetManagement1Membertrow:FixedIncomeIncludingMoneyMarketMembertrow:AssetsUnderManagementMember2022-01-012022-12-310001113169us-gaap:AssetManagement1Membertrow:FixedIncomeIncludingMoneyMarketMembertrow:AssetsUnderManagementMember2021-01-012021-12-310001113169us-gaap:AssetManagement1Membertrow:AssetsUnderManagementMembertrow:MultiAssetMember2023-01-012023-12-310001113169us-gaap:AssetManagement1Membertrow:AssetsUnderManagementMembertrow:MultiAssetMember2022-01-012022-12-310001113169us-gaap:AssetManagement1Membertrow:AssetsUnderManagementMembertrow:MultiAssetMember2021-01-012021-12-310001113169us-gaap:AssetManagement1Membertrow:AlternativesInvestmentMembertrow:AssetsUnderManagementMember2023-01-012023-12-310001113169us-gaap:AssetManagement1Membertrow:AlternativesInvestmentMembertrow:AssetsUnderManagementMember2022-01-012022-12-310001113169us-gaap:AssetManagement1Membertrow:AlternativesInvestmentMembertrow:AssetsUnderManagementMember2021-01-012021-12-310001113169us-gaap:AssetManagement1Membertrow:AssetsUnderManagementMember2023-01-012023-12-310001113169us-gaap:AssetManagement1Membertrow:AssetsUnderManagementMember2022-01-012022-12-310001113169us-gaap:AssetManagement1Membertrow:AssetsUnderManagementMember2021-01-012021-12-310001113169trow:SponsoredInvestmentPortfoliosMember2023-01-012023-12-310001113169trow:SponsoredInvestmentPortfoliosMember2022-01-012022-12-310001113169trow:SponsoredInvestmentPortfoliosMember2021-01-012021-12-310001113169trow:SponsoredInvestmentPortfoliosMember2023-12-310001113169trow:SponsoredInvestmentPortfoliosMember2022-12-310001113169us-gaap:GeographicConcentrationRiskMemberus-gaap:NonUsMembertrow:InvestmentAdvisoryClientsMembertrow:AssetsUnderManagementMember2023-01-012023-12-31xbrli:pure0001113169us-gaap:GeographicConcentrationRiskMemberus-gaap:NonUsMembertrow:InvestmentAdvisoryClientsMembertrow:AssetsUnderManagementMember2022-01-012022-12-310001113169trow:SponsoredInvestmentPortfoliosDiscretionaryInvestmentsMember2023-12-310001113169trow:SponsoredInvestmentPortfoliosDiscretionaryInvestmentsMember2022-12-310001113169trow:SponsoredInvestmentPortfoliosSeedCapitalMember2023-12-310001113169trow:SponsoredInvestmentPortfoliosSeedCapitalMember2022-12-310001113169trow:SponsoredInvestmentPortfoliosSupplementalSavingsPlanLiabilityEconomicHedgesMember2023-12-310001113169trow:SponsoredInvestmentPortfoliosSupplementalSavingsPlanLiabilityEconomicHedgesMember2022-12-310001113169trow:InvestmentPartnershipsAndOtherInvestmentsMember2023-12-310001113169trow:InvestmentPartnershipsAndOtherInvestmentsMember2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2022-12-310001113169trow:UtiAssetManagementCompanyIndiaMember2023-12-310001113169trow:UtiAssetManagementCompanyIndiaMember2022-12-310001113169trow:InvestmentsInAffiliatedPrivateInvestmentFundsCarriedInterestMember2023-12-310001113169trow:InvestmentsInAffiliatedPrivateInvestmentFundsCarriedInterestMember2022-12-310001113169trow:InvestmentsInAffiliatedPrivateInvestmentFundsSeedCoInvestmentMember2023-12-310001113169trow:InvestmentsInAffiliatedPrivateInvestmentFundsSeedCoInvestmentMember2022-12-310001113169trow:InvestmentsInAffiliatedCollateralizedLoanObligationsMember2023-12-310001113169trow:InvestmentsInAffiliatedCollateralizedLoanObligationsMember2022-12-310001113169us-gaap:USTreasurySecuritiesMember2023-12-310001113169us-gaap:USTreasurySecuritiesMember2022-12-310001113169trow:SponsoredInvestmentPortfoliosSeedCapitalMember2023-01-012023-12-310001113169trow:SponsoredInvestmentPortfoliosSeedCapitalMember2022-01-012022-12-310001113169trow:SponsoredInvestmentPortfoliosSeedCapitalMember2021-01-012021-12-310001113169us-gaap:AssetsMember2023-01-012023-12-310001113169us-gaap:AssetsMember2022-01-012022-12-310001113169us-gaap:AssetsMember2021-01-012021-12-310001113169us-gaap:LiabilityMember2023-01-012023-12-310001113169us-gaap:LiabilityMember2022-01-012022-12-310001113169us-gaap:LiabilityMember2021-01-012021-12-310001113169trow:RedeemableNoncontrollingInterestMember2023-01-012023-12-310001113169trow:RedeemableNoncontrollingInterestMember2022-01-012022-12-310001113169trow:RedeemableNoncontrollingInterestMember2021-01-012021-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:ReclassificationOutOfAccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:ReclassificationOutOfAccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:ReclassificationOutOfAccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001113169trow:VerticalStripInvestmentMembertrow:InvestmentsInEuropeanCollateralizedLoanObligationsMember2023-12-310001113169us-gaap:AccountsPayableAndAccruedLiabilitiesMembertrow:InvestmentsInAffiliatedCollateralizedLoanObligationsMember2023-12-310001113169us-gaap:AccountsPayableAndAccruedLiabilitiesMembertrow:InvestmentsInAffiliatedCollateralizedLoanObligationsMember2022-12-31iso4217:EUR0001113169trow:InvestmentsInAffiliatedCollateralizedLoanObligationsMembertrow:EuroInterbankOfferRateEURIBORMembersrt:MinimumMember2023-12-310001113169trow:InvestmentsInAffiliatedCollateralizedLoanObligationsMembertrow:EuroInterbankOfferRateEURIBORMembersrt:MaximumMember2023-12-310001113169us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2023-12-310001113169us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMembertrow:SponsoredInvestmentPortfoliosDiscretionaryInvestmentsMemberus-gaap:FairValueInputsLevel1Member2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Membertrow:SponsoredInvestmentPortfoliosDiscretionaryInvestmentsMember2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membertrow:SponsoredInvestmentPortfoliosDiscretionaryInvestmentsMember2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMembertrow:SponsoredInvestmentPortfoliosDiscretionaryInvestmentsMemberus-gaap:FairValueInputsLevel1Member2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Membertrow:SponsoredInvestmentPortfoliosDiscretionaryInvestmentsMember2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membertrow:SponsoredInvestmentPortfoliosDiscretionaryInvestmentsMember2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMembertrow:SponsoredInvestmentPortfoliosSeedCapitalMemberus-gaap:FairValueInputsLevel1Member2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Membertrow:SponsoredInvestmentPortfoliosSeedCapitalMember2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membertrow:SponsoredInvestmentPortfoliosSeedCapitalMember2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMembertrow:SponsoredInvestmentPortfoliosSeedCapitalMemberus-gaap:FairValueInputsLevel1Member2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Membertrow:SponsoredInvestmentPortfoliosSeedCapitalMember2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membertrow:SponsoredInvestmentPortfoliosSeedCapitalMember2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMembertrow:SponsoredInvestmentPortfoliosSupplementalSavingsPlanLiabilityEconomicHedgesMemberus-gaap:FairValueInputsLevel1Member2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMembertrow:SponsoredInvestmentPortfoliosSupplementalSavingsPlanLiabilityEconomicHedgesMemberus-gaap:FairValueInputsLevel2Member2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMembertrow:SponsoredInvestmentPortfoliosSupplementalSavingsPlanLiabilityEconomicHedgesMemberus-gaap:FairValueInputsLevel3Member2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMembertrow:SponsoredInvestmentPortfoliosSupplementalSavingsPlanLiabilityEconomicHedgesMemberus-gaap:FairValueInputsLevel1Member2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMembertrow:SponsoredInvestmentPortfoliosSupplementalSavingsPlanLiabilityEconomicHedgesMemberus-gaap:FairValueInputsLevel2Member2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMembertrow:SponsoredInvestmentPortfoliosSupplementalSavingsPlanLiabilityEconomicHedgesMemberus-gaap:FairValueInputsLevel3Member2022-12-310001113169us-gaap:FairValueMeasuredAtNetAssetValuePerShareMember2023-12-310001113169us-gaap:FairValueMeasuredAtNetAssetValuePerShareMember2022-12-310001113169trow:OHAAcquisitionMember2021-12-290001113169trow:OHAAcquisitionMember2021-12-292021-12-290001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2021-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2023-01-012023-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2022-01-012022-12-310001113169srt:ReportableLegalEntitiesMembertrow:VotingInterestEntitiesMember2023-12-310001113169srt:ReportableLegalEntitiesMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001113169srt:ReportableLegalEntitiesMembertrow:ConsolidatedInvestmentPortfoliosMember2023-12-310001113169srt:ReportableLegalEntitiesMembertrow:VotingInterestEntitiesMember2022-12-310001113169srt:ReportableLegalEntitiesMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-310001113169srt:ReportableLegalEntitiesMembertrow:ConsolidatedInvestmentPortfoliosMember2022-12-310001113169srt:ReportableLegalEntitiesMembertrow:SponsoredInvestmentPortfoliosMemberus-gaap:MoneyMarketFundsMembertrow:ConsolidatedInvestmentPortfoliosMember2023-12-310001113169srt:ReportableLegalEntitiesMembertrow:SponsoredInvestmentPortfoliosMemberus-gaap:MoneyMarketFundsMembertrow:ConsolidatedInvestmentPortfoliosMember2022-12-310001113169srt:ReportableLegalEntitiesMembertrow:SponsoredInvestmentPortfoliosMembertrow:ConsolidatedInvestmentPortfoliosMember2023-12-310001113169srt:ReportableLegalEntitiesMembertrow:SponsoredInvestmentPortfoliosMembertrow:ConsolidatedInvestmentPortfoliosMember2022-12-310001113169srt:ReportableLegalEntitiesMembertrow:VotingInterestEntitiesMember2023-01-012023-12-310001113169srt:ReportableLegalEntitiesMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-01-012023-12-310001113169srt:ReportableLegalEntitiesMembertrow:ConsolidatedInvestmentPortfoliosMember2023-01-012023-12-310001113169srt:ReportableLegalEntitiesMembertrow:VotingInterestEntitiesMember2022-01-012022-12-310001113169srt:ReportableLegalEntitiesMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-01-012022-12-310001113169srt:ReportableLegalEntitiesMembertrow:ConsolidatedInvestmentPortfoliosMember2022-01-012022-12-310001113169srt:ReportableLegalEntitiesMembertrow:VotingInterestEntitiesMember2021-01-012021-12-310001113169srt:ReportableLegalEntitiesMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-01-012021-12-310001113169srt:ReportableLegalEntitiesMembertrow:ConsolidatedInvestmentPortfoliosMember2021-01-012021-12-310001113169trow:VotingInterestEntitiesMember2023-01-012023-12-310001113169trow:ConsolidatedInvestmentPortfoliosMember2023-01-012023-12-310001113169trow:VotingInterestEntitiesMember2022-01-012022-12-310001113169trow:ConsolidatedInvestmentPortfoliosMember2022-01-012022-12-310001113169trow:VotingInterestEntitiesMember2021-01-012021-12-310001113169trow:ConsolidatedInvestmentPortfoliosMember2021-01-012021-12-310001113169srt:ConsolidationEliminationsMember2023-01-012023-12-310001113169srt:ConsolidationEliminationsMember2022-01-012022-12-310001113169srt:ConsolidationEliminationsMember2021-01-012021-12-310001113169srt:ReportableLegalEntitiesMembertrow:VotingInterestEntitiesMember2021-12-310001113169srt:ReportableLegalEntitiesMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-12-310001113169srt:ReportableLegalEntitiesMembertrow:ConsolidatedInvestmentPortfoliosMember2021-12-310001113169srt:ReportableLegalEntitiesMembertrow:VotingInterestEntitiesMember2020-12-310001113169srt:ReportableLegalEntitiesMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2020-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Membertrow:ConsolidatedInvestmentPortfoliosMember2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Membertrow:ConsolidatedInvestmentPortfoliosMember2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membertrow:ConsolidatedInvestmentPortfoliosMember2023-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Membertrow:ConsolidatedInvestmentPortfoliosMember2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Membertrow:ConsolidatedInvestmentPortfoliosMember2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membertrow:ConsolidatedInvestmentPortfoliosMember2022-12-310001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMembertrow:ConsolidatedInvestmentPortfoliosMember2022-12-31trow:alternative_energy_credit0001113169us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membersrt:MaximumMembertrow:ConsolidatedInvestmentPortfoliosMember2022-12-310001113169trow:ComputerAndCommunicationsSoftwareAndEquipmentMember2022-12-310001113169us-gaap:BuildingAndBuildingImprovementsMember2022-12-310001113169us-gaap:LeaseholdImprovementsMember2022-12-310001113169us-gaap:FurnitureAndFixturesMember2022-12-310001113169us-gaap:LandMember2023-12-310001113169us-gaap:LandMember2022-12-310001113169us-gaap:SoftwareDevelopmentMember2023-01-012023-12-310001113169us-gaap:SoftwareDevelopmentMember2022-01-012022-12-310001113169us-gaap:SoftwareDevelopmentMember2021-01-012021-12-310001113169us-gaap:TradeNamesMember2023-12-310001113169us-gaap:TradeNamesMember2022-12-310001113169trow:InvestmentAdvisoryAgreementsMember2023-12-310001113169trow:InvestmentAdvisoryAgreementsMember2022-12-310001113169trow:InvestmentAdvisoryAgreementsMember2022-12-310001113169trow:InvestmentAdvisoryAgreementsMember2022-01-012022-12-310001113169us-gaap:TradeNamesMember2022-01-012022-12-310001113169trow:InvestmentAdvisoryAgreementsMember2023-01-012023-12-3100011131692021-06-140001113169us-gaap:StockCompensationPlanMember2023-12-310001113169us-gaap:EmployeeStockMember2023-12-310001113169us-gaap:EmployeeStockOptionMembertrow:CompensationAndRelatedCostMember2023-01-012023-12-310001113169us-gaap:EmployeeStockOptionMembertrow:CompensationAndRelatedCostMember2022-01-012022-12-310001113169us-gaap:RestrictedStockMember2022-12-310001113169us-gaap:RestrictedStockUnitsRSUMember2022-12-310001113169us-gaap:RestrictedStockMember2023-01-012023-12-310001113169us-gaap:RestrictedStockMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2023-01-012023-12-310001113169us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2023-01-012023-12-310001113169us-gaap:ShareBasedCompensationAwardTrancheTwoMember2023-01-012023-12-310001113169us-gaap:RestrictedStockMember2023-12-310001113169us-gaap:RestrictedStockUnitsRSUMember2023-12-310001113169us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2023-12-310001113169trow:CompensationAndRelatedCostMembertrow:RestrictedStockAndRestrictedStockUnitsMember2023-01-012023-12-310001113169trow:CompensationAndRelatedCostMembertrow:RestrictedStockAndRestrictedStockUnitsMember2022-01-012022-12-310001113169trow:CompensationAndRelatedCostMembertrow:RestrictedStockAndRestrictedStockUnitsMember2021-01-012021-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMember2023-01-012023-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMember2022-01-012022-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMember2021-01-012021-12-310001113169trow:AccumulatedForeignCurrencyAdjustmentAttributableToParentDeconsolidationMember2023-01-012023-12-310001113169trow:AccumulatedForeignCurrencyAdjustmentAttributableToParentDeconsolidationMember2022-01-012022-12-310001113169trow:AccumulatedForeignCurrencyAdjustmentAttributableToParentDeconsolidationMember2021-01-012021-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:EquityMethodInvesteeMember2020-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2020-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMember2020-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:EquityMethodInvesteeMember2021-01-012021-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-01-012021-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:EquityMethodInvesteeMember2021-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMember2021-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:EquityMethodInvesteeMember2022-01-012022-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-01-012022-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:EquityMethodInvesteeMember2022-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMember2022-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:EquityMethodInvesteeMember2023-01-012023-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-01-012023-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:EquityMethodInvesteeMember2023-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001113169us-gaap:AccumulatedTranslationAdjustmentMember2023-12-310001113169trow:OHACommitmentsMember2023-12-310001113169srt:ExecutiveOfficerMemberus-gaap:DeferredBonusMember2023-12-310001113169srt:ExecutiveOfficerMemberus-gaap:DeferredBonusMember2023-01-012023-12-310001113169srt:ExecutiveOfficerMemberus-gaap:DeferredBonusMember2021-01-012021-12-310001113169srt:ExecutiveOfficerMemberus-gaap:DeferredBonusMember2022-12-310001113169srt:ExecutiveOfficerMemberus-gaap:DeferredBonusMember2021-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2023

Commission file number 000-32191

T. ROWE PRICE GROUP, INC.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Maryland | | 52-2264646 |

| State of incorporation | | IRS Employer Identification No. |

100 East Pratt Street, Baltimore, Maryland 21202

Address, including zip code, of principal executive offices

(410) 345-2000

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act: | | | | | | | | |

| Common stock, $.20 par value per share | TROW | The NASDAQ Stock Market LLC |

| (Title of class) | (Ticker symbol) | (Name of exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months, and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulations S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | ☒ | Accelerated filer | ☐ |

| Non-accelerated filer (do not check if smaller reporting company) | ☐ | Smaller reporting company | ☐ |

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to Section 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☒ No

The aggregate market value of the common equity (all voting) held by non-affiliates (excludes executive officers and directors) computed using $112.02 per share (the NASDAQ Official Closing Price on June 30, 2023, the last business day of the registrant’s most recently completed second fiscal quarter) was $24.6 billion.

The number of shares outstanding of the registrant's common stock as of the latest practicable date, February 12, 2024, is 223,656,595.

DOCUMENTS INCORPORATED BY REFERENCE: Certain portions of the registrant's Definitive Proxy Statement for the 2024 Annual Meeting of Stockholders, to be filed pursuant to Regulation 14A of the general rules and regulations under the Act, are incorporated by reference into Part III of this report.

Exhibit index begins on page 94.

| | | | | | | | |

| | PAGE |

| | |

| ITEM 1. | Business | |

| ITEM 1A. | | |

| ITEM 1B. | | |

| ITEM 1C. | Cybersecurity | |

| ITEM 2. | | |

| ITEM 3. | | |

| ITEM 4. | | |

| | |

| | |

| | |

| ITEM 5. | | |

| ITEM 6. | Reserved | |

| ITEM 7. | | |

| ITEM 7A. | | |

| ITEM 8. | | |

| ITEM 9. | | |

| ITEM 9A. | Controls and Procedures | |

| ITEM 9B. | Other Information | |

| ITEM 9C. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | |

| | |

| | |

| ITEM 10. | | |

| ITEM 11. | | |

| ITEM 12. | | |

| ITEM 13. | | |

| ITEM 14. | | |

| | |

| | |

| ITEM 15. | | |

| ITEM 16. | Form 10-K Summary | |

| |

PART I

Item 1.Business.

T. Rowe Price Group, Inc. ("T. Rowe Price Group", "T. Rowe Price", "the firm", "we", "us", or "our") is a financial services holding company that provides global investment management services through its subsidiaries to investors worldwide. We are driven by our purpose: to identify and actively invest in opportunities to help people thrive in an evolving world. With more than 80 years of experience, we provide a broad range of investment solutions across equity, fixed income, multi-asset, and alternative capabilities for clients around the world— from individuals to advisors to institutions to retirement plan sponsors. We also provide certain investment advisory clients with related administrative services, including distribution, mutual fund transfer agent, accounting, and shareholder services; participant recordkeeping and transfer agent services for defined contribution retirement plans; brokerage; trust services; and non-discretionary advisory services through model delivery. We take an active, independent approach to investing, offering our dynamic perspective and meaningful partnership, so our clients can feel more confident.

The late Thomas Rowe Price, Jr., founded our firm in 1937, and the common stock of T. Rowe Price Associates, Inc. was first offered to the public in 1986. The T. Rowe Price Group, Inc. corporate holding company structure was established in 2000. Our common stock trades on the NASDAQ Global Select Market under the symbol "TROW".

Our core capabilities have enabled us to deliver excellent operating results since our initial public offering. We maintain a strong corporate culture that is focused on delivering strong long-term investment performance and world-class service to our clients. We distribute our broad array of active investment solutions through a diverse set of distribution channels and vehicles to meet the needs of our clients globally. These vehicles include an array of U.S. mutual funds, collective investment trusts, subadvised funds, separately managed accounts, and other sponsored products. The other sponsored products include: open-ended investment products offered to investors outside the U.S., products offered through variable annuity life insurance plans in the U.S., affiliated private investment funds and collateralized loan obligations.

The investment management industry has been evolving and industry participants are facing several challenging trends including passive investments taking market share from traditional active strategies; continued downward fee pressure; demand for new investment vehicles to meet client needs; and an ever-changing regulatory landscape. It is also a unique time in our industry with a significant amount of money remaining out of the market as investors maintain a shorter investment time horizon and relatively low risk appetite.

Despite these challenging trends, we believe there are significant opportunities that align to our core capabilities. Our ongoing financial strength and discipline allows us to respond to these opportunities with several strategic, multi-year initiatives that are designed to strengthen our long-term competitive position and to:

•Sustain our leadership position in retirement.

•Access growth of the U.S. wealth management channel through improved vehicle capabilities, technology, specialist sales, and content.

•Focus on further global growth in select high-opportunity countries where we have existing business by investing more in resources, products, and marketing.

•Deepen client relationships and renew our individual investor base by innovating and investing in our capabilities to deliver world class service and a differentiated offer to clients.

•Broaden our reach in the private and alternatives market by leveraging our distribution channels and expanding our investment capabilities.

•Strengthen our distribution technology to enhance the digital client experience and client reporting.

•Attract and retain top talent, enable effective hybrid collaboration, and deliver on our expanded diversity, equity, and inclusion goals.

•Nurture our brand globally and leverage it effectively across channels and geographies.

•Deliver strong financial results and balance sheet strength for our stockholders over the long term.

ASSETS UNDER MANAGEMENT (AUM).

During 2023, we derived most of our consolidated net revenues and net income from investment advisory services provided by our subsidiaries, primarily T. Rowe Price Associates (TRPA), T. Rowe Price Investment Management (TRPIM), Oak Hill Advisors (OHA), and T. Rowe Price International Ltd (TRPIL). Our revenues depend largely on the total value and composition of our assets under management. Accordingly, fluctuations in financial markets and in the composition of assets under management impact our revenues and results of operations.

At December 31, 2023, we had $1,444.5 billion in assets under management, an increase of $169.8 billion from 2022. This increase in assets under management was driven by market appreciation, net of distributions not reinvested, of $251.6 billion, offset by net cash outflows of $81.8 billion.

In 2023, our target date retirement products experienced net cash inflows of $13.1 billion. The assets under management in our target date retirement products totaled $408.4 billion at December 31, 2023, or 28.3% of our managed assets at December 31, 2023, compared with 26.2% at the end of 2022.

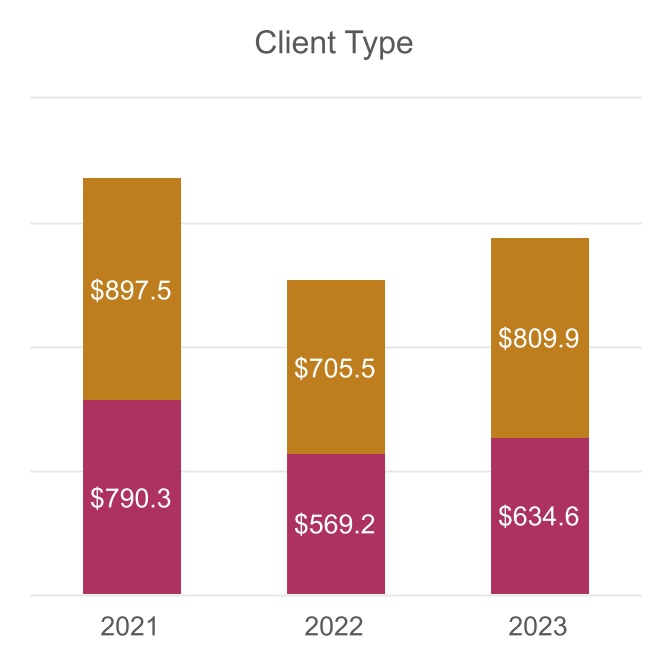

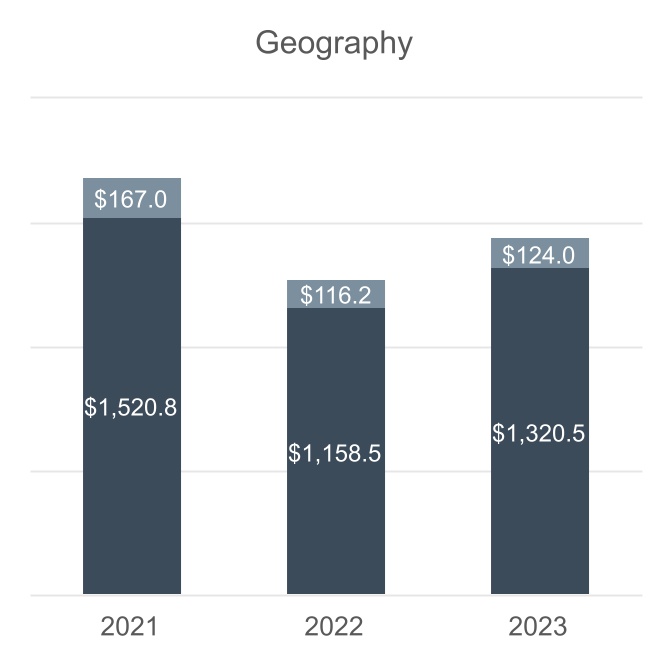

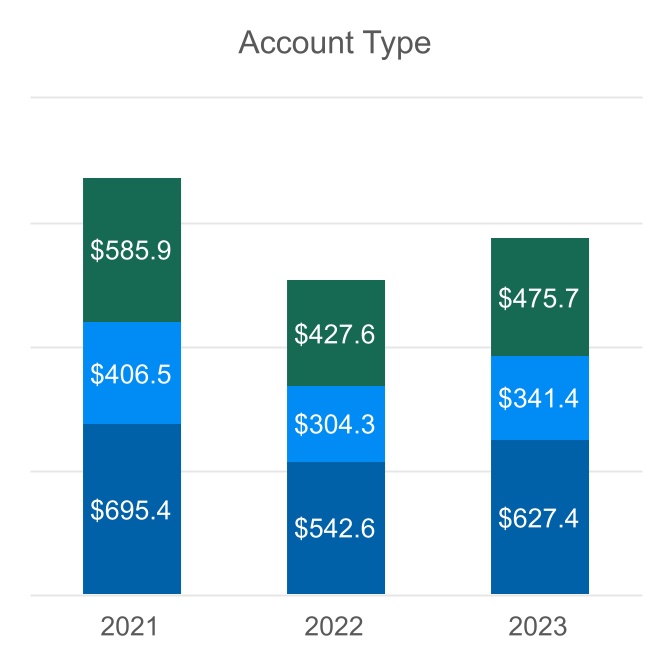

The following charts show our AUM by asset class, client type, geography, and account type as of December 31 for the prior three years:

| | | | | | | | | | | |

| Equity | | Institutional(3) |

| Fixed Income, including money market | | Retail(4) |

| Multi-Asset(1) | | |

| Alternatives(2) | | |

(1)The underlying assets under management of the multi-asset portfolios have been aggregated and presented in this category and not reported in the equity and fixed income rows.

(2)The alternatives asset class includes strategies authorized to invest more than 50% of its holdings in private credit, leveraged loans, mezzanine, real assets/CRE, structured products, stressed / distressed, non-investment grade CLOs, special situations, or have absolute return as its investment objective. Generally, only those strategies with longer than daily liquidity are included.

(3)Institutional includes assets sourced from institutions along with defined contribution assets, including assets sourced through intermediaries and our full-service recordkeeping business.

(4)Retail includes assets sourced through our direct-marketed business and financial intermediaries.

| | | | | | | | | | | |

| United States | | U.S. Defined Contribution |

| APAC, EMEA, Canada | | Other Retirement |

| | | Other Accounts |

Additional information concerning our assets under management, results of operations, and financial condition during the past three years is contained in the Management’s Discussion and Analysis of Financial Condition and Results of Operations in Part II, Item 7, as well as our consolidated financial statements, which are included in Item 8 of this Form 10-K.

SERVICES AND CAPABILITIES.

INVESTMENT MANAGEMENT SERVICES.

Investment Capabilities

We manage a broad range of investment strategies in equity, fixed income, multi-asset, and alternatives across sectors, styles and regions. Our strategies are designed to meet the varied and changing needs and objectives of investors and are delivered across a range of vehicles. We also offer specialized advisory services, including management of stable value investment contracts, modeled multi-asset solutions, and a distribution management service for the disposition of equity securities our clients receive from third-party venture capital investment pools.

The following tables set forth our broad investment capabilities as of December 31, 2023.

| | | | | | | | | | | | | | | | | | | | |

| Equity |

| Growth | Core | Value | Concentrated | Integrated (Quantitative & Fundamental) | Impact |

| U.S.: | All-Cap, Large-Cap, Mid-Cap, Small-Cap, Sectors | Large-Cap, Mid-Cap, Small-Cap | Large-Cap, Mid-Cap, Small-Cap | Large-Cap (Value) | Large-Cap (Growth & Value, Lower Volatility), Multi-Cap, Small-Cap | Large-Cap |

| Global / International: | All-Cap, Large-Cap, Small-Cap, Sectors, Regional | Large-Cap | Large-Cap, Regional | Large-Cap, Regional | Large-Cap (Core) | Large-Cap |

| | | | | | | | | | | | | | | | | | | | |

| Fixed Income |

| Cash | Low Duration | High Yield / Bank Loans | Government | Securitized | Investment Grade Credit |

| U.S.: | Taxable Money, Tax-Exempt Money | Stable Value, Short-Term Bond, Short Duration Income, Ultra-Short Term Bond | Credit Opportunities, Floating Rate, US High Yield | US Inflation Protection, US Treasury | Securitized Credit, CLO, GNMA | US Investment Grade |

| Global / International: | N/O | N/O | Euro High Yield, High Income, Global High Yield | Global Government Bond, Global Government Bond ex-Japan, Global Government Bond High Quality | N/O | Global Investment Grade Corporate, Euro Investment Grade Corporate |

| | | | | | | | | | | | | | | | | |

| |

| Multi-Sector | Dynamic Suite | Emerging Markets | Municipal | Impact |

| U.S.: | QM US Bond, US Core Bond, US Core Plus, US Investment Grade Core, US Total Return | N/O | N/O | Tax-Free High Yield, Intermediate Tax-Free High Yield, Muni Intermediate, Tax-Free Long-Term, Tax-Free Short/Intermediate | N/O |

| Global / International: | Global Multi-Sector, Global Aggregate, International Bond, Euro Aggregate | Dynamic Credit, Dynamic Global Bond, Dynamic Global Bond Investment Grade, Dynamic Emerging Markets Bond | EM Bond, EM Corporate, EM Corporate High Yield, EM Corporate Investment Grade, EM Local Bond, Asia Credit | N/O | Global Impact Credit |

N/O - Not offered

| | | | | | | | | | | | | | | | | |

| Multi-Asset |

| U.S. / Global / International: | Target Date, Custom Target Date | Target Allocation | Global Allocation | Global Income | Managed Volatility |

| Custom Solutions | Real Assets | Retirement Income | N/O | N/O |

N/O - Not offered

| | | | | | | | | | | | | | | | | |

| Alternatives |

| U.S. / Global / International: | Private Credit | Leveraged Loans | Mezzanine | Real Assets / CRE | Structured Products |

| Stressed / Distressed | CLOs - Non-Investment Grade | Special Situations | N/O | N/O |

N/O - Not offered

We employ fundamental and quantitative security analysis in the performance of the investment management function through substantial internal equity, fixed income, and alternative investment research capabilities. Our research staff operates primarily from offices located in the U.S. and U.K. with additional staff based in Australia, China, Hong Kong, Japan, and Singapore. We also use research provided by brokerage firms and security analysts in a supportive capacity and information received from private economists, political observers, commentators, government experts, and market analysts.

We introduce new strategies, investment vehicles, or other products to complement and expand our investment offerings, to respond to competitive developments in the financial marketplace, and to meet the changing needs of our clients. A new strategy is solely dependent on our belief we have the appropriate investment management expertise and its objective will be useful to investors over a long period.

We typically provide seed capital for certain new investment products to begin building an investment performance history in advance of the portfolio receiving sustainable client assets. The length of time we hold our seed capital investment will vary for each new investment product as it is highly dependent on how long it takes to generate cash flows into the product from unrelated investors or, in the case of certain alternative products, the investment term. Generally, we ensure that the new investment product has a sustainable level of assets from unrelated shareholders before we consider redemption of our seed capital investment in order to not negatively impact the product's net asset value or its performance record. At December 31, 2023, we had seed capital investments in our products of $1.4 billion.

We may also close or limit new investments to new investors across sponsored investment products in order to maintain the integrity of the investment strategy and to protect the interests of its existing shareholders and investors. At present, the following strategies, which represent about 5% of total assets under management at December 31, 2023, are generally closed to new investors:

| | | | | |

| Strategy | Year closed |

| U.S. Small-Cap Core | 2013 |

| Capital Appreciation | 2014 |

Distribution Channels and Products

We distribute our products across a diversified client base across five primary distribution channels in three broad geographical regions: Americas; Europe, Middle East and Africa ("EMEA"); and Asia Pacific ("APAC"). We service clients in 51 countries around the world. Investors domiciled outside the U.S. represented about 9% of total assets under management at the end of 2023.

The following table outlines the five distribution channels and products through which our assets under management are sourced as of December 31, 2023.

| | | | | | | | | | | | | | | | | | | | | | | |

| Vehicle | | Retail | | Institutional |

| | Americas financial intermediaries | EMEA & APAC financial intermediaries | Individual U.S. investors on a direct basis | | U.S. Defined Contribution | Global institutions |

| | | | | | | |

| U.S. Mutual Funds | | x | | x | | x | x |

| Collective Investment Trusts | | | | | | x | x |

| Active Exchange-Traded Funds | | x | | x | | | |

| College Savings Plans | | x | | x | | | |

Model Portfolios(1) | | x | | x(6) | | | |

| Managed Accounts / Model Delivery | | x | x | | | | |

| Subadvised Accounts | | x | x | | | | |

| Separate Accounts | | | | x | | x | x |

SICAVs(2) / FCPs(3) | | | x | | | | x |

| Canadian Pooled Funds | | x | | | | | x |

OEICs(4) | | | x | | | | |

Japanese ITMs(5) | | | x | | | | x |

| Australian Unit Trusts | | | x | | | | |

| Private Funds | | | | | | | x |

| Collateralized Loan Obligations | | | | | | | x |

| Business Development Company (BDC) | | x | | | | | x |

(1) Mutual fund models,. (2)Société d'Investissement à Capital Variable (Luxembourg), (3)Fonds Commun de Placement (Luxembourg), (4)Open-Ended Investment Company (U.K.), (5)Japanese Investment Trust Management Funds, (6) Provided through our ActivePlus and Retirement Advisory Service Portfolios.

Investment Advisory Fees

We derive substantially all of our net revenue from investment advisory fees that are earned pursuant to agreements with our sponsored funds and clients. Nearly 57% of our investment advisory fees are earned from our sponsored U.S. mutual funds, with the remaining investment advisory fees earned from our collective investment trusts, subadvised funds, separately managed accounts, and other sponsored products. The other sponsored investment portfolios include: open-ended investment products offered to investors outside the U.S., products offered through variable annuity life insurance plans in the U.S., affiliated private investment funds and sponsored collateralized loan obligations.

Our investment advisory fees are generally computed using the value of assets under management at a contracted annual fee rate or an effective fee rate for those products with a tiered-fee rate structure. For the majority of our revenue, the value of the assets under management used to calculate the fees are based on a daily valuation. The contracted fee rate(s) applied to the fund or account’s assets under management will vary depending on the services provided, the asset class, and vehicle. For example, fee rates are typically higher for equities and alternatives as compared to multi-asset and fixed income products. Additionally, fees rates are typically higher for commingled vehicles including U.S. mutual funds, private investment funds and collective investment trusts as compared to separately managed accounts and subadvised funds.

Investment management agreements typically provide the ability for termination upon relatively short notice with little or no penalty. Specifically, our sponsored U.S. mutual fund investment management agreements must be approved, and fees are annually reviewed by the Boards of the respective funds, including a majority of directors who are not interested persons of the funds or of T. Rowe Price Group (as defined in the Investment Company Act of 1940). Additionally, fund shareholders must approve material changes to these investment management agreements. Each agreement automatically terminates in the event of its assignment (as defined in the Investment Company Act) and, generally, either party may terminate the agreement without penalty after a 60-day notice. The termination of one or more of the U.S. mutual fund agreements could have a material adverse effect on our results of operations.

We also earn performance-based investment advisory fees on certain separately managed accounts and affiliated private investment funds. These performance-based fees are recognized when performance returns exceed the stated hurdle at the end of the performance period, which can lead to an uneven recognition pattern in a given year.

We distribute certain of our sponsored products outside the U.S. through distribution agents and other financial intermediaries. The fees we earn for distributing and marketing these products are part of our overall investment management fees for managing the product assets. We recognize any related distribution fees paid to these financial intermediaries in distribution and servicing costs.

CAPITAL ALLOCATION-BASED INCOME.

We recognize income earned from general partner interests in certain affiliated private investment funds that are entitled to a disproportionate allocation of income, which we also refer to as carried interest. We record our proportionate share of the investment funds' income assuming the funds were liquidated as of each reporting date pursuant to each investment fund's governing agreements. The income will fluctuate period-to-period and the realization of accrued carried interest occurs over a number of years. A portion of this income is allocated to non-controlling interest holders and is reflected in compensation expense as these holders are also employees.

ADMINISTRATIVE, DISTRIBUTION, AND SERVICING FEES.

Administrative Services

We also provide certain ancillary administrative services to our investment advisory clients. These administrative services are provided by several of our subsidiaries and include mutual fund transfer agent, fund/portfolio accounting, distribution, and shareholder services; participant recordkeeping and transfer agent services for defined contribution retirement plans investing in our sponsored U.S. mutual funds; recordkeeping services for defined contribution retirement plans investing in mutual funds outside the T. Rowe Price complex; brokerage; trust services; and non-discretionary advisory services.

Distribution and Servicing

Our subsidiary, T. Rowe Price Investment Services, is the principal distributor of our U.S. mutual funds and contracts with third-party financial intermediaries who distribute these share classes. Certain of the U.S. mutual funds offer Advisor Class and R Class shares that are distributed to investors and defined contribution retirement plans, respectively. These share classes pay 12b-1 fees of 25 and 50 basis points, respectively, out of fund assets, for distribution, administration, and personal services. In addition, U.S. mutual funds offered to investors through variable annuity life insurance plans have a share class that pays a 12b-1 fee of 25 basis points. We pay all of the 12b-1 fees earned to financial intermediaries who source assets under management into these share classes and provide distribution, administration, and personal services on our behalf.

REGULATION.

All aspects of our business are subject to extensive federal, state, and foreign laws and regulations. These laws and regulations are primarily intended to benefit or protect our clients and product shareholders. They generally grant supervisory agencies and bodies broad administrative powers, including the power to limit or restrict the conduct of our business if we fail to comply with laws and regulations. Possible sanctions that may be imposed on us, if we fail to comply, include the suspension of individual employees, limitations on engaging in certain business activities for specified periods of time, revocation of our investment adviser and other registrations, censures, and fines. Furthermore, the regulations to which we are subject continue to change over time, resulting in uncertainty for our business as we must adapt to new laws and regulatory regimes and could significantly increase our reporting, disclosure and compliance obligations, including for cybersecurity and climate-related disclosures.

As a global company which offers its products to customers in a variety of jurisdictions, our subsidiaries are registered with or licensed by various U.S. and/or non-U.S. regulators. We are subject to various securities/financial services, compliance, corporate governance, disclosure, privacy, cybersecurity, technology, anti-bribery and anti-corruption, anti-money laundering, anti-terrorist financing, and economic, trade and sanctions laws and regulations, both domestically and internationally, as well as to various cross-border rules and regulations, and the data protection laws and regulations of numerous jurisdictions, including the General Data Protection Regulation (“GDPR”) of the European Union (“EU”) and the California Consumer Privacy Act (“CCPA”). We also must comply with complex and changing tax regimes in the jurisdictions where we operate our business.

The following table shows the securities and financial services regulator to certain of our subsidiaries:

| | | | | | | | | | | |

| Regulator | | T. Rowe Price Entity |

| Within the U.S. |

| Securities & Exchange Commission | | - T. Rowe Price Associates | - T. Rowe Price Hong Kong |

| | - T. Rowe Price International | - T. Rowe Price Japan |

| | - T. Rowe Price Australia | - T. Rowe Price Singapore |

| | - T. Rowe Price (Canada) | - T. Rowe Price Advisory Services |

| | - T. Rowe Price Investment Management | - Oak Hill Advisors |

| | - Oak Hill Advisors (Europe) | - OHA (UK) |

| | -OHA Private Credit Advisors | - OHA Private Credit Advisors II |

| | | |

| | All entities above are registered as investment advisers under the Investment Advisers Act of 1940, which imposes substantive regulation around, among other things, fiduciary duties to clients, transactions with clients, effective compliance programs, conflicts of interest, advertising, recordkeeping, reporting, and disclosure requirements. |

| State of Maryland, Office of Financial Regulation | | - T. Rowe Price Trust Company |

| | | |

| Outside the U.S. | | | |

| Financial Conduct Authority | | - T. Rowe Price International | |

| | - T. Rowe Price UK |

| | - Oak Hill Advisors (Europe) |

| | - OHA (UK) | |

| Securities and Futures Commission | | - T. Rowe Price Hong Kong | |

| | - Oak Hill Advisors (Hong Kong) |

| Monetary Authority of Singapore | | - T. Rowe Price Singapore | |

| Several provincial securities commissions in Canada | | - T. Rowe Price (Canada) | |

| Commission de Surveillance du Secteur Financier | | - T. Rowe Price (Luxembourg) Management Sàrl |

| | - OHA Services Sàrl | |

| Australian Securities and Investments Commission | | - T. Rowe Price Australia | |

| | - Oak Hill Advisors (Australia) Pty |

| Japan Financial Services Agency | | - T. Rowe Price Japan | |

Swiss Financial Market Supervisory Authority | | - T. Rowe Price (Switzerland) |

Serving the needs of retirement savers is an important focus of our business. Such activities are subject to regulators such as the U.S. Department of Labor, and applicable laws and regulations including the Employee Retirement Income Security Act of 1974 ("ERISA").

Registrations

•Our subsidiaries providing transfer agent services, T. Rowe Price Services and T. Rowe Price Retirement Plan Services, are registered under the Securities Exchange Act of 1934.

•T. Rowe Price Investment Services (TRPIS) is an SEC registered introducing broker-dealer and member of the Financial Industry Regulatory Authority ("FINRA") and the Securities Investor Protection Corporation. This subsidiary is the principal underwriter and distributor for our sponsored U.S. mutual funds and exchange-

traded funds, and may also offer and make recommendations for certain funds that are not offered to the general public such as privately placed funds. Investors may open a brokerage account with TRPIS in order to buy and sell securities. Pershing, a third-party clearing broker and an affiliate of BNY Mellon, maintains our brokerage’s customer accounts and clears all transactions.

•T. Rowe Price Associates and certain subsidiaries are registered as commodity trading advisors and/or commodity pool operators with the Commodity Futures Trading Commission and are members of the National Futures Association.

Net Capital Requirements

Certain subsidiaries are subject to net capital requirements, including those of various federal, state, and international regulatory agencies. Each of our subsidiary's net capital, as defined, meets or exceeds all minimum requirements as of December 31, 2023.

For further discussion of the potential impact of current or proposed legal or regulatory requirements, please see the Legal and Regulatory risk factors included in Item 1A of this Form 10-K.

COMPETITION.

As a member of the financial services industry, we are subject to substantial competition in all aspects of our business. A significant number of proprietary and other sponsors’ mutual funds are sold to the public by other investment management firms, broker-dealers, mutual fund companies, banks, and insurance companies. We compete with brokerage and investment banking firms, insurance companies, banks, mutual fund companies, hedge funds, and other financial institutions and funds in all aspects of our business and in every country in which we offer our products and services. Some of these financial institutions have greater resources than we do. We compete with other providers of investment advisory services based primarily on the availability and objectives of the investment products offered, investment performance, fees and related expenses, and the scope and quality of investment advice and other client services.

We have and will continue to face significant competition from passive oriented investment strategies. As a result, such products have taken market share from active managers. While we cannot predict how much market share these competitors will continue to gain, we believe there will always be demand for good active management investment products.

In order to maintain and enhance our competitive position, we may review acquisition and venture opportunities and, if appropriate, engage in discussions and negotiations that could lead to an acquisition transaction or other financial relationships with another entity.

HUMAN CAPITAL.

At T. Rowe Price, our people set us apart. We thrive because our company culture is based on collaboration and diversity. We believe that our culture of collaboration enables us to identify opportunities others might overlook. Our associates’ knowledge, insight, enthusiasm, and creativity are the reason our clients succeed and our firm excels. In order to attract and retain the highest quality talent, we develop key talent and succession plans, invest in firm diversity and inclusion initiatives, provide opportunities for our associates to learn and grow, and provide strong, competitive, and regionally specific benefits and programs that promote the health and wellness of our associates, both personally and financially.

At December 31, 2023, we employed 7,906 associates, an increase of 0.5% from the 7,868 associates employed at the end of 2022. We may add temporary and part-time personnel to our staff from time to time to meet periodic and special project demands, primarily for technology and collective investment fund administrative services.

Investing In Our People

We seek to help our clients achieve their long-term investment goals. In order to do this, we are committed to helping our associates achieve their long-term career goals. We continuously seek to identify new opportunities for our associates to expand their experience and grow their skills. As a result of our associates developing these skills we are able to promote from within, with more than 35% of our open positions being filled by internal applicants, and

all of our portfolio managers having been promoted from within. We are committed to the professional growth of our associates through the development of their knowledge, skills and experience, by providing them access to in-person, virtual and online training programs and by offering a generous tuition reimbursement program. We believe a critical driver of our firm’s future growth is our ability to grow leaders. Reflecting this, we have held a series of leadership speaker events and offer access to virtual programs focused on leadership development led by professors at leading universities.

Hiring Diverse Talent

Having a diverse and inclusive workforce and providing an equal opportunity to all associates is a business and cultural imperative. Our diversity, equity, and inclusion initiatives have garnered recognitions, including World's Most Admired Companies from Fortune, Barron's 100 Most Sustainable Companies and America's Most Responsible Companies from Newsweek. We also continue to be a top company for LGBTQ+ equality by the Human Rights Campaign Foundation. Although we have made progress in our workforce diversity representation, we seek to continuously improve in this area. Our priority is to increase our hiring, retention and development of talent from groups that are underrepresented in asset management; including both ethnically diverse associates and women. At the end of 2023, female associates held 32.5% of senior roles globally and ethnically diverse associates held 19.8% of senior roles in the U.S. For every open role at the firm, our goal is that at least 40% of interviewed candidates will be female and/or ethnically diverse, and during 2023, 65% of the candidates were ethnically diverse and/or female.

In an effort to be more transparent, we publish our EEO data on our website at https://www.troweprice.com/corporate/us/en/what-sets-us-apart/diversity-and-inclusion.html. In addition, during 2023, we published our sustainability report which included transparency into our diversity, equity and inclusion data, a copy of which can be found on our website at https://www.troweprice.com/corporate/us/en/what-we-do/esg-approach/esg-corporate.html. Set forth below is our diversity information as of December 31, 2023, grouped by division. The data excludes information about the employees of OHA.

Investments Group Diversity Breakdown

| | | | | | | | | | | | | | | | | | | | | | | |

| Gender Representation - Global Population | | Ethnically Diverse - US Population Only |

| Female | Male | Total | | Ethnically Diverse | Non- Ethnically Diverse | Total |

| Investments Group | 28% | 72% | 968 | | | 24% | 76% | 683 | |

| Portfolio Managers | 14% | 86% | 171 | | | 15% | 85% | 126 | |

| Analysts | 30% | 70% | 361 | | | 37% | 63% | 247 | |

| Traders | 26% | 74% | 97 | | | 21% | 79% | 66 | |

| All Other Roles | 35% | 65% | 339 | | | 16% | 84% | 244 | |

Global Distribution and Global Product Group Diversity Breakdown

| | | | | | | | | | | | | | | | | | | | | | | |

| Gender Representation - Global Population | | Ethnically Diverse - US Population Only |

| Female | Male | Total | | Ethnically Diverse | Non- Ethnically Diverse | Total |

| Global Distribution & Global Product | 48% | 52% | 2,927 | | | 30% | 71% | 2,636 | |

| Senior Level* | 35% | 65% | 537 | | | 16% | 84% | 438 | |

| All Others | 51% | 49% | 2,390 | | | 32% | 68% | 2,198 | |

Corporate Functions Group Diversity Breakdown

| | | | | | | | | | | | | | | | | | | | | | | |

| Gender Representation - Global Population | | Ethnically Diverse - US Population Only |

| Female | Male | Total | | Ethnically Diverse | Non- Ethnically Diverse | Total |

| Corporate Functions | 45% | 55% | 3,590 | | | 35% | 65% | 2,865 | |

| Senior Level* | 43% | 57% | 462 | | | 20% | 80% | 358 | |

| All Others | 45% | 55% | 3,128 | | | 37% | 63% | 2,507 | |

* Senior Level is defined as people leaders and individual contributors with significant business or functional responsibility.

AVAILABLE INFORMATION.

We intend to use our website, troweprice.com, as means of disclosing material non-public information and for complying with our disclosure obligations under Regulation FD. These disclosures will be included in the Investor Relations section of our website, investors.troweprice.com. We make our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) of the Exchange Act, available free of charge in this section of our website as soon as reasonably practicable after they have been filed with the SEC. In addition, our website includes the following information:

•our financial statement information from our periodic SEC filings in the form of XBRL data files that may be used to facilitate computer-assisted investor analysis;

•corporate governance information including our governance guidelines, committee charters, senior officer code of ethics and conduct, and other governance-related policies;

•other news and announcements that we may post from time to time that investors might find useful or interesting, including our monthly assets under management disclosure and periodic investor presentations; and

•opportunities to sign up for email alerts and RSS feeds to have information pushed in real time.

Accordingly, investors should monitor this section of our website, in addition to following our press releases, SEC filings, and public webcasts, all of which will be referenced on the website. Unless otherwise expressly stated, the information found on our website is not incorporated into this or any other report we file with, or furnish to, the SEC. Specifically, information in our sustainability report is not incorporated by reference into this Form 10-K.

The SEC maintains a website that contains the materials we file with the SEC at www.sec.gov.

Item 1A. Risk Factors.

An investment in our common stock involves various risks, including those mentioned below and those that are discussed from time to time in our periodic filings with the SEC. Investors should carefully consider these risks, along with the other information contained in this report, before making an investment decision regarding our common stock. There may be additional risks of which we are currently unaware, or which we currently consider immaterial. Any of these risks could have a material adverse effect on our financial condition, results of operations, and value of our common stock.

RISKS RELATING TO OUR BUSINESS AND THE FINANCIAL SERVICES INDUSTRY.

Our revenues are based on the market value and composition of the assets under our management, all of which are subject to fluctuation caused by factors outside of our control.

We derive our revenues primarily from investment advisory services provided by our subsidiaries to individual and institutional investors. Our investment advisory fees typically are calculated as a percentage of the market value of the assets under our management. As a result, our revenues are dependent on the value and composition of the assets under our management, all of which are subject to substantial fluctuation due to many factors, including:

•Investment Performance. If the investment performance of our managed investment portfolios is less than that of our competitors or applicable third-party benchmarks, we could lose existing and potential clients and suffer a decrease in assets under management. Poor performance relative to other competing products tends to result in decreased sales and increased redemptions with corresponding decreases in our revenues.

•General Financial Market Declines. We derive a significant portion of our revenues from advisory fees on managed investment portfolios. A downturn in financial markets would cause the value of assets under our management to decrease, and may also cause investors to withdraw their investments, thereby further decreasing the level of assets under our management.

•Investment Concentration. The allocation of investment products for assets under management within market segments or strategies may impact associated fees that can vary depending on product offerings.

•Investor Mobility. Our investors generally may withdraw their funds at any time, without advance notice and with little to no significant penalty. Any redemptions and other withdrawals from, or shifting among, our investment portfolios could reduce our assets under management. These could be caused by investors reducing their investments in our portfolios in general or in the market segments in which we focus; investors taking profits from their investments; and portfolio risk characteristics, which could cause investors to move assets to other investment managers.

•Capacity Constraints. Prolonged periods of strong relative investment performance and/or strong investor inflows has resulted in, and may result in, capacity constraints within certain strategies, which can lead to, among other things, the closure of those strategies to new investors.

•Investing Trends. Changes in investing trends, particularly investor preference for passive or alternative investment products as well as increasing investor preference for environmentally and socially responsible investment products, and changes in retirement savings trends, may reduce interest in our products and may alter our mix of assets under management.

•Interest Rate Changes. Investor interest in and the valuation of our fixed income and multi-asset investment portfolios are affected by changes in interest rates.

•Geo-Political Exposure. Our managed investment portfolios may have significant investments in markets that are subject to risk of loss from political or diplomatic developments, government policies, wars, conflicts or civil unrest (such as the Russian invasion of Ukraine, the threat that Russia’s military aggression may expand beyond Ukraine, and the recent conflicts in the Middle East), trade wars or tariffs, currency fluctuations, illiquidity and capital controls, and changes in legislation related to ownership limitations.

A decrease in the value of our assets under management, or an adverse change in their composition, particularly in market segments where our assets are concentrated, could have a material adverse effect on our investment advisory fees and revenues. For any period in which revenues decline, net income and operating margins will likely decline by a greater proportion because certain expenses will be fixed over that finite period and may not decrease in proportion to the decrease in revenues.

A majority of our revenues are based on contracts with collective investment funds that are subject to termination without cause and on short notice.

We provide investment advisory, distribution, and other administrative services to collective investment funds under various agreements. Investment advisory services are provided to each T. Rowe Price collective investment fund under individual investment management agreements, which can be terminated on short notice. In addition, the Board of each T. Rowe Price U.S. mutual fund must annually approve the terms of the investment management and service agreements. If a T. Rowe Price collective investment fund seeks to lower the fees that we receive or terminate its contract with us, we would experience a decline in fees earned from the collective investment funds, which could have a material adverse effect on our revenues and net income.

We operate in an intensely competitive industry. Competitive pressures may result in a loss of clients and their assets or compel us to reduce the fees we charge to clients, thereby reducing our revenues and net income.

We are subject to competition in all aspects of our business from other financial institutions. Some of these financial institutions have greater resources than we do and may offer a broader range of financial products across more markets. Some competitors operate in a different regulatory environment than we do which may give them certain competitive advantages in the investment products and portfolio structures that they offer. We compete with other providers of investment advisory services primarily based on the availability and objectives of the investment products offered, investment performance, fees and related expenses, and the scope and quality of investment advice and other client services. Some institutions have proprietary products and distribution channels that make it more difficult for us to compete with them. Substantially all of our investment products are available without sales or redemption fees, which means that investors may be more willing to transfer assets to competing products. If our clients reduce their investments with us, and we are not able to attract new clients, our AUM, revenue and earnings could decline.

The market environment in recent years has led investors to increasingly favor lower fee passive investment products. As a result, investment advisors that emphasize passive products have gained and may continue to gain market share from active managers like us. While we believe there will always be demand for strong performing active management, we cannot predict how much market share these competitors will gain.

Furthermore, many aspects of the asset management industry are seeing increased regulatory activity and scrutiny, in particular related to environmental, social, and governance ("ESG") practices and related matters, transparency and unbundling of fees, inducements, conflicts of interest, risk management, cybersecurity, technology, privacy and data protection, diversity, equity and inclusion, and compensation. We may respond to these regulatory matters or may be impacted by these actions in a manner different from our competitors, which may impact our AUM or result in the loss of clients and their assets.

As part of our continued efforts to attract and retain clients, we develop and launch new products and services, which may require expenditure of resources and may expose us to new regulatory or compliance requirements as well as increased risk of operational or client service errors.

In the event that we decide to reduce the fees we charge for investment advisory services in response to competitive pressures, which we have done selectively in the past, revenues and operating margins could be adversely impacted. Fee reductions may vary depending on strategy and product offerings, which could result in investment rebalancing or reallocation adversely impacting revenues and operating margins.

The failure or negative performance of products offered by competitors may cause our products, which are similar, to be impacted irrespective of our performance.

Many competitors offer similar products to those offered by us, and the failure or negative performance of competitors’ products could lead to a loss of confidence in similar products we offer, irrespective of the performance of such products. Any loss of confidence in a product type could lead to withdrawals, redemptions and liquidity issues in such products, which may cause our AUM, revenue and earnings to decline.

Our operations are complex and a failure to properly execute operational processes could have an adverse effect on our reputation and decrease our revenues.